The Social Security trust funds face looming insolvency if policymakers don’t reform the program. One issue that garners a lot of attention in the debate over solutions is the payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue.

cap. Some have proposed raising the cap to increase the share of wage and salary income covered by the payroll taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

. But policymakers should also recognize that broader changes in how workers are compensated have contributed to the decline in wages subject to payroll taxes. Therefore, expanding the payroll tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

to include all forms of worker compensation should also be on the table.

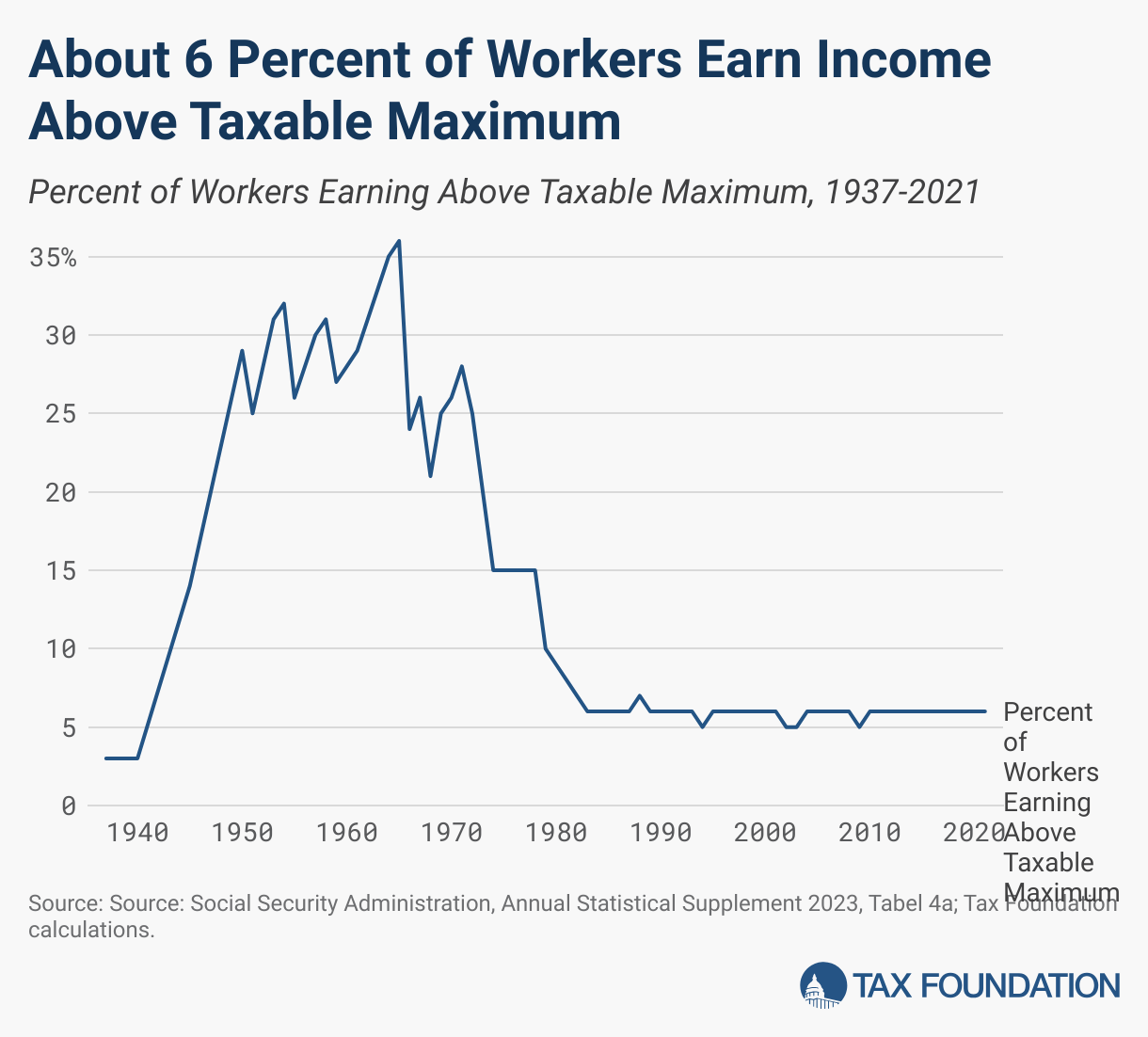

When Social Security was introduced in 1937, it applied a 2 percent payroll tax to the first $3,000 of earnings ($66,000 in today’s dollars). It covered about 92 percent of taxable earnings at the time, and only 3 percent of workers earned more than the taxable maximum. From 1937 to 1950, the cap was fixed, and the share of workers earning more than the taxable maximum quickly rose from 3 percent to as high as 29 percent by 1950. Legislation over the next two decades periodically raised the cap, but it wasn’t until the 1977 amendments introduced wage indexing that the cap would increase each year. Since then, the cap automatically adjusts each year based on the average growth in wages, and the share of workers earning above the taxable maximum has stabilized around 6 percent.

