Competition between the United States and China has become a central theme in American policy discussions, from recently enacted legislation like the CHIPS and Science Act to policy recommendations from the Select Committee on the Strategic Competition Between the United States and the Chinese Communist Party. Economic competition is undeniably connected to broader geopolitical competition, but it makes sense to draw a distinction between economic competition with China and security competition with China with an economic component. For the former, tax policy is one of many relevant policy areas.

Broad, pro-investment taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

policy matters for growth, and the US has plenty of opportunities to make improvements, particularly given the advantages our cross-Pacific rival confers on its firms.

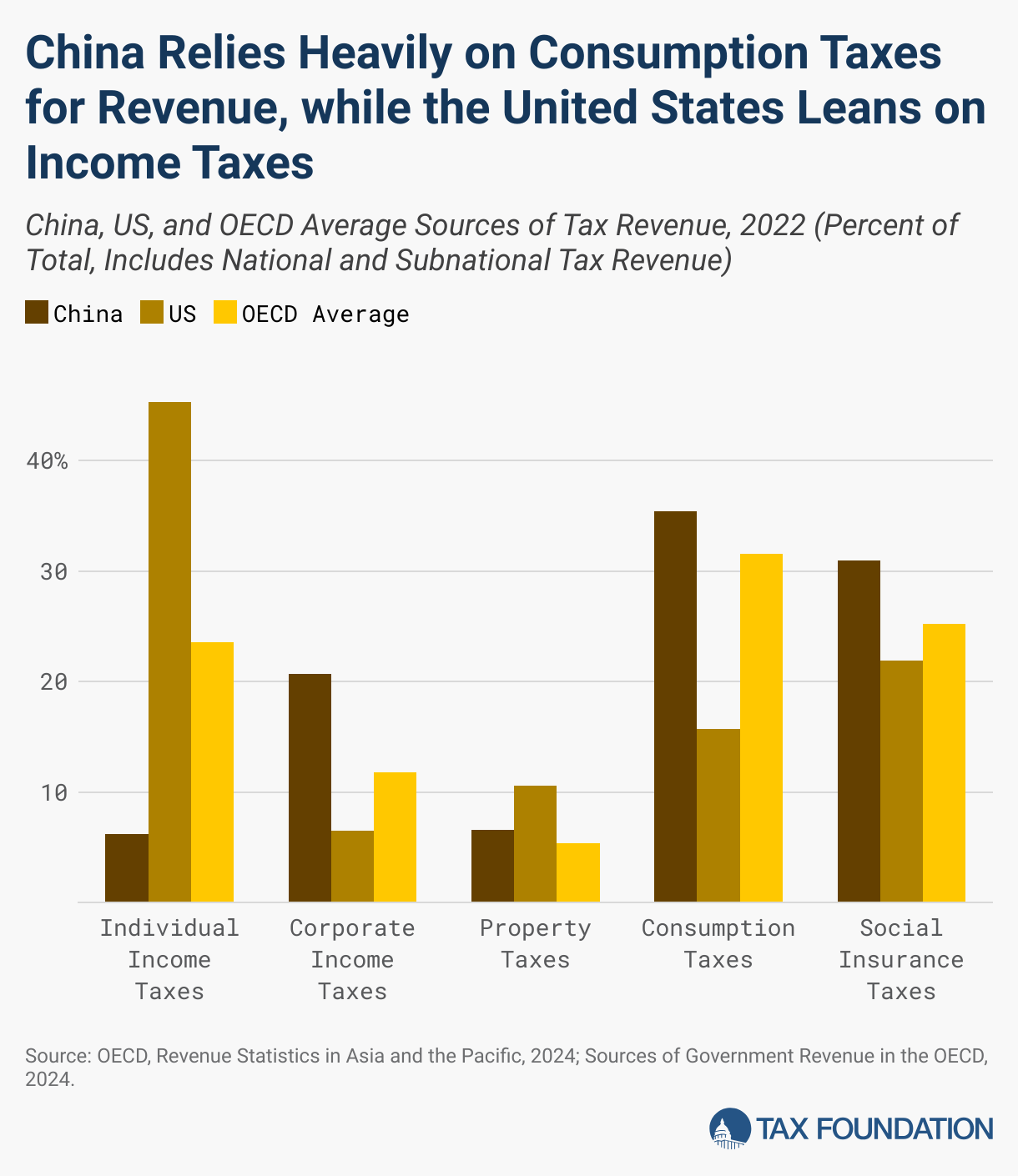

The first point to consider is the tax mix. How a country raises revenue matters: an extensive economic literature suggests well-structured taxes on property and consumption are less harmful for economic growth than taxes on income, particularly corporate or business income. China’s high reliance on consumption taxes is more economically sound than the US’s reliance on personal income taxes, although the US does lean more on property taxes than China.

