Key Findings

- Taxpayers reported nearly $11.8 trillion of total income on their 2018 tax returns.

- About 67 percent ($7.9 trillion) of the total income reported on Form 1040 consisted of wages and salaries, and 82 percent of all tax filers reported earning wage income.

- Retirement accounts such as 401(k)s and pensions are important sources of capital income for the middle class. Taxable IRA (Individual Retirement Account) distributions, pensions, and annuities (nearly $1.1 trillion) and taxable Social Security benefits ($337 billion) accounted for about $1.42 trillion of income in 2018.

- Business income is another large component of reported personal income. Businesses that report income taxes through the individual income tax, like S corporations, sole proprietorships, and partnerships, accounted for $1.1 trillion of income in 2018.

- Investment income consisting of net capital gains, taxable interest, and ordinary dividends accounted for nearly $1.4 trillion of income in 2018, more than business income and slightly less than taxable retirement income.

Introduction

The individual income tax is the federal government’s largest source of revenue. More than 153 million individual income tax returns were filed for tax year 2018, the first year under the changes made by the Tax Cuts and Jobs Act (TCJA).

Each household with taxable income must file a return to the Internal Revenue Service (IRS). On the IRS individual income tax form (Form 1040), all sources of taxable income are listed on the first page and added to reach total income. From there, the taxpayer’s deductions and credits are calculated on the tax return to determine tax liability and tax owed or refunded.

This report will focus on sources of reported total income in 2018, which amounted to just under $11.8 trillion.[1] We will review the component parts of total income reported on lines 1 through 5 of the 2018 Form 1040 and on the 2018 Schedule 1.[2] Reviewing reported income helps to understand the composition of the federal government’s revenue base and how Americans earn their taxable income.[3] We divide income into four major categories—wages and salaries, business income, investment income, and retirement income—and review each category for tax year 2018.

| Income Type | Amount |

|---|---|

| Salaries and Wages | $7,908 |

| Taxable Individual Retirement Arrangement (IRA) distributions, pensions, and annuities | $1,087 |

| Capital Gains Less Losses | $927 |

| Partnership and S Corporation Net Income (Less Losses) | $683 |

| Business or Profession Net Income (Less Losses) | $349 |

| Taxable Social Security Benefits | $337 |

| Ordinary Dividends* | $321 |

| Taxable Interest** | $129 |

| Total Rent and Royalty Net Income (Less Losses) | $65 |

| Other income less loss | $45 |

|

* The IRS excludes qualified dividends from total income, which amounts to about $243 billion. ** Tax-free interest, such as interest on municipal bonds, adds another $60 billion. Source: IRS SOI Table 1.3. |

|

Wages and Salaries Make Up $7.9 Trillion of Personal Income

Wages and salaries comprise the largest overall source of total income. For most tax filers in the U.S., the largest income number on their own Form 1040 appears on the line where they report wages, salaries, tips, and other compensation for their work. In other words, most Americans report earning labor income, and most of their income comes from labor as most of the American economy is made up of labor compensation. In total, nearly 127 million tax filers in 2018 reported $7.9 trillion in wage income, making up 67 percent of total income.

The amounts reported on Form 1040 reflect most, but not all, labor compensation. For example, businesses also pay for employee health benefits and make contributions to Social Security, both of which are excluded from income taxation.

Wage and salary income is taxed at a progressive rate schedule with rates ranging from 10 percent to 37 percent. The top rate of 37 percent was levied on taxable income above $500,000 for single filers and above $600,000 for married couples filing jointly in tax year 2018.[4]

Business Income Makes Up $1.1 Trillion of Personal Income

In the United States, passthrough entities are the dominant tax filing structure for businesses, so labeled because the income is not taxed at the business level but instead immediately passed through to individual owners’ tax returns using schedules C, E, and F. According to the U.S. Census Bureau, in 2018, 92.5 percent of businesses used the passthrough structure, and the majority were sole proprietorships, fully owned by a single individual.[5]

Passthrough firms employ most of the private-sector workforce in the U.S., and account for most business income.[6] Partnerships and S corporations reported $683 billion of net income in 2018. Individuals reported an additional $348 billion of business or professional income (sole proprietorship income). Together, business income totaled about $1.1 trillion when including income from estates, farms, trusts, rents, and royalties.[7]

Unlike corporations subject to the corporate income tax, passthrough business income is taxed as ordinary income on owners’ personal tax returns. Like salaries and wages, passthrough business income is taxed at the same progressive rate schedule. However, the TCJA established a temporary 20 percent tax deduction for passthrough business income, notwithstanding certain limits and qualifications.[8]

Investment Income Makes Up Nearly $1.4 Trillion of Personal Income

Overall taxable investment income amounted to just over $1.39 trillion in 2018, consisting of taxable interest, dividends, and capital gains income. Taxpayers reported $321 billion of taxable ordinary dividends and $927 billion of net capital gains and capital gain distributions, only some of which comes from the sale of corporate stock.[9] Taxable interest accounted for about $129 billion, and taxpayers reported $19.7 billion of net gains from sales of property other than capital assets, such as certain real business property or copyrights.

