Key Findings

- By 2035, the Old-Age, Survivors, and Disability Insurance Trust Fund, or the Social Security Trust Fund, will be depleted, and current payroll taxes will only be able to fund 83 percent of the scheduled benefits.

- Absent any reforms, Social Security recipients would immediately face a 17 percent cut in benefits.

- Past reform efforts, such as the 1983 amendments, have not been able to solve Social Security’s long-term funding problem, which is due to a declining worker-per-retiree ratio that now stands at only 3-to-1 and is projected to fall further.

- Reforms such as using price indexing instead of wage indexing to calculate benefits, raising the retirement age, using the chained CPI to adjust benefits for inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

, and raising the payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue.

cap would restore solvency to the system. - The current Social Security system crowds out private saving and harms young workers and new entrants to the labor force.

- Policymakers should look to other countries for inspiration, including Chile, Singapore, Australia, and Chile, which have all reformed their systems to encourage personal saving.

Introduction

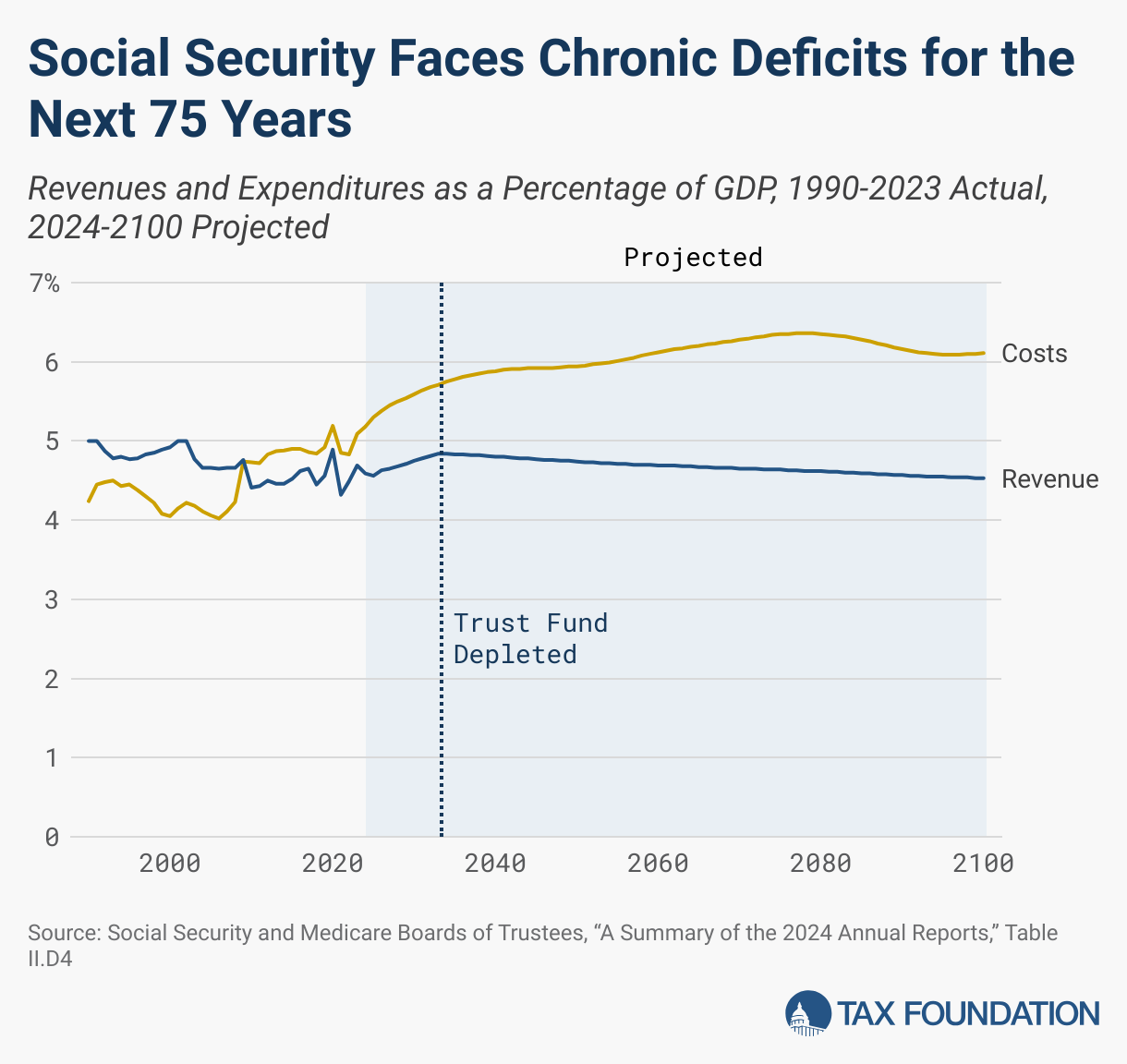

Social Security is by far the largest federal government spending program,[1] constituting 21 percent of the budget, or $1.3 trillion, in FY 2023—larger than the entire nondefense discretionary budget. The latest trustees report shows the program is on a fiscally unsustainable path that will exacerbate the US debt crisis if its imbalances are not addressed in the near term.[2] By 2035, the Old-Age, Survivors, and Disability Insurance (OASDI) Trust Fund will be depleted, and current payroll taxes will only be able to fund 83 percent of the scheduled Social Security benefits. Absent any reforms, Social Security recipients would immediately face a 17 percent cut in benefits.[3]

As it stands, neither major party candidate seeking the presidency of the United States has indicated that they would significantly alter the program’s negative trajectory, and one proposal would actually worsen it. Former President Donald Trump has indicated that not only would he prohibit any benefit cuts, but he would also consider exempting Social Security benefits from taxation entirely, which would accelerate insolvency of the program by six years.[4] Vice President Kamala Harris has not yet made any formal statements on how she would alter the program, but her voting record in the Senate suggests that she would be open to raising payroll taxes on high earners, which alone is not sufficient to close the funding gap.[5]

