You might receive Form 1099-S this year if you sold a house, some land, or another piece of property. But what does this form mean for your income tax return? Don’t worry — we’ll walk you through everything you need to know about this form, why you got it, and how to easily e-file it.

At a glance:

- Form 1099-S reports real estate transactions, which you must report on your tax return.

- The person or entity responsible for closing the sale fills out and sends Form 1099-S.

- Selling property doesn’t automatically mean you owe taxes, as you may qualify for an exclusion.

What is Form 1099-S?

Form 1099-S, Proceeds from Real Estate Transactions, reports the sale or exchange of real estate property to the Internal Revenue Service (IRS). This could include any of the following:

- Your main home or another residential building

- Developed or undeveloped land (including air space)

- Condominium units (including any fixtures or land)

- Commercial or industrial buildings

- Shares in a cooperative housing corporation

- Non-contingent interest in standing timber

Who sends Form 1099-S?

Depending on the specific transaction circumstances, different parties may be responsible for sending Form 1099-S. According to IRS instructions, the person responsible for closing the transaction should be the one to fill out the form. Often, this falls on the title company, escrow company, or mortgage lender who helped you close the transaction.

However, just because you sold a piece of property doesn’t automatically mean you owe taxes. Whether you’re on the hook depends on factors like the type of property, any exclusions you qualify for, and your overall capital gains.

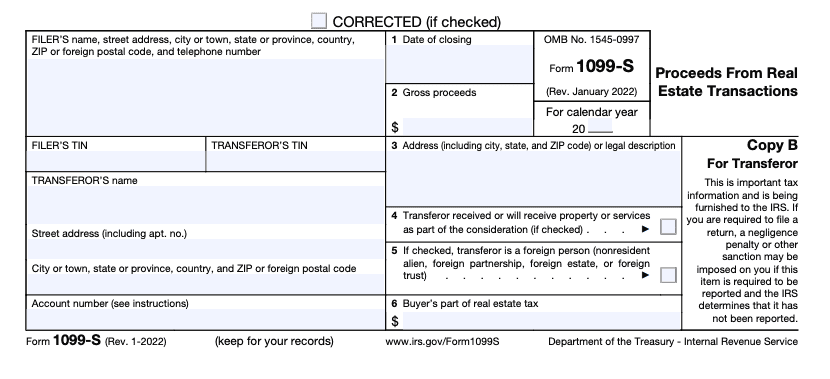

IRS Form 1099-S example

Form 1099-S looks like this:

On the left side of the form, you’ll find two types of contact information:

- The filer: This is the closing agent or entity that sent you the form. You’ll see their name, address, and taxpayer identification number (TIN).

- The transferor: As the seller, you are also known as the transferor. You’ll see your own contact info, account number, and TIN (often your Social Security number or SSN).

Here’s what the boxes on the right mean:

- Box 1: Date of closing – The date when the real estate transaction was finalized.

- Box 2: Gross proceeds – The total amount you received from the property sale.

- Box 3: Address or legal description – The property sold or transferred.

- Box 4: Non-cash consideration – If this box is checked, it means you received or will receive services or property other than cash or notes.

- Box 5: Foreign person – This box is checked if you (the seller) are a nonresident alien, foreign partnership, foreign estate, or foreign trust.

- Box 6: Buyer’s part of real estate tax – This box shows the remaining real estate tax to be paid by the buyer for the tax year. For instance, say you paid your real estate taxes for the rest of the year in advance but sold your main home at the end of October. The buyer would then be responsible for the final two months of tax payments, indicated in this box.

Instructions for Form 1099-S

Once you have your Form 1099-S, follow these steps to ensure you report it correctly:

- Determine if the transaction is reportable: First, find out if your real estate sale qualifies for any exclusions, like the home sale exclusion. TaxAct® can help you determine whether you have a reportable transaction by asking questions about the sale.

- Report your capital gains: If you have a reportable gain, you must fill out Form 8949 with information from your 1099-S. Then, you’ll need to complete Schedule D to officially report capital gains and losses. TaxAct can simplify this process by filling out the necessary tax forms for you step by step.

- Check for state-specific requirements: Some states have their own tax forms you need to file, so check with your state’s tax agency. TaxAct can also pull information from your federal income tax return to help streamline the e-filing of your state income tax return.

IRS Form 1099-S FAQs

Do all home sales get a 1099-S?

