Key Findings

- Property values have skyrocketed in recent years, rising almost 27 percent faster than inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

since 2020, which yields dramatically higher property taxes in jurisdictions that fail to adjust millages (rates) downward. - Legitimate discontent over high property taxes is fueling a movement to significantly curtail or even eliminate the property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services.

, but many of the policy solutions offered, like assessment limits and taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

swaps, create more problems than they solve, distorting property markets and undermining long-term housing affordability. - Despite its unpopularity, the property tax is relatively economically efficient, and shifting to any alternative tax would harm economic growth.

- Well-designed levy limits can provide homeowners with much-needed relief from soaring property tax bills without the harms associated with other policy responses, and narrowly tailored circuit breakers can help ensure that low-income families are not priced out of their homes.

- The property tax is a tax worth saving—and therefore worth reforming. Policymakers should work to constrain the runaway growth of property tax liability witnessed in some parts of the country but should not overcompensate by eliminating or dramatically curtailing an economically efficient tax.

Introduction

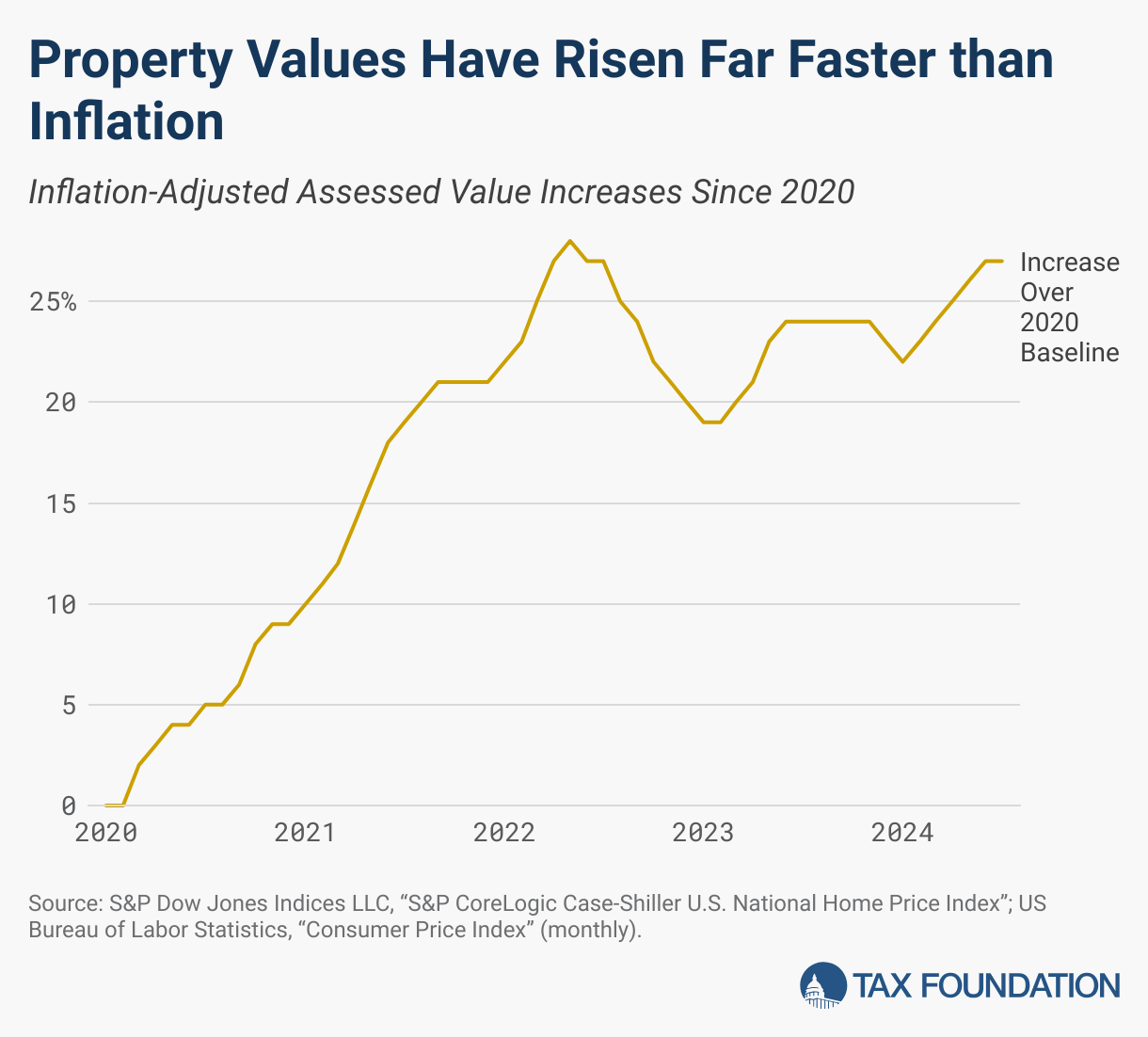

The value of a typical single-family home in fast-growing Bozeman, Montana, or Boise, Idaho, has doubled in seven years.[1] Early in the pandemic, the average sales price of a home in the United States was $371,100. Two years later, it had soared to $525,100—a 41 percent increase—before leveling off slightly.[2] Between January 2020 and July 2024, aggregate US home prices soared 54.4 percent in nominal terms,[3] rising considerably faster than income or inflation. In real (inflation-adjusted) terms, homes increased in value by 26.7 percent in four and a half years—a fine return on investment, but a disquieting development when property taxes come due.

Many jurisdictions across the country have rolled back millages (property tax rates) to avoid or at least limit unlegislated tax increases. Sometimes these rollbacks have happened automatically, and other times they have reflected a decision by local elected officials. But that has not happened everywhere. In cities and counties across America, many homeowners face dramatically rising property tax burdens even though nothing about their property has changed.

They are upset, understandably. And their discontent is fueling a new property tax revolt, with flashpoints in North Dakota (where a proposal to repeal the property tax made the ballot), Nebraska (where a repeal measure missed the ballot but the tax’s evisceration was debated in special session), Wyoming (where the legislature passed a virtual elimination of the tax on residences, but drew a gubernatorial veto), and elsewhere.

The historical record is murky on the origins of property taxes,[4] but this much is almost certain: the first property tax was proceeded almost immediately by the first complaint about property taxes. Taxing property is nearly universal—it is taxed in all 50 states and in nearly every country[5]—and, with only slight exaggeration, nearly universally reviled by those who pay the tax. More than any other major tax, the property tax generates a visceral response.