Fortunately, we can draw lessons from past reform efforts to stave off the coming crisis. Reforms will involve politically difficult choices, but they are necessary if we are to ensure a broad-based and universally accessible retirement system of some form exists for future generations and is not threatened by funding cliffs. We can also look to other countries that have faced similar crises to learn how they reformed their retirement systems over time. This paper will consider comprehensive reforms in Sweden, Australia, Singapore, and Chile; while none of their systems are perfect, they demonstrate the feasibility of significant improvements to how the federal government incentivizes saving for retirement.

How Social Security Works

Social Security is a defined benefit pension system, where benefits are calculated based on a predetermined formula that accounts for a retiree’s earnings over time. Under this system, current payroll taxes fund current retirees, resulting in a “pay-as-you-go” system. The pay-as-you-go structure means the fiscal health of the program depends on how many workers contribute through payroll taxes each year.

Social Security payroll taxes are applied to an earner’s wage income, up to $168,600 for 2024.[6] The current Social Security payroll taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

rate is 12.4 percent, split between the employer and employee.[7]

Social Security benefits are calculated based on the average wage-indexed monthly earnings over a retiree’s career.[8] The formula replaces a larger share of income for lower earners relative to higher earners, and the relative replacement rates will remain constant over time no matter how high wages grow, since the benefits themselves are indexed to real wage growth. Although the program is not explicitly means-tested, in the sense that all retirees receive some benefit regardless of how high their incomes were during their working years or how many assets they currently hold, the formula ensures that the program is progressive.

The tax treatment of benefits also contributes to the system’s progressivity. Joint filers with less than $32,000 of income, and single filers with less than $25,000, face no tax on benefits (income is defined as “modified adjusted gross incomeFor individuals, gross income is the total pre-tax earnings from wages, tips, investments, interest, and other forms of income and is also referred to as “gross pay.” For businesses, gross income is total revenue minus cost of goods sold and is also known as “gross profit” or “gross margin.”