Not necessarily. If your sale meets the qualifications for the home sale exclusion, your mortgage lender or escrow company might not need to issue a Form 1099-S. The home sale exclusion allows you to exclude up to $250,000 ($500,000 for joint filers) in capital gains on the sale of your main home if you meet specific requirements. Check out our FAQ page if you’re unsure whether the sale of your home is reportable.

Who is exempt from 1099-S?

The IRS has a detailed list of exceptions for Form 1099-S. If the transaction meets any of these exceptions, it does not need to be reported. For example, certain transactions, like gifts of real estate or transfers to satisfy a debt, might be exempt from the Form 1099-S requirements. You can view the full list of exceptions on the IRS website.

How do I report a 1099-S on my tax return?

If necessary, you’ll report the sale on Schedule D and the specific details on Form 8949. TaxAct will walk you through the process to help you report the details of the sale (see the next section).

How to file Form 1099-S with TaxAct

You can report your real estate proceeds in TaxAct using various methods depending on the type of property you sold.

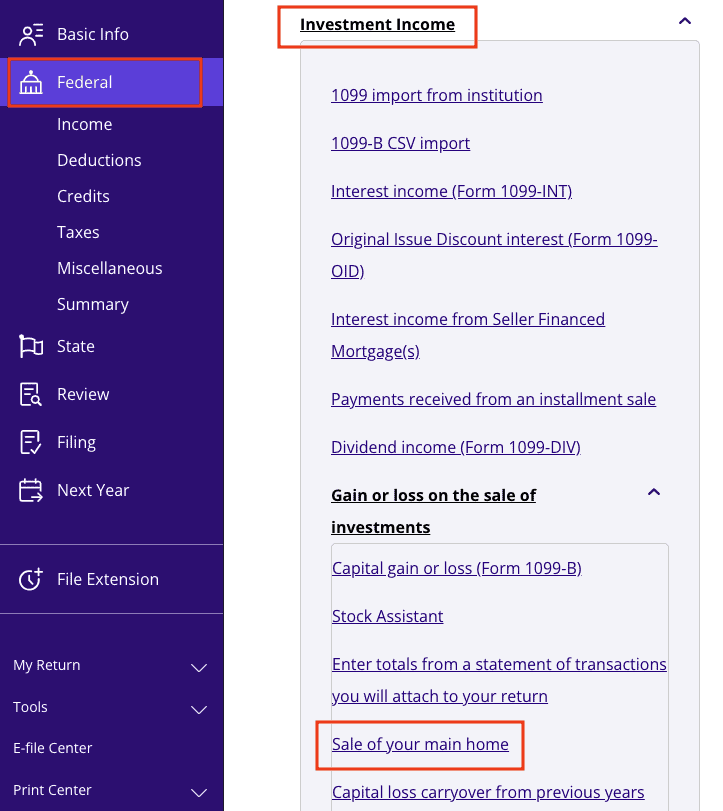

Sale of your main home:

- From within your TaxAct return (Online or Desktop), click Federal (on smaller devices, click in the top left corner of your screen, then click Federal).

- Click the Investment Income dropdown, click the Gain or loss on the sale of investments dropdown, then click Sale of your main home.

3. Continue with the interview process to enter your information.

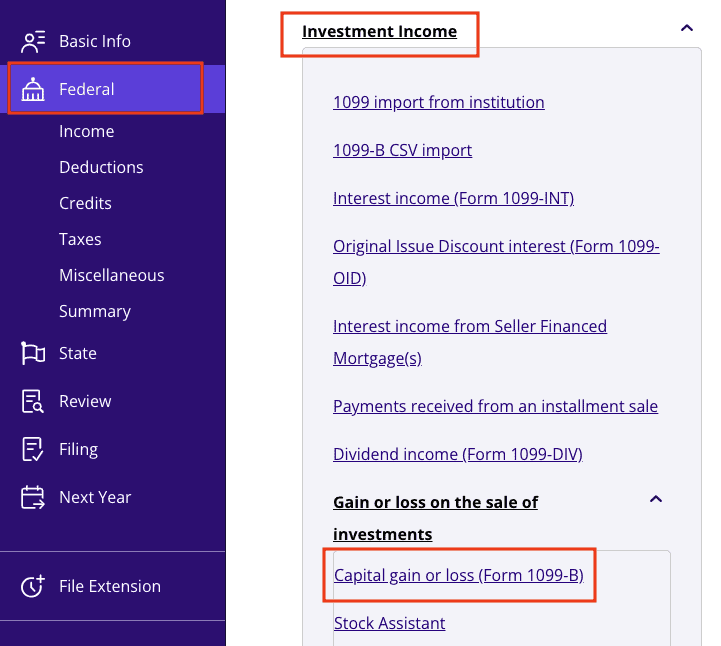

Sale of a timeshare, vacation home, or investment property:

A timeshare or vacation home is considered a personal capital asset and should be reported on Schedule D for Capital Gains or Losses. If you profit from selling it, you must report it as income. However, if you experience a loss from the sale, the IRS does not allow you to deduct that loss.