The grievances are often legitimate, and in many cases, reforms are warranted. The proposed solutions—severely carving up or even eliminating the tax—are, however, considerably worse than the status quo, for all its flaws. That the property tax endures despite millennia of discontent is a testament not only to its importance but also to its insufficiently acknowledged virtues. But today, in at least some states, its future is in doubt.

The property tax is not a perfect tax, and there are ways to improve it, but it is better than the alternatives. It is a tax worth saving—and therefore worth reforming. This paper makes the economic case for the property tax, evaluates the trade-offs associated with common proposals to reform or curtail it, and highlights one approach (well-designed levy limits) that stands head and shoulders above the rest as a responsible way to deliver relief to genuinely aggrieved homeowners without distorting housing markets or undercutting economic growth.

The Case for Property Taxes

The title of a 1996 book on the history of property taxes in America posed a question: The Worst Tax?[6] (The author, Glenn Fisher, answered his own question in the negative.) Two decades later, Joan Youngman of the Lincoln Institute of Land Policy delivered her own verdict, without the question mark: A Good Tax.[7] For local governments across the country, the verdict has simply been that it is a necessary tax. But are Fisher and Youngman right, that, far from being the worst tax, the property tax is actually a good tax? As it turns out, yes.

The basic case for property taxes rests on the following premises, which are well-supported by the economic literature:

- Property taxes do less economic harm than alternative ways to raise the same amount of revenue, making them more economically efficient than the alternatives.

- Property taxes have less of an effect on decision-making—including location decisions—than most other taxes, making them less distortionary than the alternatives.

- Property taxes roughly align with the benefits that property owners receive from local services, making them more equitable than the alternatives.

- Property taxes are highly transparent and correlate strongly with services that enhance the value and utility of property, making them unusually sensitive to local preferences on the size and scope of government.

Each assertion must be defended and expanded upon. None of them, moreover, is a justification for runaway property taxation. But here’s the gist of it: compared to other taxes, property taxes do a good job of aligning tax burdens with the value property owners get from local expenditures, and they are much more economically competitive and pro-growth than revenue sources that might displace them.

Growing discontent with rising property tax burdens does not negate the point that property taxes are better aligned with local preferences—quite the contrary. To be sure, property tax systems are far from perfect, and better mechanisms can and should be adopted to preclude unlegislated tax increases. But more than that, the discontent reinforces one of the benefits of funding local government through property taxes.

Very few taxpayers have any sense of what they pay in sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding.

. Even income tax payments, typically withheld over the course of the year, are not always front of mind. But virtually every homeowner knows what they pay in property taxes and can evaluate whether they believe that local services—including potential increases in their cost or provision—are justified by their tax bill. When property owners perceive a misalignment, as many do now, they are stirred to action. The present discontent is not an argument against property taxes. It is evidence that the transparency of property taxes, and the degree to which they are aligned with local services that broadly benefit those paying them, enables accountability mechanisms that are virtually nonexistent with other taxes.

But it’s one thing to say that the property tax is a good tax, and it’s another to demonstrate it, especially against common objections that deserve to be taken seriously. Let’s dig in.

Property Taxes Are Comparatively Pro-Growth

Taxes themselves never create economic growth; it’s only a question of how much they impede it. Government spending, on the other hand, can facilitate growth—but then it’s a question of how much, and whether the tax revenue funding it would have been better spent in the private sector. These are difficult questions, and the appropriate balance is both heavily disputed and beyond the scope of this paper, particularly since economic growth is far from the only legitimate priority.[8]

For our purposes, however, we only need to accept two almost universally accepted assumptions: (1) taxes impose economic costs, but not all taxes impose the same cost per dollar raised; and (2) government spending can yield economic benefits, but not every dollar spent yields the same economic benefit.

Economic analysis consistently finds that property taxes are better for economic growth than income or sales taxes. We will review the empirical evidence first, then dive into the explanations for it.

In a study spanning 21 Organisation for Economic Co-operation and Development countries across more than three decades, researchers concluded that a 1 percentage point shift from income taxes to consumption taxes (like sales taxes) improves GDP by 0.74 percent, while shifting to property taxes increases GDP by 1.45 percent.[9] Similarly, an International Monetary Fund working paper determined that a 1 percentage point shift from income to consumption taxes increases GDP by 0.92 percent, while a shift to property taxes yields a 1.22 percent GDP improvement. Even more notably, this study also drilled down to taxes on immovable property, and a 1 percentage point shift from taxes on income to taxes on immovable property grew GDP by 2.47 percent.[10]

Regional studies find complementary results. Using data from Indiana, one study explored wholesale replacement of the property tax with an income or sales tax, finding that gross state product would decline by 2.8 percent when an income tax replaced the property tax and by 2.7 percent under a shift to a sales tax. Household disposable incomes would decline by about 3.5 percent under either shift.[11]

Another study, focused on the DC metro area, found that a 1 percentage point higher rate on the sales tax reduced employment growth by 2.08 percent, but that a similar increase in property tax rates—including on commercial property—was associated with modestly increased rates of employment, with results suggesting that the services provided by higher property taxes (including school quality) were valued by businesses commensurate with the additional property tax costs, whereas the higher sales tax rate had business costs exceeding benefits.[12]

Still other studies deal in hypotheticals or stylized questions, with research finding extremely large positive effects from shifting from income taxes on mobile capital to a tax on land value,[13] which is useful in developing our theoretical understanding of why property taxes are comparatively pro-growth, but does not quite simulate real-world conditions, as income taxes fall on more than just mobile capital and virtually all property taxes fall on structures as well as land.

But this gets us into the reasons why property taxes are so economically efficient compared to other taxes. Real property taxes fall on land and improvements. Land itself is a fixed asset; the supply of land does not change with property taxes. An income tax, by reducing the returns to labor and investment, has a negative effect on labor force participation, productivity, and capital formation. A tax on land cannot, by contrast, decrease the amount of land.

At the margin, of course, property taxes can affect how much land can be used productively. Specifically, they may impact the capital invested in improving the land—irrigating arid land to make it suitable for crops, say, or building a house or an apartment complex on it rather than leaving it vacant or putting it to some lesser use. But the part of the property tax that falls on the land itself creates extremely few distortions.