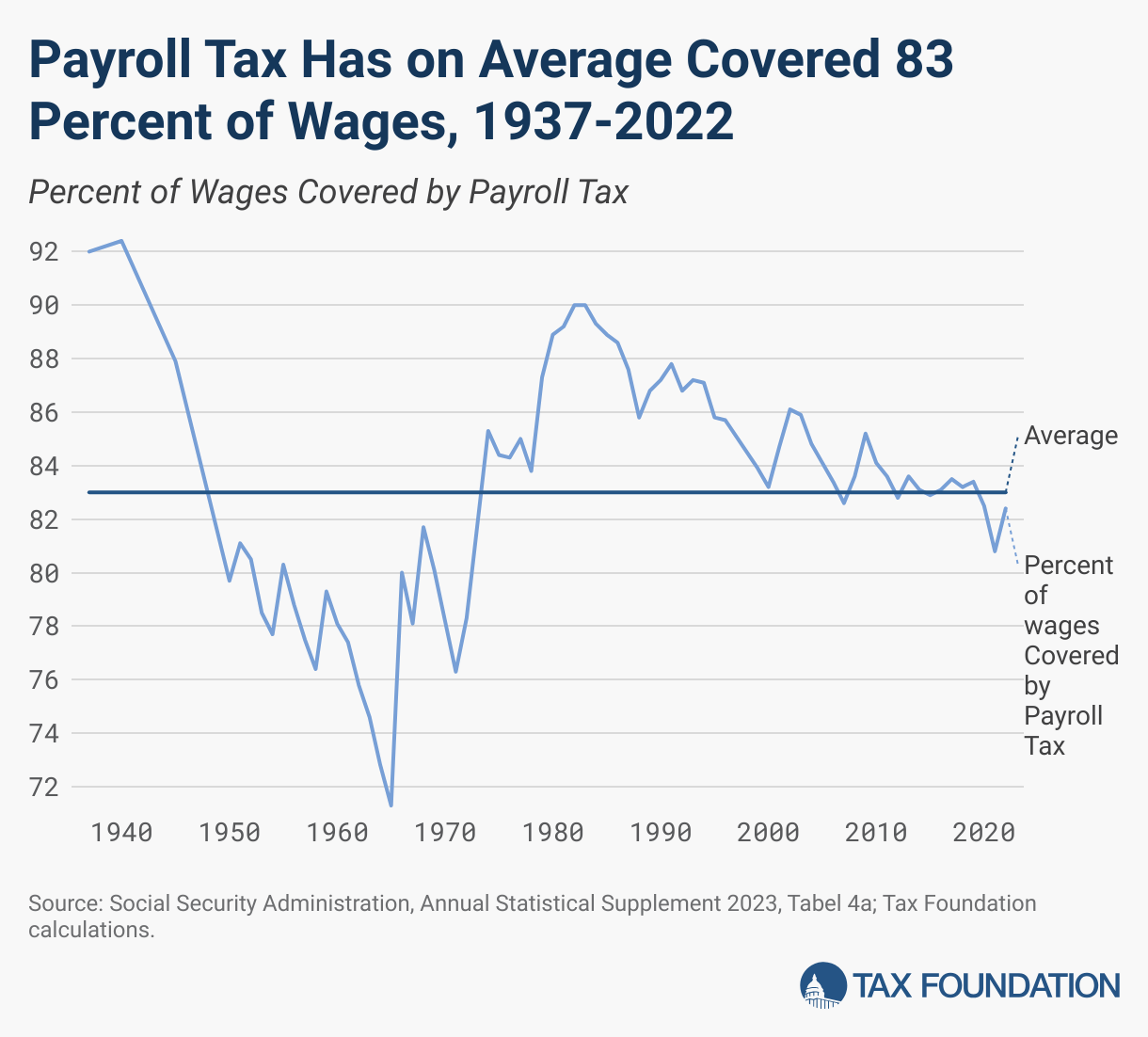

But even with the payroll cap rising to $160,000 today, the share of wages and salaries covered by the payroll tax has fallen to about 82 percent. The last time it reached as high as 90 percent was during the 1983 Social Security amendments, which increased the payroll tax to address the funding crisis that had occurred at the time. On average, the payroll tax has covered about 83 percent of wages since Social Security’s inception.

One underappreciated contributor to the decline in how much wage income faces the payroll tax is the rise in employee-provided fringe benefits, the largest of which is health insurance. Employer-provided health insurance is tax deductible, and thus faces neither the income nor payroll tax. Other fringe benefits exempt from income and payroll taxes include group-term life insurance, disability insurance, certain transportation expenses, contributions to health savings accounts, and business expense reimbursements for travel.