If you inherit a property that is considered an investment property, any capital gain or loss should be reported on Schedule D. If you incur a loss, the IRS will expect the sale to be reported on your return. In this case, you should enter a cost equal to the sale price so that the reported gain/loss is zero (0).

To report the sale of your vacation home, timeshare, or investment property in TaxAct:

- From within your TaxAct return (Online or Desktop), click Federal (on smaller devices, click in the top left corner of your screen, then click Federal).

- Click the Investment Income dropdown, click the Gain or loss on the sale of investments dropdown, then click Capital gain or loss (Form 1099-B).

3.Click + Add Form 1099-B to create a new copy of the form or click Edit to edit a form already created (desktop program: click Review instead of Edit).

4. Continue with the interview process to enter your information.

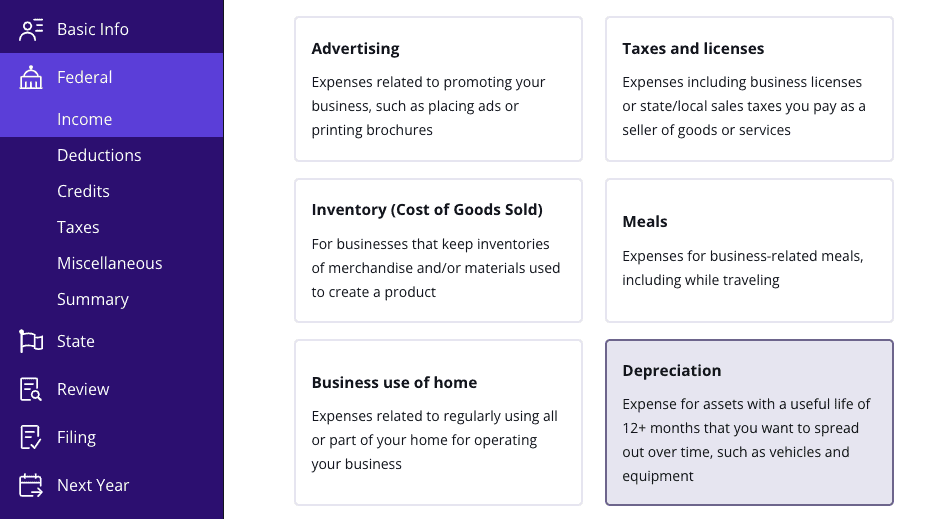

Sale of business property (reportable on Form 4797 and Schedule D):

- From within your TaxAct return (Online or Desktop), click Federal (on smaller devices, click in the top left corner of your screen, then click Federal).

- Click the Business Income dropdown, then click Business income or loss from a sole proprietorship (or Farming income or loss, if applicable).

3. Continue with the interview process until you reach the screen titled Here are some of the most commonly used expenses. Select Depreciation from the list as shown below.