Even where the improvements are concerned, research suggests that property taxes do relatively little to distort economic decision-making, since (unlike income or sales taxes) the tax does not penalize productivity or consumption. Those taxes reduce incentives to work, invest, or consume. The property tax does none of those things, at least not to the same degree. There are fewer elasticities—an economic term for the responsiveness of quantity supplied or demanded to other factors, including tax costs—and thus fewer deadweight losses from property taxes, because property is not quickly or easily added or removed.[14]

It is unsurprising that property taxes are more pro-growth than income taxes, as the effects of income taxation on economic growth are well-documented.[15] It may be more surprising that property taxes also perform better than sales taxes, since economists generally regard consumption taxes as a relatively neutral form of taxation.

This is true—for well-designed consumption taxes. In the US, however, property taxes (however flawed) diverge from their ideal considerably less than sales taxes do. A sales tax that fell exclusively on final consumption would be much more competitive with property taxes, but actual sales taxes in the US exempt vast swaths of final consumption while inappropriately taxing many intermediate transactions (business inputs), turning them at least partly into a tax on in-state capital investment and leading to tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action.

, where the tax is imposed several times over on the same good or service.[16]

Notably, the two international studies referenced above, which found property taxes more pro-growth than consumption taxes, are thus likely an understatement of the preference for property taxes, since most of the countries studied have better consumption taxA consumption tax is typically levied on the purchase of goods or services and is paid directly or indirectly by the consumer in the form of retail sales taxes, excise taxes, tariffs, value-added taxes (VAT), or an income tax where all savings is tax-deductible.

systems than the US, with far less tax pyramiding.[17]

Property Taxes Align with Benefits

Economists have proposed several models for understanding the incidence and effects of property taxes, but two views predominate: the “capital tax view” and the “benefits view.”[18] Increasingly, there’s a recognition that these views are not at odds with each other but are both necessary to understand the effects of property taxes.[19]

This is not the place to get into the weeds of a nuanced economic debate, but it is helpful to have a basic understanding of the two concepts. Essentially, one view sees the property tax mainly as a tax on capital investment in property, while the other view sees it as primarily a charge for benefits provided to property.

At some level, higher property tax rates reduce the return to capital investment and will thus yield less of it. If a jurisdiction decides to impose excessively high property taxes, that might disincentivize a property owner from pouring resources into further developing the land. But at reasonable levels, these responses will be muted—in part due to an effect called “capitalization.”[20] All else being equal, when property taxes rise, this reduces the value of the property. (All else is not equal: at least up to a certain point, the benefits of additional government spending might outweigh the increase in property taxes, but more on that in a minute.)

This “discount” in the price means that a prospective future buyer won’t be turned away by the tax rate, because it is already priced in. Conversely, a tax cut will benefit the current owner but won’t do as much to make the property more attractive to a future buyer, because they will now have to pay more to acquire it. This is a relatively positive feature of property taxes, because capitalization means that property taxes have less of an effect on migration decisions than other taxes.

But capital taxation is only half the story, if that. Whereas federal and state taxes fund many programs that provide no direct benefit to those remitting the taxes (which is simply the reality, and not a judgment on the value of those expenditures), most local government expenditures—roads, schools, police, emergency services, parks, waste management, etc.—have a direct bearing on the quality of life of property owners, and often enhance the value of property. Businesses do not have children, but benefit from good schools, as do childless homeowners who not only enjoy the broad social benefits of a jurisdiction with a quality education system, but also see their home appreciate in value because it is in a good school district.

Under the benefit view, property owners aren’t paying tax on their capital so much as they are paying for a set of services provided to their property.[21] This doesn’t mean they desire or benefit proportionally from every local government expenditure, any more than a person who purchases an insurance plan would have designed its coverage exactly the way it’s offered or a homeowner in an HOA would have selected each service the HOA provides. Still, the property owner is essentially paying for a bundle of services to that property, and to a certain extent, owners will self-sort based on the level of services they want.[22] For all the practical objections that can be raised to this—moving is neither easy nor costless, after all—it is undeniably true that the benefits funded by property taxes align with the value of a given property far better than under almost any other system, at any other level of government.

The value of your home is a far better proxy for the benefits you receive from local government than your income or how much you consume. And the services provided by local governments are much more proportional to taxes paid, especially under a property tax, than the services provided by state and federal governments.

A common objection to property taxes is that they’re never “paid off”—that, the thinking goes, one never really owns their own home because they will always owe property taxes. Consider a thought experiment. Imagine a new community is formed in a place without government services. The best thing to do, presumably, is form a government, because some services are best provided or at least funded by governments. But if this were impossible for some reason, the private sector certainly can provide roads, schools, security services, firefighters, and the like. Imagine that homeowners enter contracts for some of these services, paying premiums for police and fire protection, or paying to ensure that their home is on the road grid. Would they value these services, and expect to pay for them, even though they already paid for their home? And would they, in fact, potentially value them more highly if their home has a higher value?

Crucially, when property taxes roughly align with benefits received—and in fact often reinforce the value and desirability of a property—that makes them not only equitable but also relatively non-distortionary. If the property tax is mostly a capital tax, then it has the potential to discourage new capital investment. But if it’s mostly a benefit tax, then much of the cost of the tax will redound to the property owner in benefits.

Both are true, and they complement each other. At some level, higher property taxes do discourage additional investment (how could it be otherwise?), but the sensitivity is much lower than it is for other taxes, and it’s further ameliorated by the degree to which the tax is aligned with benefits received.

Is it perfect? Of course not. But the comparison isn’t a world where taxes don’t exist, or where everyone only pays exactly the amount at which they value the benefits they receive from government services. The comparison is income and sales taxes, and against these two alternatives, the property tax excels.

One more thing: research also finds that tax differentials seem to meaningfully affect prices in densely populated areas, while they have more of a quantity response in more rural areas. This makes a lot of sense. In areas where the supply of housing is more elastic (there is more room to build and probably fewer land use restrictions), higher property taxes largely affect the decision of whether to build more. In built-up areas, which often have restrictive zoning, housing stock is less elastic, so more of the response is channeled into higher prices.[23]

The Problem of Runaway Property Tax Growth

It’s one thing to say that property taxes are a good tax and worth preserving. It’s another thing altogether to defend the way property taxes have skyrocketed in some jurisdictions. Property owners are clamoring for relief, often with good reason. In response, policymakers across the country are exploring options to offset or constrain the growth of property taxes. Assessment, rate, and levy limits; circuit breakers; larger homestead exemptions; tax rebates; local revenue backfills; and even full repeal have been considered.

An immediate objection to any proposal to offset property tax burdens with revenue from some other source is that the alternative funding stream is likely to be more economically harmful, as outlined above. But rebates and offsets can introduce other problems as well, and often lead to higher overall levels of taxation.

