Corporations in the United States pay federal corporate income taxes levied at a 21 percent rate. Forty-four states and D.C. also levy taxes on corporate income, with top marginal rates ranging from 2.5 percent in North Carolina to 11.5 percent in New Jersey. Fifteen of the states levy graduated corporate income tax rates, while the remaining 29 states and D.C. levy a flat rate on corporate income.

In Nevada, Ohio, Texas, and Washington, corporations are subject to gross receipts taxes instead of corporate income taxes. Delaware, Oregon, and Tennessee impose a tax on corporate income and a separate levy on gross receipts. Pennsylvania, Virginia, and West Virginia levy gross receipts taxes at the local (but not state) level too.

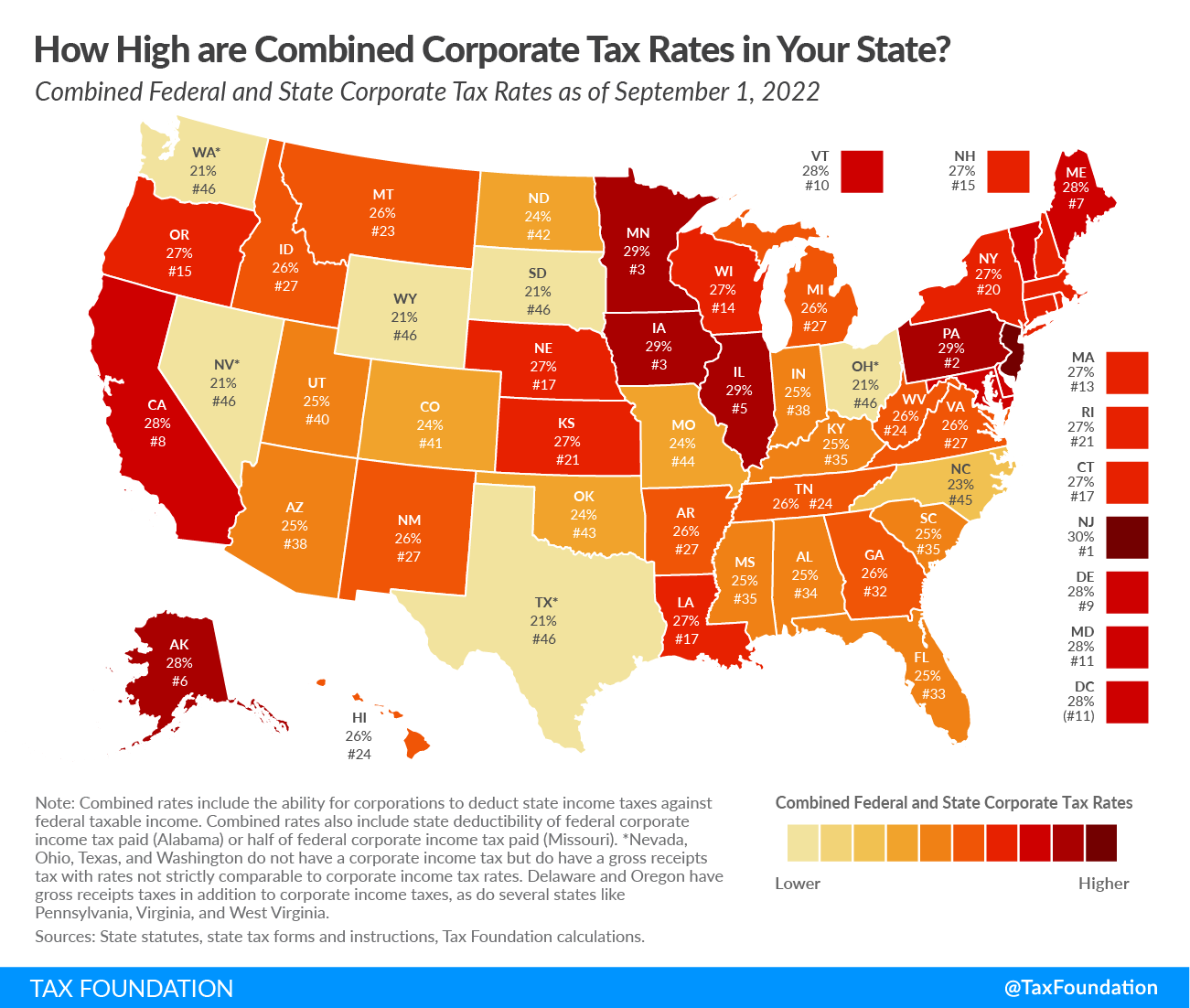

The state with the highest combined state and federal corporate tax rate is New Jersey at 30.1 percent. Corporations in Alaska, California, Illinois, Iowa, Maine, Minnesota, and Pennsylvania face combined corporate tax rates at or above 28 percent. Six states—Ohio, Nevada, South Dakota, Texas, Washington, and Wyoming—face no state corporate income tax and only face the federal tax rate of 21 percent.

{kind=link}

Corporations may deduct state corporate income tax paid against federal taxable income, lowering the effective federal corporate income tax rate. For example, a corporation in Rhode Island may deduct tax paid at a 7 percent flat rate against the 21 percent federal corporate income tax, reducing its federal rate to 19.53 percent and a combined rate of 26.53 percent.

Additionally, two states allow corporations to deduct federal corporate income tax against some portion of state corporate income tax. Alabama allows full deductibility of federal corporate income tax liability against state liability, while Missouri permits a 50 percent deduction of federal corporate income tax liability. This lowers the effective corporate income tax rate faced by corporations in these states.

Louisiana provided a full deduction for federal corporate income taxes before January 1, 2022, but it repealed deductibility last year. Iowa also previously permitted a 50 percent deduction for federal corporate income taxes, but this provision expired in 2021.

When examining tax burdens on businesses, it is important to consider both federal and state corporate taxes. Corporate taxes are one of the most economically damaging ways to raise revenue and are a promising area of reform for states to increase competitiveness and promote economic growth, benefiting both companies and workers.