,” or adjusted gross income plus tax-exempt interest plus half of Social Security benefits). Households earning between those thresholds and $34,000 for single filers and $44,000 for joint filers face taxation on half of their benefits. Above those levels, up to 85 percent of benefits are taxable.[9]

Recipients can receive full benefits starting at age 67 for people born in 1960 or later.[10] They may start receiving partial benefits as early as age 62, subject to an early retirement penalty. A delayed retirement credit up to age 70 is also available.[11]

Under the current three-bracket calculation system, higher earners receive a smaller share of their lifetime earnings compared to lower earners. For example, Social Security benefits will replace 90 percent of the first $1,174 in average indexed monthly earnings. But for the next $5,904 in monthly income, the replacement rate falls to 32 percent of earnings. For earnings in the third bracket, up to the maximum of $14,050 (equivalent to $168,600 in annual income), the rate falls further to 15 percent.[12] Income earned in excess of the maximum is not replaced.[13]

The dollar thresholds separating the brackets (which the actuaries call “bend points”) are adjusted each year to match the rise in average wages covered by Social Security in the economy. That results in a constant set of replacement rates over time for low-, average-, or upper-income retirees. Constant replacement rates do not mean constant benefits, but they do mean that as wages rise in real terms over time, the benefits will keep pace to maintain the existing ratios.

The trustees report assumes that real wages will grow in the long run by 1.14 percent annually, boosting real benefits accordingly at all income levels.[14] For example, lower-income workers (with average earnings over a 35-year period of $31,100) will on average receive benefits of $18,000, for a replacement rate of 58 percent. By the end of the century, lower-income workers will receive real benefits 43 percent higher than benefits paid to current medium-wage workers.[15] And medium-wage workers, who currently receive $29,800 in benefits, will receive real benefits 79 percent higher than benefits paid to current high-wage workers. Benefits are even higher for people qualifying for the 50 percent spousal benefit for married couples, or up to twice as much in cases where both spouses worked and qualified for benefits.

Why Social Security Is Facing a Crisis

In 1960, 20 years after Social Security issued its first payments, the ratio of workers to retirees stood at 5 to 1.[16] It has since fallen to 3 to 1 and is expected to fall to 2 to 1 by 2030.[17] Since the Great RecessionA recession is a significant and sustained decline in the economy. Typically, a recession lasts longer than six months, but recovery from a recession can take a few years.

, Social Security has been in a persistent deficit, as benefit payments have consistently exceeded payroll tax receipts. The OASDI Trust Fund has covered the gap, but by 2035, it will be depleted.

The program’s projected costs continue to balloon over the next 75 years due to increasing numbers of retirees, expanding longevity, and declining fertility. The latest trustees report shows that payroll taxes would have to rise by 3.5 percentage points, or 28 percent, to cover the shortfall.[18]

The recurring deficits of the Social Security system are primarily the result of a clash between the falling ratio of workers to retirees and the wage-indexed benefit formula that seeks to keep replacement rates constant per retiree at every point in the income distribution. Another smaller factor is the falling share of earnings subject to payroll tax due to the rise of tax-exempt employer-sponsored health insurance and other fringe benefits, as these benefits are a much larger share of total compensation than they were decades ago.[19] To truly bring the system into balance, either fertility rates must permanently increase sharply, tax rates or the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

must increase, or the formula must allow the replacement rates to decline over time.

Substituting Real Personal Saving for Part of Our Tax and Transfer System

The current Social Security system in the United States relies heavily on the tax and transfer system rather than on personal saving. One reason the status quo remains popular is that a defined benefit system like Social Security eliminates some uncertainty involved when saving for retirement. Benefits are “guaranteed” by law to the recipient upon retirement, regardless of how the financial markets and the economy perform. And many workers will receive more than they paid into the system in nominal dollars. The average middle-income couple will have paid $783,000 in taxes and receive $831,000 in benefits.[20] Low earners will receive even more generous benefits relative to what they paid in taxes because of the progressive benefit formula.