But beyond the revenue mix, tax design matters. That is particularly true of the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

.

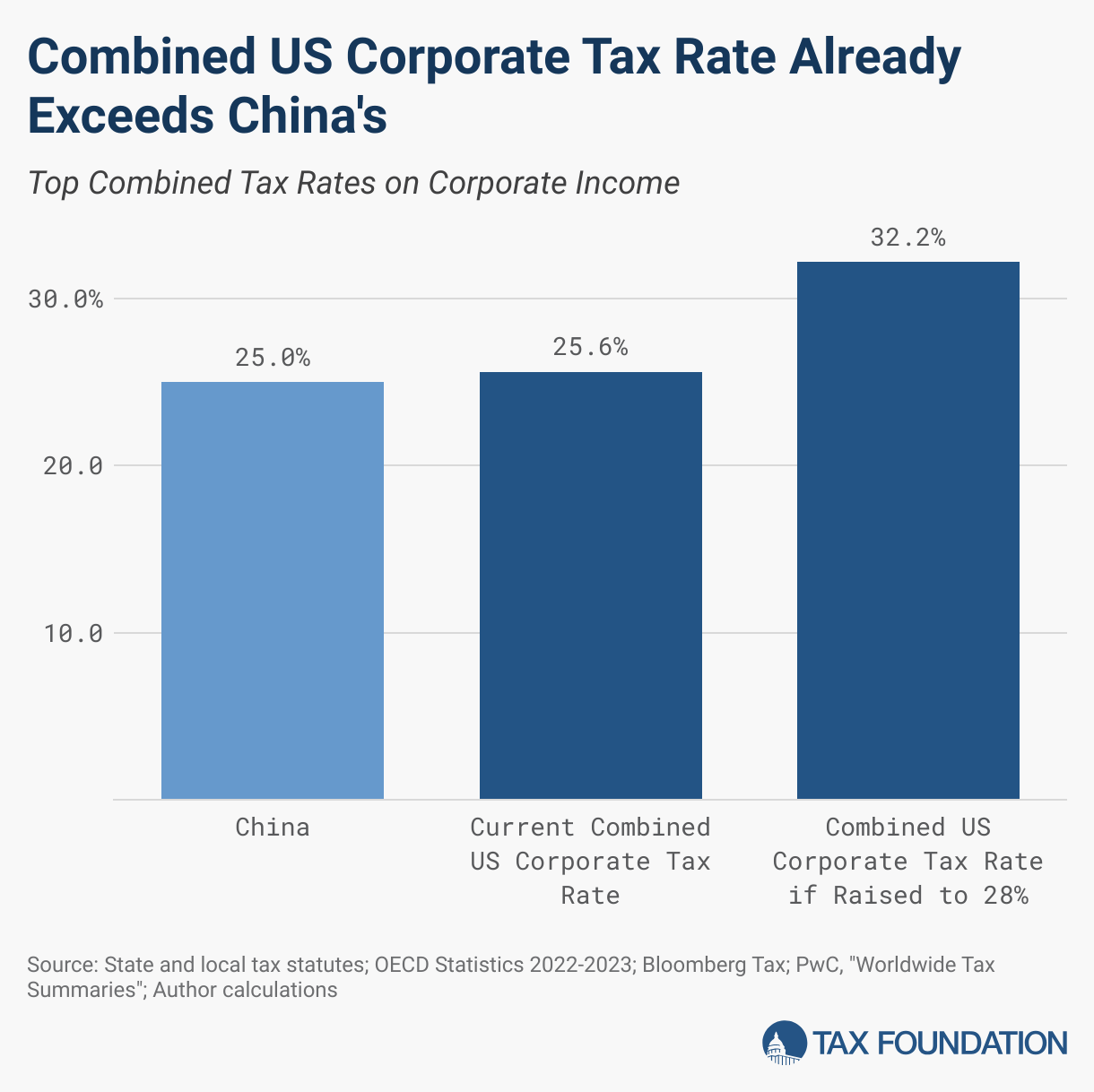

Corporate tax rates are similar in China and the US today. The US has a 21 percent corporate tax rate at the federal level, while China has a national corporate tax rate of 25 percent. However, many US states levy corporate taxes of their own, bringing the average US corporate tax rate to 25.8 percent, slightly higher than the Chinese rate. Chinese subnational jurisdictions, on the other hand, do not levy corporate income taxes of their own, and the Chinese government provides either reduced tax rates or full tax exemptions for specific industries, sometimes across the whole country, and sometimes in specific regions.

The corporate rate is not the whole story though. The deductibility of investment costs is just as, if not more, important than the tax rate.