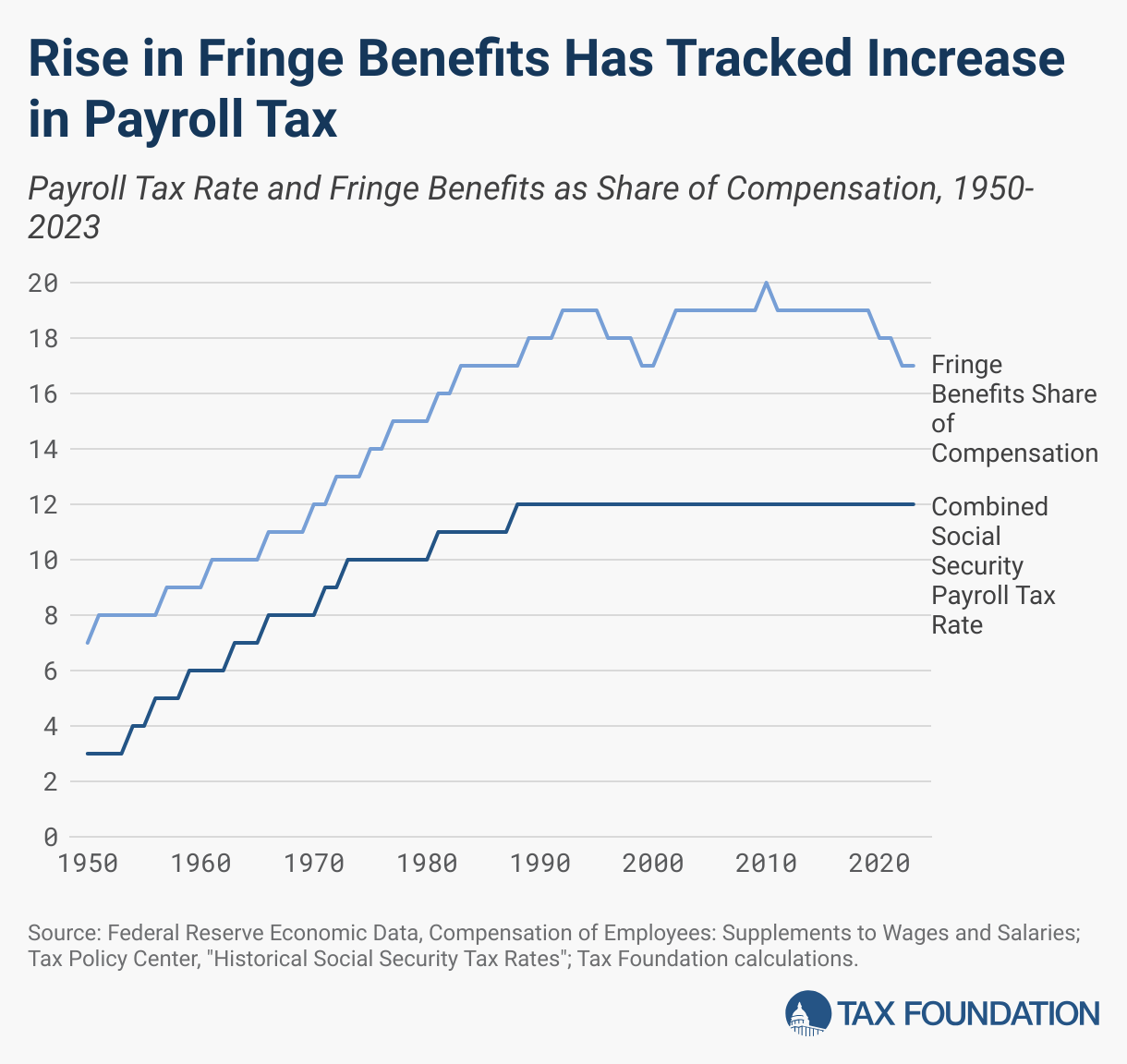

Fringe benefits grew from 7 percent of compensation in 1950 to 19.3 percent in 1993. Since then, the trend has somewhat flattened, generally hovering between 17 and 20 percent of total compensation. The trendline has generally tracked with the Social Security tax rate. The combined Social Security payroll tax rate, including both the employee and employer burden, rose from 3 percent in 1950 to 12.4 percent in 1990, where it has remained since.

Currently, Social Security faces a $3.5 trillion shortfall over the next decade. By 2035, the trust fund will be depleted, and current payroll taxes will only be able to fund 83 percent of the scheduled benefits. If policymakers were to eliminate the tax exclusion for employer-provided health insurance, for example, that alone would generate $5.0 trillion in additional tax revenue over the next decade on a conventional basis, in line with CBO estimates. About 28 percent of that, or $1.4 trillion, would be specifically payroll tax revenue.

While difficult choices will have to be made to restore fiscal solvency to Social Security, policymakers searching for ways to boost the trust fund revenues as part of some broader bipartisan reform might want to consider curtailing these various tax exclusions for fringe benefits.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share this article