However, the system contains several drawbacks. First, it is not totally free from uncertainty. Economic downturns can cause payroll tax revenue to slow and projected Social Security deficits to increase, as happened in the early 1980s. Congress has been compelled in the past to reduce the benefit structure in such circumstances, as it was in 1983.[21]

Second, while Social Security provides generous benefits for retirees with low incomes, and many workers can expect to receive more from Social Security than they paid into it, it is a raw deal for many workers compared to the savings they could accumulate if they had the option to invest in personal accounts. A worker’s contribution to Social Security through payroll taxes earns about a 3 percent real rate of return over the long run, whereas investors can expect a 7 percent real rate of return holding stocks.[22]

Of course, there is no free lunch: the higher return in the stock market compensates savers for the higher risk. Nonetheless, private accounts would give taxpayers the choice of how much risk they are willing to bear as well as options to diversify their portfolios beyond low-yielding Treasuries. As an example, a young entrant into the workforce could invest heavily in equities and then shift to bonds and less risky assets as they age.

The government system thus contains several vulnerabilities. As funds are invested in low-yielding Treasuries, the financial health of such a system depends on the size of the working-age population and how much workers pay in payroll taxes. Unlike defined contribution systems, where taxpayers deposit funds into their own personal accounts, and are therefore self-funding, defined benefit systems will always risk being underfunded.

The other issue with the current Social Security system is that it limits the ability of young earners to save independently of the current system for their own retirement. Social Security crowds out private saving in two ways. First, it collects payroll taxes from the working-age population. Many of the workers subject to the payroll tax have just entered the labor force, earn lower wages than more experienced workers, and thus are not able to save as much as they would in the absence of a payroll tax.

Second, because households receive Social Security when they retire, they are less likely to save than they would if Social Security did not exist. Of course, some households also save less because they might be short-sighted, make bad investments, or have incomes so low that their ability to save is constrained.

Under the current system, the burden of the payroll tax and the knowledge of guaranteed benefits in the future reduces some saving, yet many households still save outside of Social Security. For individuals 65 and older, Social Security represents about 30 percent of their total income.[23] Less than 15 percent of the retired population rely on Social Security for 90 percent or more of their income. Many individuals save independently, and more than half participate in a defined contribution or defined benefit pension plan through their employer.[24]

The current system also has implications for intergenerational transfers. When individuals die in old age, they pass on their wealth to their children or close friends. But because Social Security “wealth” is not owned by them, they do not pass on any benefits that they would have if they had managed their own personal accounts. Currently, only about 1 in 5 households receive an inheritance according to the Federal Reserve Board’s Survey of Consumer Finances, but it is possible this would be higher under a different system of saving.[25]

Learning from Past Reform Efforts

The last time Social Security was reformed was in 1983. During the early 1980s, the economy was battered by high inflation, high unemployment, and wage stagnation, resulting in lower payroll tax revenue than would be needed to fund benefits for retirees. The situation was even more dire than it is today; when the reforms were actually enacted, the OASDI trust fund was scheduled to run out that year.[26] The bipartisan 1983 changes gradually raised the full retirement age from 65 to 67, raised the payroll tax by 1.6 percentage points, and introduced the taxation of benefits.[27]

The reforms brought Social Security into a surplus for nearly three decades, until 2009, but did not solve the contradiction between the long-run demographic problem facing the program and the wage-indexed benefit formula. Even the 1984 trustees report projected a deficit over the next 75 years of 0.06 percent,[28] with growing annual deficits in the later decades of the 75-year planning period. As early as 1993, the trustees were estimating the trust fund would be depleted by 2036.[29]

Reforming Replacement Rates

Currently, the Social Security bend points (the income brackets used to calculate the replacement rates) are indexed to the average growth in wages. This originated in the 1977 Social Security amendments, which were designed to correct an earlier reform that overcorrected for inflation and imperiled Social Security’s financing during the 1970s stagflation.[30] The introduction of wage indexing, unfortunately, placed Social Security on a path of permanent instability.

In 1976, Congress convened a panel under Harvard Professor William C. Hsiao to correct the Social Security benefit formula that had led to skyrocketing replacement rates. The panel presented two options, each involving a benefit formula with bend points and fixed replacement rates. The first option indexed bend points to wage growth, while the second indexed them to price growth.