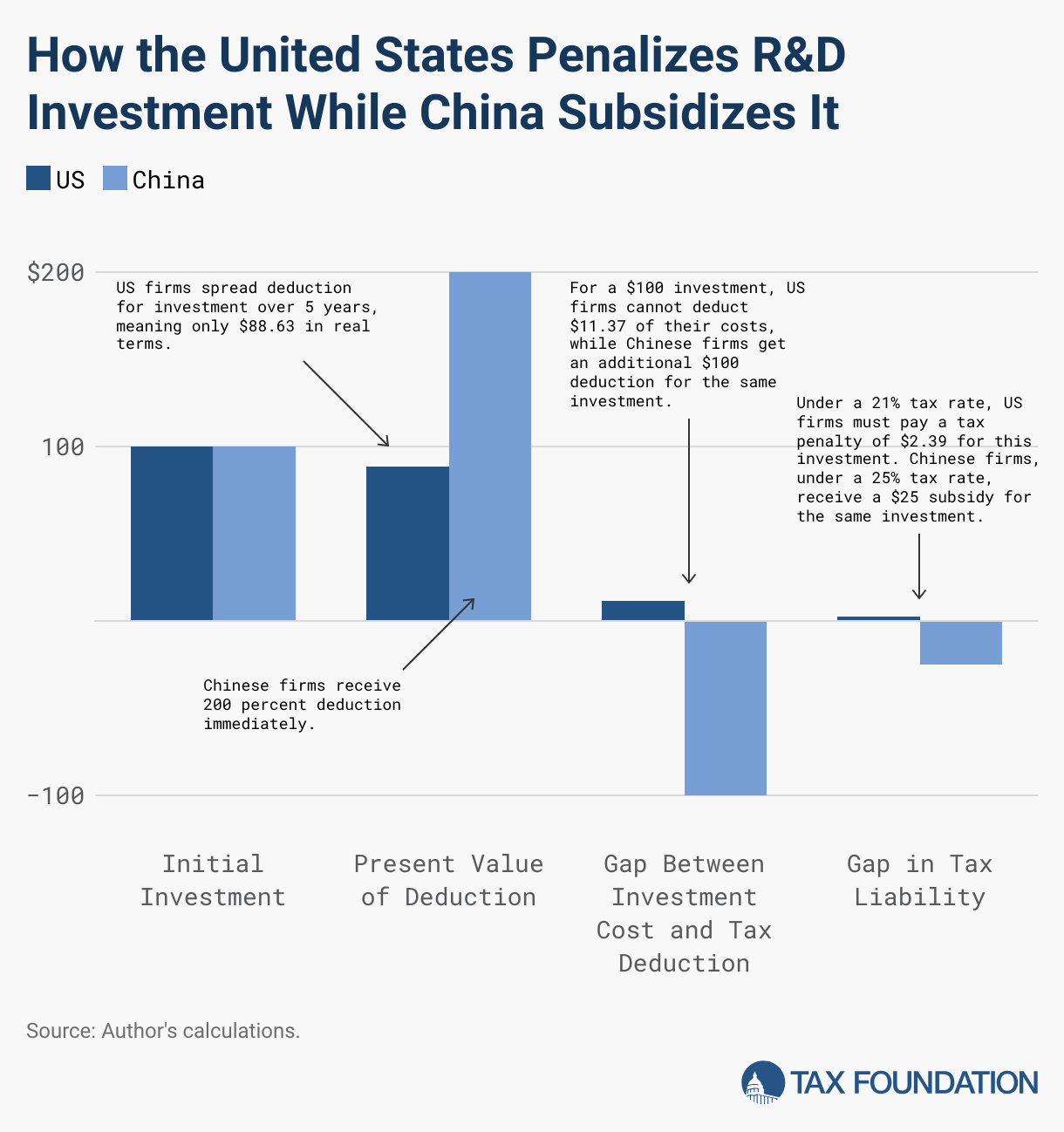

China has a substantial edge over the US in this regard. Chinese firms spread deductions for physical assets out over between 3 and 20 years, while US firms must spread deductions out over between 3 and 39 years. Longer asset lives mean US companies cannot deduct as much of the cost of property, plant, and equipment as their Chinese counterparts, penalizing investment in the US economy.

The gap is even more substantial in research and development (R&D) investment. Under the policy of R&D amortization, US companies must spread deductions out over 5 years for US R&D investment and 15 years for R&D investment made abroad. China, meanwhile, allows (almost) all companies to deduct 200 percent of their R&D investment costs, in effect creating a 25 percent subsidy for R&D.

A few key fixes to the tax treatment of capital investment could resolve the competitive disadvantages US firms face. While subsidizing R&D investment as aggressively as China does comes with its own problems, returning to R&D expensing would erase the strange tax penalty for R&D we have introduced. On physical investment, we could fully and permanently restore 100 percent bonus depreciationBonus depreciation allows firms to deduct a larger portion of certain “short-lived” investments in new or improved technology, equipment, or buildings in the first year. Allowing businesses to write off more investments partially alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

, a policy introduced in the Tax Cuts and Jobs Act of 2017 that allows companies to immediately deduct the cost of short-lived physical assets, mostly equipment and machinery.

Lastly, for long-lived assets like structures, neutral cost recovery is a strong option. Under neutral cost recoveryCost recovery is the ability of businesses to recover (deduct) the costs of their investments. It plays an important role in defining a business’ tax base and can impact investment decisions. When businesses cannot fully deduct capital expenditures, they spend less on capital, which reduces worker’s productivity and wages.

, investing firms would still spread deductions out over the course of an asset’s life, but they would adjust deductions for both inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

and a risk-free rate of return, which would be economically equivalent to immediate expensing. Another advantage of neutral cost recovery is that it avoids the large, frontloaded transition cost incurred by moving to full expensingFull expensing allows businesses to immediately deduct the full cost of certain investments in new or improved technology, equipment, or buildings. It alleviates a bias in the tax code and incentivizes companies to invest more, which, in the long run, raises worker productivity, boosts wages, and creates more jobs.

.