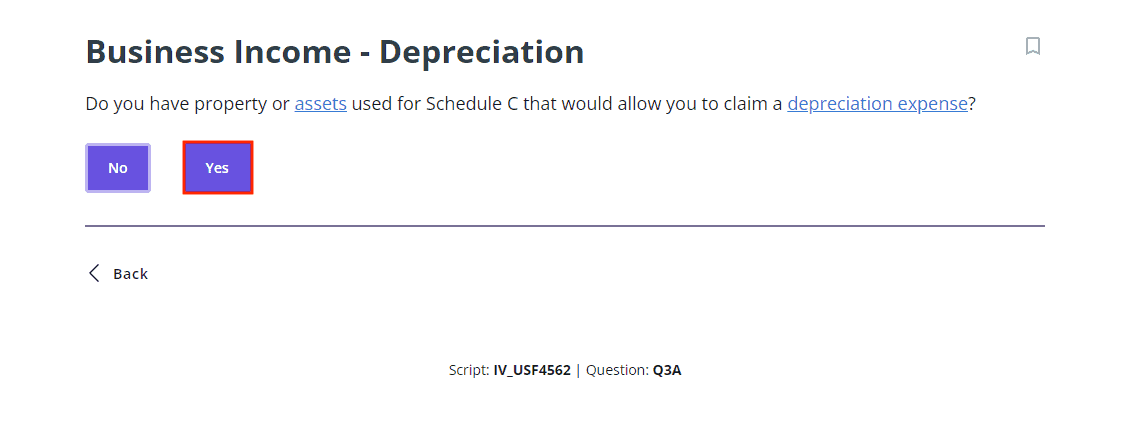

4. On the page titled Business Income – Depreciation, click Yes to the question shown below.

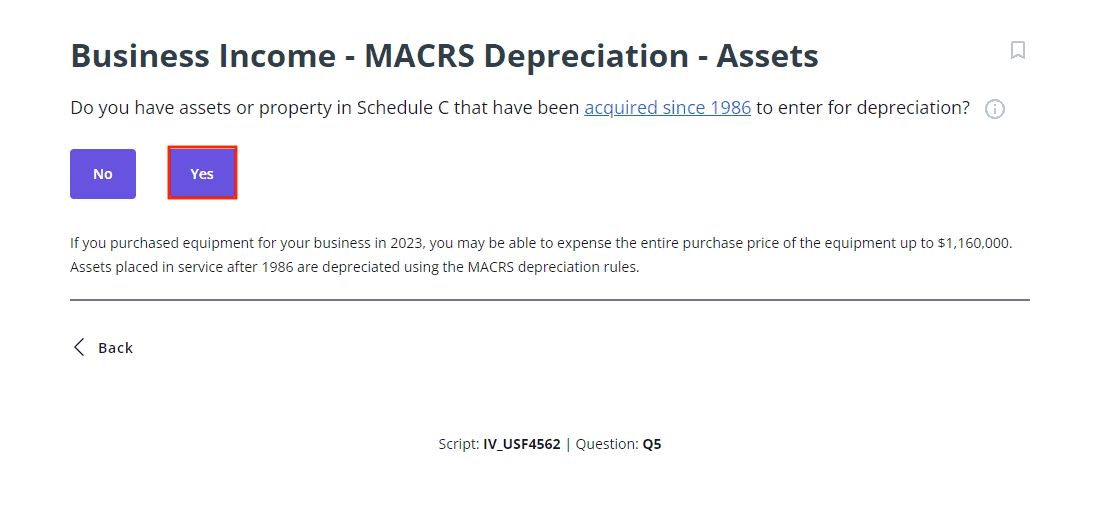

5. On the screen titled Business (or Farm) Income – MACRS Depreciation – Assets, click Yes as shown below.

6. Click Step-by-Step Guidance and continue with the interview process to enter your information.

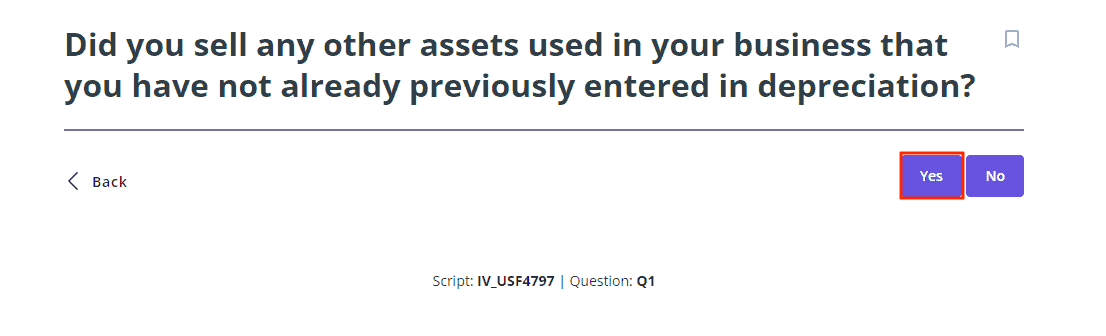

Sale of business property (if the property never depreciated):

- Follow the steps for reporting the sale of business property in the previous section. After entering any depreciation and expenses, you’ll come to the screen shown below. Click Yes.