Taxable labor compensation is much larger than taxable investment income. While the returns to corporate stock found on individual income tax returns are substantial, they are small compared to the amount of labor income taxpayers earned, which totaled $7.9 trillion in tax year 2018.

{kind=link}

Some investment income is subject to ordinary income tax rates and some is subject to a separate schedule with lower tax rates. Taxable interest, ordinary dividends, and short-term capital gains (gains realized on assets held for less than one year) are taxed as ordinary income at a taxpayer’s marginal income tax rate, just like wage and salary income. Long-term capital gains (gains realized on assets held for more than one year) are taxed at lower rates, ranging from 0 percent to 20 percent, plus a 3.8 percent net investment income tax, depending on a taxpayer’s taxable income.[10]

Retirement Income Makes Up More Than $1.42 Trillion of Personal Income

In 2018, taxpayers reported about $1.1 trillion of taxable Individual Retirement Account (IRA) distributions and pensions and annuities.[11] In addition to private saving, taxpayers reported about $337 billion in taxable Social Security benefits in tax year 2018, for a total of $1.42 trillion in taxable retirement income.

Taxpayers reported slightly more taxable investment income from retirement accounts than from outside of retirement accounts. America’s system of retirement accounts, while overly complex, is taxed neutrally, removing the bias against saving.[12]

It is often hard to track capital income in retirement accounts, especially because it does not appear on IRS forms until it is distributed. Economists often struggle with categorizing retirement income correctly. The Congressional Budget Office (CBO) released a report in 2011 on trends in the distribution of income which reviewed the portion of capital income in retirement accounts.[13]

The report accounted for all the sources of income, including some nontaxable sources. The authors categorized incomes by source, sorting pensions into a separate category from labor income and capital income. Pensions are, in part, compensation for labor. Workers also earn capital income by deferring their labor income and having that income invested, often amounting to multiples of their original contributions. While it is difficult to allocate pension income precisely between labor and capital, workers earn capital income through their pensions. The CBO report sorted retirement income into a category called “other.”

The CBO report shows that while it is true that middle-class Americans do not report much investment income such as dividends or capital gains on their tax returns, they still earn returns to capital through their retirement accounts, where saving receives proper tax treatment.