Limits on the growth of property tax burdens, however, do not involve replacing one revenue stream with another. These constraints can apply to individual parcels, limiting how much a particular owner’s property taxes can rise year-to-year (assessment limits), or they can apply in aggregate for all existing property, limiting how much collections can rise on the same cluster of properties just because values have risen (levy limits). Additionally, many states have rate limits, though these are powerless against unlegislated, valuation-driven increases in property tax burdens that have generated the most outrage in recent years.[24]

Levy limits are an effective tool for keeping property taxes in check without distorting property markets or shifting burdens onto new homeowners. Assessment limits, while superficially appealing, can easily make housing affordability worse. Circuit breakers, meanwhile, have a place as a narrow intervention to protect the most vulnerable, but should not be allowed to grow into an alternative property tax system for broad swaths of homeowners.

Assessment Limits

The purpose of assessment limits is to constrain increases in individual homeowners’ tax burdens caused by rising home values. While property owners may be wealthier on paper due to the appreciation of their property value, their income flows and ability to pay higher taxes may not have risen proportionally. Assessment limits seek to cushion the blow, limiting the amount by which rising property values can increase exposure to taxation.

They do this in a variety of ways, such as by freezing or rolling back assessment increases, or, more commonly, by setting a cap on the maximum rate of assessment growth per year. Under assessment limits, a home’s value is only reset to market rates when a triggering event occurs. That can require a change in ownership or can be triggered by an addition or renovation project, depending on the provisions of a particular state’s assessment limits.

Over time, assessment limits lead to artificially low effective rates of taxation on long-time homeowners, with burdens shifting to new owners, and often to commercial real estate (frequently excluded from assessment limits). Notably, because apartment complexes are classified as commercial real estate, this means that most renters bear the cost of these shifted tax burdens, as homeowners experience shrinking effective rates each year.[25]

Assessment limits create a lock-in effect for existing homeowners, who are incentivized to remain in their current home—often avoiding significant renovations—even if it might otherwise be in their interest to move. Empty nesters, for instance, might live in a house that is too large for them and which could better meet the needs of a growing family, because downsizing would yield a higher tax bill.

Some states have added “portability” provisions to their assessment limits to address the lock-in effect, but that swaps one problem for another. Under portability provisions, homeowners may transfer their favorable assessment to another property, typically up to the amount of the prior savings. California even confers inheritability, allowing children and grandchildren to assume the sub-market-rate assessed value of the deceased grantor if the home becomes their primary residence.[26] Allowing existing homeowners to transfer their reduced assessment to another property eliminates the perverse incentive to stay put, but ensures that how long one has owned a home in the state—not one specific home, but any home—is the determining factor in one’s property tax liability.

This shifts tax burdens onto newer purchasers, many of whom have fewer financial resources than the established owners who receive preferential treatment. It therefore undermines affordability for these newer would-be purchasers. It also complicates the way that property values adjust in response to tax burdens, since the effective property tax rate will vary based on the identity of the prospective buyer and not just on the value and location of the property.

With assessment limits eroding the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

, jurisdictions must resort to millage increases just to remain at par. This can lead to anomalously high effective rates on new purchasers, which ought to be at least partially capitalized into the cost of the home (reducing its purchase price). This effect will be diminished, however, when some would-be purchasers (those transferring an existing assessment) will face low property tax burdens while others (those unable to transfer an assessment) face much higher future tax bills.

Significantly, lock-in effects apply not only to downsizing but also to upscaling. The cost of purchasing a costlier home is magnified if it means giving up a preferential assessment on one’s current home for a market-rate assessment on a new one. Even under portability, moreover, any value above that of one’s existing home will be taxed at market rate, which increases the marginal cost of moving. Policies that make it harder for empty nesters to downsize are inefficient, as they impede a mutually beneficial market reallocation of housing space, but artificially interfering with upscaling should not be neglected, either. This is particularly true in jurisdictions where land values are high or zoning policies are stringent, as these may create incentives for new construction to be larger and more expensive. Enabling households with rising fortunes to move into something more spacious or desirable frees up their existing, more affordable home for newer entrants into the housing market.

Under assessment limits, new homes will, on average, be taxed more heavily than existing stock. In the absence of a portability regime, any newly constructed home will bear the full weight of a jurisdiction’s property taxes, while they will be partially abated for any existing stock, based on how much time has transpired since the last market-rate reassessment (if any). Even with portability, many purchasers will lack the ability to transfer an assessment, and those with transferrable assessments may not find them adequate to cover the entire valuation of the new home. This disincentivizes new construction, as new homes will experience disproportionate levels of taxation. The overall effect can be to reduce housing affordability and availability over time.[27]