2. Continue with the interview process to enter information for the asset that you sold.

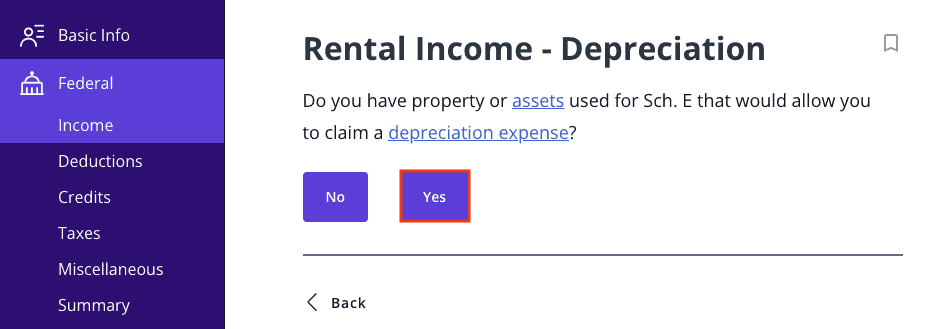

Sale of rental property (reportable on Form 4797 and Schedule D):

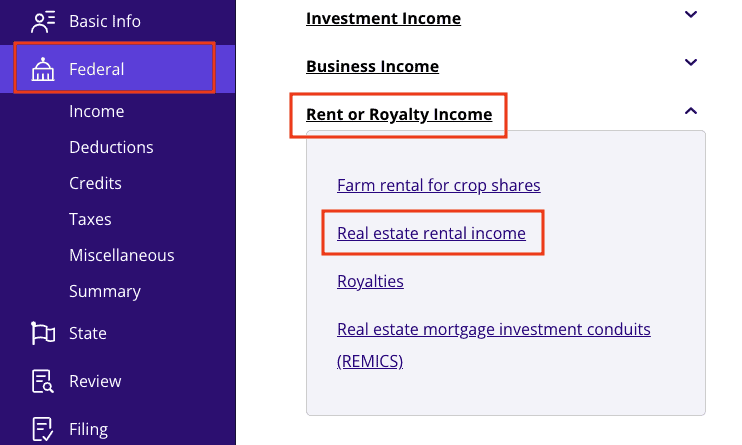

- From within your TaxAct return (Online or Desktop), click Federal (on smaller devices, click in the top left corner of your screen, then click Federal).

- Click the Rent or Royalty Income dropdown, then click Real estate rental income.

3.Click + Add Schedule E, Pg 1 to create a new copy of the form or click Edit to edit a form already created (desktop program: click Review instead of Edit).

4. Continue with the interview process until you reach the screen titled Rental Income – Depreciation as shown below, then click Yes.

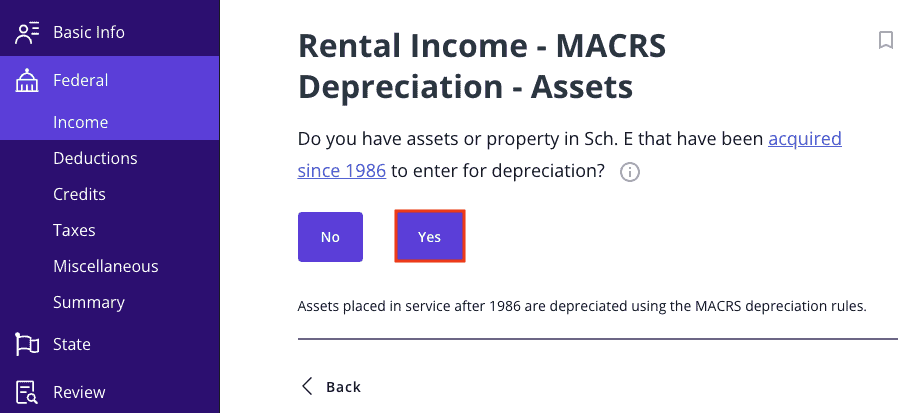

5. On the screen titled Rental Income – MACRS Depreciation – Assets as shown below, click Yes.

6. Click Step-by-Step Guidance, and continue with the interview process to enter your information.

The bottom line

Form 1099-S doesn’t have to be intimidating. Whether it’s your first time filing or you’re a seasoned DIY tax filer, knowing what this form means and how to report it can save you stress and headaches during tax filing season. And as always, when you file with TaxAct, you can rest assured we’ve got the tools you need to tackle your 1099 forms without breaking a sweat.