The Hsiao panel recognized that wage indexing would plunge Social Security into chronic deficits given the impending demographic changes—a finding consistent with an earlier report by retirement experts presented to the Senate Finance Committee in 1973.[31] For this reason, the Hsiao panel recommended using price indexing, which would have reduced benefit growth over time, since consumer prices typically grow more slowly than wages. However, the Carter administration, organized labor, and the Social Security Administration itself preferred wage indexing; thus, the current system was born.

Converting to price indexing would be a huge step toward restoring permanent balance to Social Security. Had price indexing been implemented under Hsiao’s proposal, Social Security would have run surpluses every year from 1982 to 2023, except for 2021. There would have been temporary shortfalls starting in 2024, but by 2044, Social Security would have been running surpluses again.[32] Surpluses in Social Security could permit a reduction in the tax rate or allow some of the revenue raised from payroll taxes to support Medicare, which is also running large deficits.[33]

Higher incomes and economic growth over time enable people to save more, which reduces the need overall for a larger Social Security benefit through wage indexing. Indeed, despite claims that the US is facing a “retirement crisis,” Federal Reserve Board data from the Survey of Consumer Finances shows that retirement savings have increased within every income group since 1989, when the survey was first introduced.[34] Further, 79 percent of current retirees in another Fed survey reported they were living comfortably or doing okay financially.[35] Given this evidence, switching to price indexing would be a commonsense step toward restoring Social Security solvency.

Proposed Reforms Since the 1983 Amendments

Since the 1983 amendments, policymakers have made a handful of attempts to improve Social Security’s financing. In the late 1990s, Congress discussed creating a “lockbox” that would prevent politicians from repurposing any of the reserves in trust fund, such as for settling other government debt, but efforts were derailed due to the impeachment efforts against President Bill Clinton.[36] A similar proposal has been offered recently by Representative Tim Walberg (R-MI).[37] At best, such a reform would only delay the inevitable, which, as noted earlier, is primarily a demographic problem coupled with a benefit formula that tries to maintain fixed replacement rates over time.

President George W. Bush proposed a more substantive change to Social Security during his second term. In 2005, Bush discussed allowing younger workers to invest part of their payroll taxes into a personal account that they could manage. Although the plan was characterized as “privatizing” Social Security by its critics, the personal accounts would have been optional and managed by the government rather than the private sector.[38] Nonetheless, the proposal was not popular with the public and congressional Republicans and Bush himself soon abandoned the idea.[39]

The Bowles-Simpson Proposal

The last comprehensive effort to reform Social Security was proposed in 2010 by President Obama’s National Commission on Fiscal Responsibility and Reform, which was led by Erskine Bowles and Alan Simpson. The bipartisan Bowles-Simpson plan would have enacted changes both to the spending and revenue sides to improve Social Security financing.[40] President Obama, fearing electoral consequences from support for a large deficit reduction plan, ultimately declined to take up the commission’s recommendations. Nonetheless, the plan included many policies that analysts across the political spectrum continue to advocate for to this day.

The Bowles-Simpson plan would have made significant changes to Social Security.[41] First, it would have gradually raised both the early and full retirement ages, currently set at 62 and 67, respectively, by indexing both to life expectancy. By 2050, the full retirement age would have been 68, rising to 69 by 2075.

The plan would have made Social Security more progressive by slowing benefit growth for high-income earners. Bowles-Simpson would have gradually phased in a four-bracket structure starting in 2017 and fully phasing in by 2050. It would have reduced the share of lifetime benefits for high-income earners even further, while expanding benefits for people at the bottom. In today’s dollars, the plan would have replaced only 10 percent of monthly income between $7,562 and $12,243, and then only 5 percent of income over that threshold and up to the taxable maximum. Additionally, the plan would have created an enhanced benefit for minimum wage workers, providing a benefit equivalent to 125 percent of the poverty line.

The plan would have further changed how retirement benefits are adjusted for inflation after a retiree begins to receive them. Currently, annual Social Security benefits are adjusted for inflation using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This standard CPI measure typically overstates inflation, as it doesn’t account for consumers’ abilities to switch to relatively cheaper substitutes when the prices of certain goods rise.[42] The reform would have switched to using the chained CPI for the cost-of-living adjustments (COLA), which better captures consumption dynamics. Doing so would have slowed benefit growth and reduced the overall cost of Social Security. Notably, the 2017 tax reform switched to chained CPI for tax bracket indexing as a modest revenue raiser.