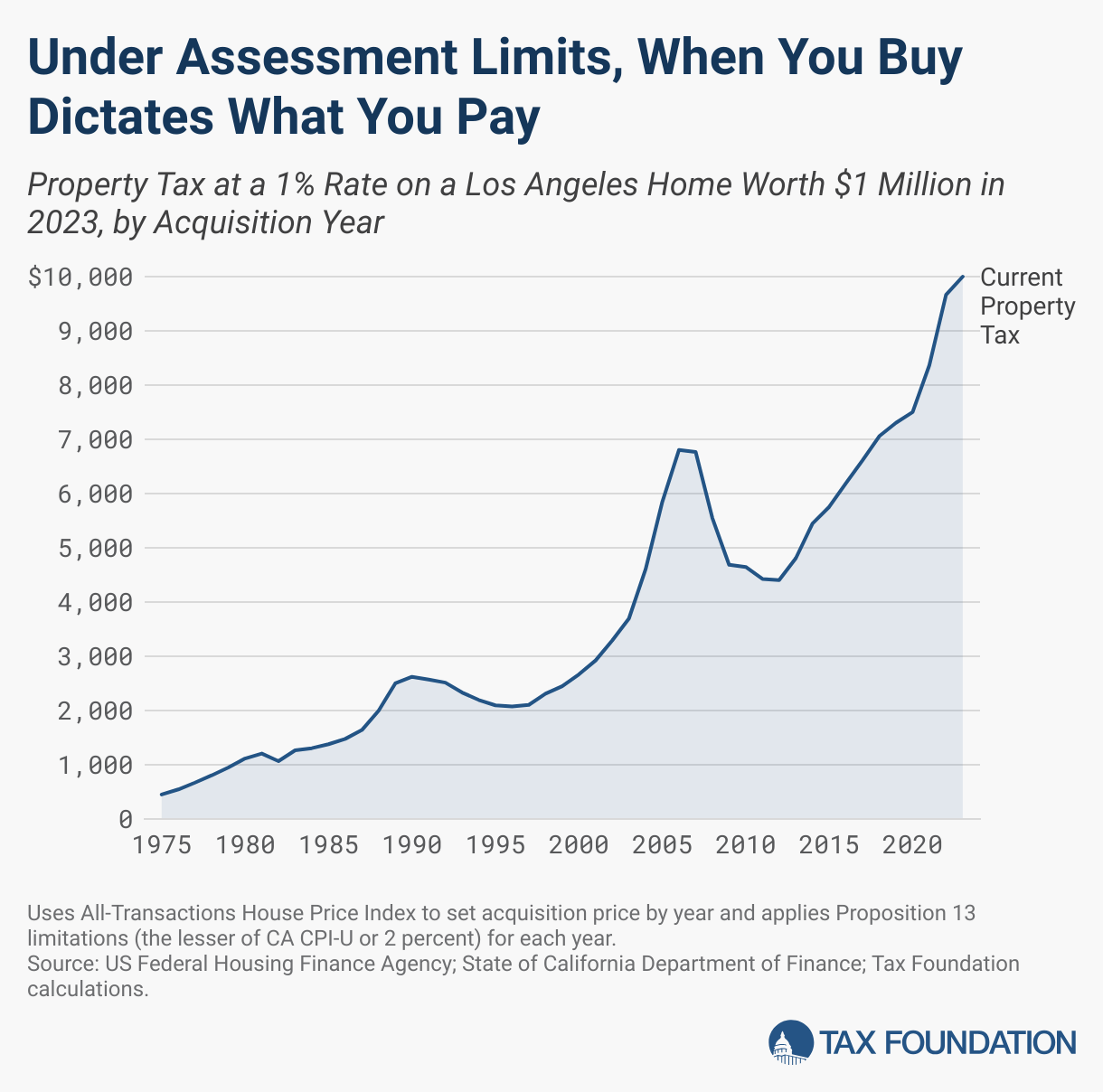

To understand just how distortionary assessment limits can be, consider the case of California’s Proposition 13, the 1978 ballot measure that implemented the nation’s first assessment limit. Under this provision—modified many times, but still in effect today—properties are only revalued when sold, with portability for incumbent homeowners. As long as a property remains under the same ownership, its assessed value for tax purposes can only increase by the lesser of 2 percent or inflation each year.

Imagine two homes side-by-side in Los Angeles, California, both with a current market rate of $1 million. One, however, was purchased in 1975 (the base year for Proposition 13 calculations), while the other was purchased in 2023. At a tax rate of 10 mills (1 percent), the $1 million home purchased in 1975 would yield a $451 tax bill, while the identical home purchased in 2023 would pay $10,000.

Rate Limits

Rate limits are intended to restrict consciously adopted tax increases, limiting the authority of local government officials to adopt a tax increase. They may cap the amount of a rate increase in a given year, establish a maximum allowable rate, require voter authorization to raise taxes, or even freeze rates outright. Under rate caps, collections can rise unimpeded if property values grow or if new construction is added to the property tax rolls, but policymakers are constrained in their ability to increase millages on those properties.

Rate limits have their place. Many states set maximum rates, and this can be particularly important when multiple local governing bodies—counties, cities, school districts, water commissions, fire departments, etc.—have taxing authority. But rate limits are unlikely to be the solution to present complaints about property taxes because, for the most part, rising tax burdens have been driven by skyrocketing property values, not rate increases.

Levy Limits

Unlike assessment limits, levy limits (also called revenue or collection limits) are concerned with the actual amount of revenue raised, imposing rollbacks or obligating rate reductions to ensure that collections do not increase in aggregate above a given amount. Individual owners may experience an increase or decrease in tax liability based on changes in rate or assessed value, but aggregate collections from the same set of properties are constrained. Whereas assessment limitations only allow a tax increase above a given threshold based on intentional policy action (a rate increase) and rate limitations only permit them when driven by rising housing values, a levy limit permits greater variation but all within the context of a hard revenue limit.

Like rate limits and unlike assessment limits, levy caps do not necessarily protect all taxpayers individually from tax increases. Policymakers remain free to adjust rates within the overall revenue cap unless separately constrained by a rate limit, and if only certain properties or classes of properties appreciate in value substantially, the owners of those properties may experience tax increases considerably in excess of any limitation on the increase in levies as a whole. But they avoid picking winners and losers, avoid creating perverse incentives, and impose an effective constraint on the growth of property taxes.

Levy limits neither reward nor penalize new construction, the choice between moving and staying, or a decision on whether to renovate a home. They keep property tax increases in check without severing the connection between property owners’ tax liability and their relative assessed values.

This turns out to be important. While it’s appealing to promise that no homeowner’s tax bill will rise above some set amount, it’s not really a property tax if it’s no longer tethered to the market value of the property. More valuable properties should face higher property tax bills than less valuable ones, in proportional terms. The key is to ensure that neither property’s taxes skyrocket just because valuations rise.

Imagine two properties in different neighborhoods in the same city, both purchased at the same time for $250,000. One neighborhood takes off, and the home is now worth $500,000. The other neighborhood doesn’t change as much, but since all property values have appreciated, that home’s value increases to $350,000. Neglecting inflation, if property tax rates remain unchanged, one home will see a 100 percent increase in property tax burdens while the other will see a 40 percent increase, neither of which is likely warranted. Millages should be rolled back to avoid these large unlegislated increases, which a levy limit would accomplish automatically. But should the house worth $500,000 have the same property tax bill as the one worth $350,000 (the outcome of an assessment limit), or should the home with the higher market value pay proportionally more than the home with a lower value?

This isn’t just a fairness issue. It also affects economic incentives and has a bearing on what the property tax is and does. Assessment limits shift the burden of the tax onto new investment, restricting housing supply and reducing housing affordability. They also sever the link between taxes paid and benefits received, forcing newer purchasers to bear burdens radically disproportionate to the value of services provided. Levy limits, by contrast, keep tax burdens in check without cutting the vital linkage between market value and taxation.

Levy limitation regimes typically allow local governing bodies to ask voters to approve increases above the limit. These voter overrides, however, force the increase to be a conscious choice, and one ratified by the voters, which is markedly different from a hidden, unlegislated tax increase. Levy limits can also be paired with “truth in taxation” requirements that provide more transparency to homeowners about the cost of a potential property tax change. Because levy limits are the best option for constraining unlegislated property tax increases, we will return to them later, outlining how best to design and implement such limitations.