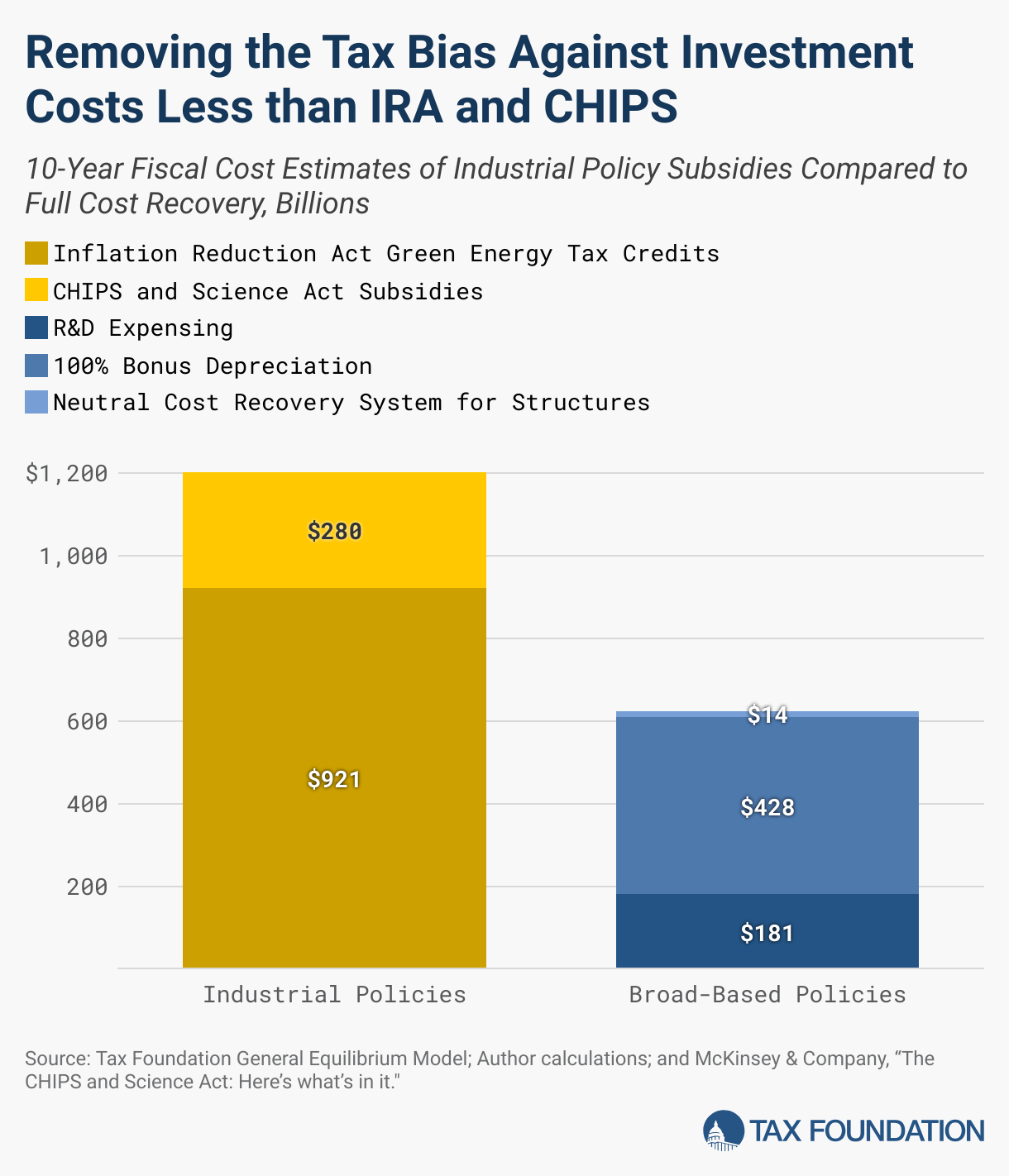

Over the long run, allowing full cost recovery would boost economic output by 1.7 percent, the capital stock by 3.3 percent, wages by 1.5 percent, and employment by 381,000 full-time equivalent jobs. This policy package would reduce federal revenue by $623 billion over the next decade, which is substantial, but ultimately smaller than the combined cost of the Inflation Reduction Act energy credits and the CHIPS and Science Act.

Focusing on pro-investment incentives is also more economically sound than using tariffs. On the campaign trail, candidate Trump has suggested universal tariffs on all imports to encourage more manufacturing and domestic investment, a dramatic expansion on the narrower tariffs imposed during his first administration. The economics of tariffs are very clear—they redistribute activity across sectors while reducing productivity and output overall. Though some sectors may benefit from protection in the short run, in the long run, tariffs harm US workers and manufacturers. Cutting trade ties with allies and creating a protected market for domestic firms to sell into will make it harder for workers to afford their current standard of living, slow innovation, and dull the competitive forces that lead to long-run technological improvement. Tariffs are not a good tool to encourage productive domestic investment or broad economic growth.

Now, a broad, pro-investment agenda may not be a complete answer to industry-specific economic security challenges. Some policymakers and analysts have called for the US to develop overcapacity in specific critical industries. Expensing for capital investment will not create overcapacity, as it is not a subsidy. However, it can alleviate undercapacity across the economy. Furthermore, while targeted policy may be needed for specific security purposes, those policies should not be mistaken for an economy-wide plan for growth.

US policymakers are aware of these competitiveness concerns. For example, Speaker of the House Johnson highlighted the benefits of better cost recovery in recent remarks, and lawmakers have introduced bipartisan legislation to restore deductions for R&D expenses as well as 100 percent bonus depreciation. However, most proposals would only restore deductions temporarily, which saps their impact on long-run growth. Ideally, lawmakers should make a permanent fix—sooner rather than later.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share this article