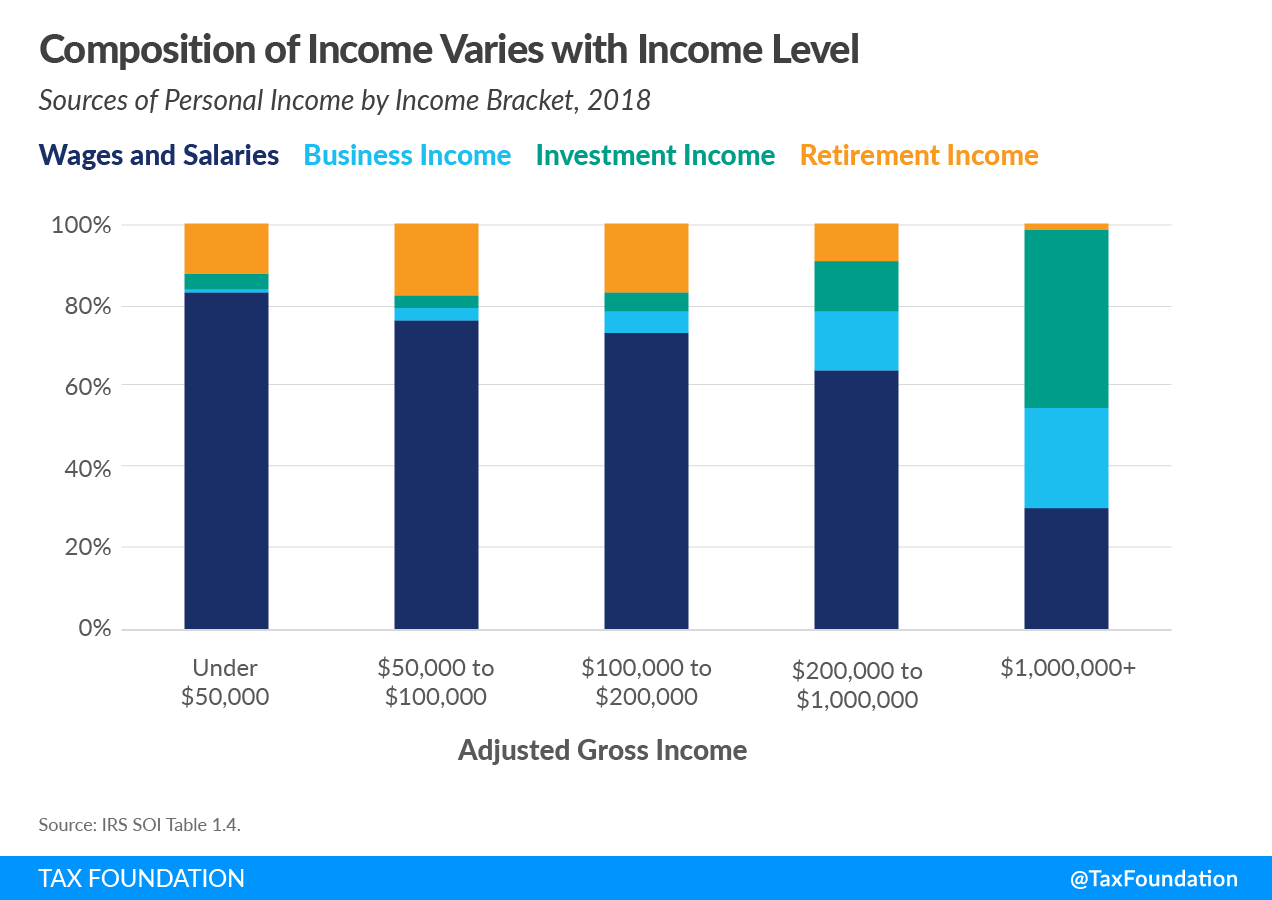

Reviewing the sources of personal income by income bracket shows the importance of retirement income to the middle class (Figure 2). Retirement income is most important as a source of personal income for taxpayers reporting between $50,000 and $100,000 of income, making up nearly 18 percent of total income. In practice, of course, a minority of middle-class taxpayers— the retirees—rely on this income, while the majority of working-age taxpayers do not.

{kind=link}

Retirement income is difficult to account for, and the tax rules governing retirement accounts are not obvious to people unfamiliar with tax data. Pension and other retirement income is, in economic terms, partially capital income; it is about as important as any other kind of capital income; and it is most important to middle-class workers, given their accessibility of retirement options. It is important to consider tax reforms that would expand the accessibility of retirement and savings accounts that are neutral with respect to saving and consumption.[14]

Many retirement accounts offer tax-deferred or tax-exempt status to minimize initial tax burden and maximize future earnings. Distributions from tax-deferred IRAs and withdrawals from pension and annuity accounts are taxed as typical income and face a progressive rate schedule with rates ranging from 10 percent to 37 percent. A portion of Social Security benefits may be taxable at ordinary income tax rates, depending on a taxpayer’s total amount of income and benefits for the tax year.[15]

Conclusion

Reviewing the sources of personal income shows that the personal income tax is largely a tax on labor, primarily because our personal income is mostly derived from labor. However, varied sources of capital income also play a role in American incomes. While capital income sources are small compared to labor income, they are still significant and need to be accounted for, both by policymakers trying to collect revenue efficiently and by those attempting to understand the distribution of personal income.

[1] IRS, “SOI Tax Stats,” Table 1.3.

[2] The Form 1040 changed in Tax Year 2018, reflecting changes from the TCJA. For more information, see IRS, “Questions and Answers about the 2018 Form 1040,” https://www.irs.gov/forms-pubs/questions-and-answers-about-the-2018-form-1040.

[3] Using data from Form 1040 to understand the nature of income in the U.S. economy comes with some limitations. Not all economic activity is found on personal income tax forms—for example, employer-provided health insurance and returns to owner-occupied housing are excluded. Both are substantial components of economic output that do not appear on income tax returns. As broad economic aggregates, though, the categories of income established on Form 1040 are still useful and instructive.

[4] Amir El-Sibaie, “2018 Tax Brackets,” Tax Foundation, Jan. 2, 2018, https://www.taxfoundation.org/2018-tax-brackets/.

[5] U.S. Census Bureau, “County Business Patterns (CBP),” https://census.gov/programs-surveys/cbp.html, and U.S. Census Bureau, “Nonemployer Statistics (NES),” https://census.gov/programs-surveys/nonemployer-statistics.html.

[6] Scott Greenberg, “Pass-Through Businesses: Data and Policy,” Tax Foundation, Jan. 17, 2017, https://www.taxfoundation.org/pass-through-businesses-data-and-policy.

[7] IRS, “SOI Tax Stats,” Table 1.3.

[8] For more, see Scott Greenberg, “Reforming the Pass-Through Deduction,” Tax Foundation, June 21, 2018, https://www.taxfoundation.org/reforming-pass-through-deduction-199a/.

[9] IRS, “SOI Tax Stats.”

[10] Qualified dividends are also taxed at preferential rates, but the IRS does not include qualified dividends in total income.

[11] IRS, “SOI Tax Stats,” Table 1.3.

[12] See generally, Erica York, “The Complicated Taxation of America’s Retirement Accounts,” Tax Foundation, May 22, 2018, https://www.taxfoundation.org/ retirement-accounts-taxation/.

[13] Congressional Budget Office, “Trends in the Distribution of Household Income between 1979 and 2007,” Oct. 25, 2011, http://cbo.gov/sites/default/files/10-25-HouseholdIncome_0.pdf.

[14] See Erica York, “The Complicated Taxation of America’s Retirement Accounts,” and Robert Bellafiore, “The Case for Universal Savings Accounts,” Tax Foundation, Feb. 26, 2019, https://www.taxfoundation.org/case-for-universal-savings-accounts/.

[15] See Internal Revenue Service, “Social Security Income,” https://www.irs.gov/faqs/social-security-income.

Banner image attribution: 1040 tax form lies near hundred dollar bills and blue pen on a light blue background. US Individual income tax return.