Rebates and Swaps

The property tax has been a mainstay of local government tax collections since the colonial era. The advent of new revenue sources—chiefly the local sales tax—has led to some diversification of local tax revenues, but property taxes still reign supreme. In 1902, property taxes accounted for 89 percent of local tax revenue, with the figure soaring to 97 percent at the onset of the Great Depression. Today the figure stands just below 73 percent—a decided decline, but one that still leaves the property tax as a vitally important source of local revenue, with its share of collections largely stable since the 1980s.[28]

The property tax generates 90 percent or more of local tax revenue in more states (13) than where it generates 60 percent or less (9 states). Nationwide, the property tax is responsible for 73 percent of local tax revenue, 37 percent of own-source revenue, and 26 percent of all revenue. Any proposal to eliminate the property tax—like those advanced in Nebraska, North Dakota, Wyoming, and elsewhere in 2024—has to grapple with how significant a revenue source it is.[29]

Even when state lawmakers only propose to defray property tax burdens, not eliminate them, the task can be daunting—and the results often disappointing. Broadly speaking, state-level relief comes in two forms: aid distributed to localities that is intended to drive down local property tax rates, and aid delivered directly to homeowners to offset the burdens of those local taxes. Lawmakers must, moreover, confront three challenges: (1) the likely economic inferiority of the alternative revenue stream, (2) distributing relief equitably and without creating perverse incentives, and (3) not enabling local governments to respond in ways that drive the overall tax burden higher rather than lower.

Whether delivered to localities or directly to homeowners, if relief is proportionate to property tax burdens, the policy rewards jurisdictions with higher property taxes, forcing communities with lower taxes and fewer services to subsidize (through their residents’ state taxes) areas with higher service provision. This incentivizes the latter communities to raise their own taxes, unless they are restricted from doing so, in which case the reverse subsidy will persist.

Using state revenues to offset property taxes undercuts the benefit principle to which property taxes otherwise hew. Property taxes offer local control and visibility, allowing property owners to judge for themselves whether the services they receive are worth what they pay in taxes. When property tax burdens are defrayed using state revenues, not only is there a statewide redistribution that has no regard for the services any particular taxpayer receives, but the pressure on local governments to achieve a proper balance of taxes and spending is alleviated.

Just because states transfer funds to local governments, moreover, does not guarantee that localities will reduce property tax rates, which is particularly important since the pressure to maintain fiscal discipline is reduced under systems of state offsets. Some states have addressed this by mandating rate rollbacks or reducing assessment ratios, which delivers tax relief to all taxpayers, at least initially. If, for instance, property taxes were originally levied at 100 percent of market value, and the state plans to provide aid to local governments to defray property taxes by 10 percent, lawmakers could set the new assessment ratio to 90 percent (meaning that only 90 percent of the value of property is included in the tax base), delivering an automatic 10 percent tax cut to property owners.

But this is a one-time adjustment. Local officials could not restore the old assessment ratio, but absent other constraints, they may be free to raise rates, or at least not lower them when property values soar. This may quickly yield property taxes that are just as high as before, even though the state is now on the hook for state aid.

State aid paired with levy limits would be more effective, provided the state assistance is counted as property tax revenue and counts toward the limit. There is still the possibility that voters may choose to override limits, restoring taxes to prior levels or higher, but at least local governing bodies cannot do this on their own. This is better, but still involves reducing burdens under an economically efficient tax by increasing them under a less efficient tax, and still involves redistribution across the state—often to the benefit of costlier homes in higher-tax, larger-government jurisdictions.

Conversely, instead of providing aid to localities to defray property tax burdens, some states provide relief directly to homeowners, often in the form of refundable income tax credits. Not only does this approach fail to satisfy discontented property owners—their property tax bill does not go down, after all, even if they receive offsetting assistance later—but it may actually result in an increase in property tax burdens, since local government officials rightly understand that tax increases “cost” less due to the subsidy.

Such relief also tends to be limited to owner-occupied housing, which shifts more burdens onto businesses (again undermining the tax’s neutrality) and can be perversely regressive, since renters—many of them lower-income than homeowners—would not benefit from the relief, even though they pay into the state taxes that fund it.

Other Mechanisms

Other approaches to property tax relief involve increasing homestead exemptions and adopting so-called “circuit breakers” for low-income homeowners. Homestead exemptions have long been a feature of property taxes, exempting a certain amount (e.g., $25,000) of the value of a primary residence. This approach provides a benefit to primary residences compared to second homes, but it also favors homeowners over renters, and residential property over commercial. It also has no connection with the value of the property or ability to pay. Moreover, it does not change the marginal rate of taxation. Recent efforts to dramatically raise homestead exemptions—like the new $100,000 exemption in Texas[30]—can carve up the tax base in areas with lower housing costs, while distorting property markets and doing nothing to help most renters.

Circuit breakers, by contrast, provide targeted relief to those who might otherwise find themselves priced out of their home. Broadly speaking, circuit breakers come in two types. “Threshold” circuit breakers provide relief when property tax liability exceeds some threshold percentage of household income, while “sliding scale” circuit breakers provide relief based on income levels, delivered as an offset of a certain percentage of their property tax liability, regardless of the percentage of income consumed by property taxes.[31]

Many states establish eligibility based on age as well as income, but as the Lincoln Institute of Land Policy convincingly argues, this is a policy error.[32] Many retirees are wealthy and should not receive targeted relief merely due to their age, while at the same time, many families well under retirement age face financial difficulties. A circuit breaker that grants eligibility based on either age or income is unnecessarily broad, while one that makes age-based eligibility a prerequisite fails to help many households in need.

The benefit of circuit breakers over assessment limits is that the relief is more narrowly targeted based on need and does not unduly distort the entire property market. In an ideal world, policymakers might take assets into account as well as income in determining eligibility, but in practice, this adds significant complexity and generates high compliance costs for eligible families. Policymakers may, however, wish to consider whether to put limits on the value of the home itself, to avoid situations where circuit breakers subsidize cash-poor but land-rich families rather than fulfilling their intended function of ensuring that low-income households aren’t driven out of their homes by high tax burdens.

Finally, many states have tax deferral programs, allowing certain homeowners to defer property tax payments until a home is sold. Take-up of these programs tends to be limited, sometimes leading to the conclusion that they are not a policy success. But that may be the wrong way of looking at it. Low take-up suggests that, given existing relief mechanisms, relatively few taxpayers are at risk of having taxes price them out of their existing home—which would argue against sweeping policies affecting the entire housing market supposedly predicated on solving this problem. Meanwhile, to the extent that some households do face hardships, the deferral option is available to them.[33]

Implementing Levy Limits

Levy limits can be a good option for states seeking to constrain the growth of property taxes, but the details matter. For levy limits to work properly, they must be imposed at the correct level of government and the annual adjustment mechanisms must be well designed.

Some states have implemented levy limits at the state level, meaning that millages in every jurisdiction roll back based on the overall projected statewide increase in property tax collections due to rising property values. This makes little sense, as it provides insufficient relief in areas that are growing (and seeing values rise faster than statewide averages), and it creates perverse incentives for localities. The limitation should be imposed at the level of the responsible taxing jurisdiction—typically a county, city, or school district. State policy can create such limitations, but the limitation should apply to each taxing jurisdiction individually, not in statewide aggregate.

As previously noted, the appropriate measure for levy limitations is the anticipated tax liability for preexisting property. When property values are rising, the exact same set of properties will have higher tax liability year over year. The goal of a levy limit is to cap the amount of revenue that can be generated from the status quo by reducing millages accordingly. New construction should be excluded, because it appropriately brings in additional revenue, as the additional housing or commercial property creates new costs for the locality.

Policymakers also need to decide on an appropriate annual growth factor for that existing property. Typically, it will be inflation at a minimum, or perhaps inflation plus some additional amount of allowable growth—like 1 or 2 percent growth above inflation. Lawmakers must also decide what spending obligations, if any, can allow increases beyond the growth factor. But before we dive into that, let’s take a step back and see how such a system works.

Imagine a small jurisdiction with 2,000 homes. (For the sake of simplicity in this example, we’ll only consider homes, though commercial and industrial property matter as well.) In the first year, they collectively bring in $5 million in property taxes at that year’s property tax rates. By the next year, 100 new homes have been built, bringing in an additional $300,000 in property taxes under existing rates. The preexisting 2,000 homes, meanwhile, have seen their assessed values rise, and they are now projected to bring in $5.6 million if rates do not change.

If inflation were at 2 percent and this locality imposed a growth factor of inflation plus 2 percent, then rates would have to be adjusted to ensure that the existing 2,000 homes paid no more than $5.2 million. This would obligate a 7 percent reduction in tax rates. (If, for instance, the rate had been 10 mills previously, it would be about 9.3 mills in year two.) The additional revenue expected from the 100 new homes would not be part of this calculation, though they too would benefit from the lower rate and thus bring in a little under $280,000 rather than $300,000. Overall collections would rise from $5 million to about $5.48 million, whereas they would have risen to $5.9 million absent the limitation.

Many limitation laws stipulate that tax in the amount necessary to service certain debt, or to meet certain obligations, is not subject to the levy limit. This can make sense, but policymakers need to tread carefully if they wish to avoid gutting their own limitations. It may be reasonable to exclude debt service on revenue-producing improvement bonds, for instance, but if all bonds are excluded, this may render the limit ineffective. It may be necessary to allow taxes to rise above the otherwise limited amount if a locality incurs liability in litigation. It likely does not make sense, however, to allow a wide range of obligations—including pension contributions—to provide end-runs around the limits.

If a jurisdiction were up against a rate limit, local officials would not be permitted to raise the rate above that amount due to rising costs. They would be obligated to find other ways to balance the budget. It is reasonable for levy limits to impose roughly commensurate constraints.

Sometimes, however, a jurisdiction may have good reason to increase revenues above the allowable growth factor. Well-designed levy limits do not prohibit this. They make the increase transparent, and frequently put the decision in the hands of voters, who can decide whether to authorize an override. The beneficial effect of levy limits is to crack down on unlegislated tax increases that result from appreciation in property values, without anyone—local officials or the general public—ever casting a vote to raise taxes.

Finally, in crafting levy limits, lawmakers should avoid allowing a downward ratchet effect during economic downturns and should consider allowing local officials to “bank” some or all of the allowable increase they decline to use.

During a recessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years.

, property values often decline, typically rebounding in a few years. If a levy limit restricted revenue growth as the property market recovered, it could result in far less tax being collected on the same set of properties post-recovery compared to pre-recession. Levy limits are intended to constrain expansionary tax policies; they are not supposed to have a sharply contractionary effect. In designing levy limits, lawmakers should avoid this downward ratchet effect by applying the allowable growth factor against the last highest collections, not the previous year’s collections, when there has been a decline in value.

Sometimes, moreover, local officials may elect not to take advantage of additional revenues. They may choose to reduce rates more than what is obligated by the levy limits, declining to capture the revenue growth allowed by the statewide formula. If the levy limitations are use-it-or-lose-it, this strongly incentivizes jurisdictions to take all allowable growth each year so that they do not reduce their capacity to increase revenues later. To avoid encouraging localities to always max out, lawmakers might consider allowing jurisdictions to “bank” at least some of the unused cap.

Conclusion

The property tax won’t win any popularity contests with homeowners, but it still has an important role to play in public finance. Policymakers can and should address taxpayers’ legitimate grievances about out-of-control property tax bills, but they should do so without upending a system of taxation that is more efficient, fair, and pro-growth, and better suited to municipal finance, than any of the alternatives.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

[1] Zillow, “Zillow Home Value Index,” https://www.zillow.com/research/data/.

[2] US Census Bureau and US Department of Housing and Urban Development, “Average Sales Price of Houses Sold for the United States,” retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/ASPUS.

[3] S&P Dow Jones Indices LLC, “S&P CoreLogic Case-Shiller U.S. National Home Price Index,” retrieved from FRED, Federal Reserve Bank of St. Louis, https://fred.stlouisfed.org/series/CSUSHPINSA.

[4] Some sources attribute the first property tax to one or more of the dynasties of ancient Sumer as far back as 8,000 years ago, with some pointing to cuneiform records of the bala system of Ur III, but this appears to be a double error, both that the Ur III system was characterized by excise taxation, and that the dynasty dates to about 4,000 years ago, not 6,000—which would predate the emergence of cuneiform tablets. Undeniably, however, property taxes are very old, and well attested throughout classical antiquity.

[5] The rare exceptions are a few oil-rich Gulf states and a handful of small countries with economies geared around wealthy ex-pats and nonresidents, like Lichtenstein and the Cayman Islands.

[6] Glenn W. Fisher, The Worst Tax?: A History of the Property Tax in America (Lawrence, KS: University Press of Kansas, 1996).

[7] Joan Youngman, A Good Tax: Legal and Policy Issues for the Property Tax in the United States (Cambridge, MA: Lincoln Institute of Land Policy, 2016).

[8] Welfare spending, almost by definition, is evaluated in terms that go beyond economic efficiency to questions of rights, responsibilities, dignity, and opportunities. The relative efficiency of these programs clearly matters, and there are accordingly better and worse ways to structure such programs, but the case for assisting the least fortunate is not predicated on the notion that doing so boosts overall economic growth. All policy involves trade-offs.

[9] Jens Arnold, Bert Brys, Christopher Heady, Åsa Johansson, Cyrille Schwellnus, and Laura Vartia, “Tax Policy for Economic Recovery and Growth,” Economic Journal 121:550 (2011): F59-F80.

[10] Santiago Acosta-Ormaechea and Jiae Yoo, “Tax Composition and Growth: A Broad Cross-Country Perspective,” IMF Working Paper, October 2012.

[11] Dagney Faulk, Nalitra Thaiprasert, and Michael Hicks, “The Economic Effects of Replacing the Property Tax with a Sales or Income Tax: A Computable General Equilibrium Approach,” Ball State University, Department of Economics, Working Papers, June 2010.

[12] Stephen T. Mark, Therese J. McGuire, and Leslie E. Papke, “The Influence of Taxes on Employment and Population Growth: Evidence From the Washington, D.C. Metropolitan Area,” National Tax Journal 53:1 (2000): 119.

[13] Thomas J. Nechyba, “Replacing Capital Taxes with Land Taxes: Efficiency and Distributional Implications with an Application to the United States Economy,” in Land Value Taxation, edited by Dick Netzer (Cambridge MA: Lincoln Institute of Land Policy, 1998), 183-204.

[14] With extremely limited exceptions, the land itself is fixed, but improvements to property are not, of course, a fixed stock. Current structures can be torn down or allowed to become dilapidated, or additional structures can be built. However, these responses are not just slower, but also less pronounced than with other taxes, and without the substitution effects found elsewhere.

[15] For a survey of the literature, see Timothy Vermeer, “The Impact of Individual Income TaxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

Changes on Economic Growth,” Tax Foundation, Jun. 14, 2022, https://taxfoundation.org/research/all/state/income-taxes-affect-economy/.

[16] For a longer discussion, see Jared Walczak, “Modernizing State Sales Taxes: A Policymakers’ Guide,” Tax Foundation, Sep. 5, 2024, https://taxfoundation.org/research/all/state/state-sales-tax-reform-guide/.

[17] Most countries impose value-added taxes (VATs) rather than a general sales tax. In the US, VATs are often conflated with gross receipts taxes (GRTs), but the two are quite different. With a VAT, the tax is imposed at every stage of the production process, but only incrementally, on the added value. With a GRT, tax is imposed on the whole value at every stage of production. Thus, a VAT is the economic equivalent of a sales tax imposed only on the final transaction, except that the amount is achieved in increments rather than all at once, whereas a gross receipts taxA gross receipts tax, also known as a turnover tax, is applied to a company’s gross sales, without deductions for a firm’s business expenses, like costs of goods sold and compensation. Unlike a sales tax, a gross receipts tax is assessed on businesses and apply to business-to-business transactions in addition to final consumer purchases, leading to tax pyramiding.

will yield taxation in multiples of the amount that would be owed under a well-constructed sales tax. In practice, US sales taxes exclude many, but far from all, business inputs, and about 41 percent of the revenue from state sales taxes comes from intermediate transactions.

[18] Youngman, 24-25.

[19] See, e.g., Wallace E. Oates and William A. Fischel, “Are Local Property Taxes Regressive, Progressive, or What?,” National Tax Journal 69:2 (June 2016): 415-434; and George R. Zodrow, “The Property Tax as a Capital Tax: A Room with Three Views,” National Tax Journal 54:1 (2001): 139-156.

[20] On capitalization generally, see William H. Hoyt, Paul A. Coomes, and Amelia M. Biehl, “Tax Limits and Housing Markets: Some Evidence at the State Level,” Real Estate Economics 39:1 (2011): 97-132; and George R. Zodrow, “Intrajurisdictional Capitalization and the Incidence of the Property Tax,” Regional Science and Urban Economics 45:2 (2014): 57-66.

[21] Youngman, 26-29.

[22] Oates and Fischel, 419-421.

[23] Byron Lutz, “Quasi-experimental Evidence on the Connection Between Property Taxes and Residential Capital Investment,” American Economic Journal: Economic Policy 7:1 (2015): 425.

[24] For a general summary of these options, see Jared Walczak, “Property Tax Limitation Regimes: A Primer,” Tax Foundation, Apr. 23, 2018, https://taxfoundation.org/research/all/state/property-tax-limitation-regimes-primer/.

[25] On the incidence of property taxes on renters, see, e.g., Robert J. Carroll and John Yinger, “Is the Property Tax a Benefit Tax? The Case of Rental Housing,” National Tax Journal 47 (June 1994): 295-316; and Leah J. Tsoodle and Tracy M. Turner, “Property Taxes and Residential Rents,” Journal of Real Estate Economics 36:1 (2008): 63-80.

[26] Ca. Const. art. XIII A § 2(h).

[27] Emily Horton, Cameron LaPoint, Byron Lutz, Nathan Seegert, and Jared Walczak, “Property Tax Policy and Housing Affordability,” National Tax Journal 77:4 (forthcoming), https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4901553.

[28] Tax Foundation analysis of Census data from multiple years. US Census Bureau, “Historical Statistics of the United States, Colonial Time to 1970” (September 1975), https://www.census.gov/library/publications/1975/compendia/hist_stats_colonial-1970.html; “Statistical Abstract of the United States,” multiple years, https://www.census.gov/library/publications/1976/compendia/statab/97ed.html; and “Annual Survey of State and Local Government Finances,” multiple years, https://www.census.gov/programs-surveys/gov-finances.html.

[29] US Census Bureau, “Annual Survey of State and Local Government Finances,” 2021.

[30] Texas Proposition 4, “Property Tax Changes and State Education Funding Amendment,” 2023.

[31] John H. Bowman, Daphne A. Kenyon, Adam Langley, and Bethany P. Paquin, “Property Tax Circuit Breakers,” Lincoln Institute of Land Policy, May 2009, https://www.lincolninst.edu/publications/policy-focus-reports/property-tax-circuit-breakers/.

[32] Id. 10-11.

[33] Youngman, 10.

Share this article