Finally, the proposal would have made changes to the revenue side as well. Currently, the payroll tax covers 83 percent of all wages earned. The Bowles-Simpson would have gradually raised the payroll tax cap to cover 90 percent of all wages earned by 2050.

While Bowles-Simpson would have solved the shorter-term funding crisis, the plan would have retained wage indexing for their new bracket bend points, and ultimately would not have resulted in permanent balance for the system.

Recent Congressional Efforts

Recent congressional proposals to reform Social Security have not been nearly as comprehensive as Bowles-Simpson, and do not address the long-term structural deficiencies in the program.

Senator Bill Cassidy (R-LA) proposed creating a separate fund that would invest in equities, like the government’s current Thrift Savings Plan for federal employees, and using the proceeds from that fund to shore up Social Security.[43] The plan would require a $1.5 trillion investment, which could be financed either by selling off state assets or borrowing.

Unfortunately, it is more likely the government would simply borrow the money. But with long-term interest rates at 4.5 percent, and the risk that the rates could go even higher, it is unlikely the investment would pay off in the long run. To put it simply, few would consider it sound financial advice to tell someone who has not saved enough for retirement to borrow money and invest in equities. If it is not responsible for an individual, it is not clear why it would be responsible for the federal government. Moreover, the government becoming such a large equity holder (under the plan, the government would control about one-third of the stock market by 2075) would entail a greater share of equity returns flowing to the government rather than private capital markets, where it could be invested more efficiently.

Proposals from congressional Democrats similarly do not fully address the Social Security financing problem. Congressman John Larson (D-CT) proposed applying the payroll tax to incomes above $400,000,[44] while Senator Bernie Sanders (I-VT) would apply the tax to incomes above $250,000.[45] Both plans would further expand benefits, in particular, by switching to the CPI-E for COLA adjustments—an inflation index for the elderly which they argue better reflects the goods and services they actually consume. The CPI-E, like the standard CPI, also overstates inflation by not adjusting for substitution. Switching to it would deplete the trust fund even further.

Ultimately, payroll tax changes alone are insufficient to place Social Security on a fiscally sustainable path. Even lifting the payroll tax cap entirely would cover little more than half of the shortfall, and Social Security would fall into deficit again within five years.[46] Moreover, lifting the cap would push federal marginal tax rates as high as 62 percent under current law, which would have damaging impacts on the economy.[47] Accounting for state taxes, top earners in New York and California would face rates north of 70 percent. Altogether, rates would be well above the revenue-maximizing rate estimated by economists and on the wrong side of the Laffer curve.[48]

What We Can Learn from Abroad

Instead of relying so heavily on tax and transfer systems, Australia, Singapore, Sweden, and Chile have transitioned to defined contribution systems. As policymakers in the United States consider solutions for Social Security, they could draw on lessons learned from the reforms in these four countries.

Australia

The Australian pension system is widely regarded as one of the “most envied” across the industrialized world as it is self-funded, generates high returns for participants, and boosts overall saving rates.[49] The system was first introduced in 1992, when Australia was facing a pension crisis due to an aging population and low saving rates overall.[50] The program has three primary components that have led to its success: a means-tested age pension, a mandatory retirement savings program, and an additional voluntary component.[51]

The means-tested age pension is similar to Social Security in that it is a defined benefit pension, but different because it provides a flat benefit up to a certain threshold. The age pension has existed in Australia since 1909 but has undergone several changes since.[52] The benefit equals about 28 percent of the average male wage for singles and 41 percent for couples.[53] The benefit is indexed to the larger of the increase in male average earnings, Australia’s CPI, or an elderly cost-of-living index.

The system maintains its progressivity by reducing the benefit for richer retirees based on income and asset tests. Altogether, about 80 percent of eligible retirees, those who are at least 67, receive some benefit, while 50 percent receive the full benefit.[54] Income tax is not owed on benefits, leading to generally high replacement rates.

The second plank of the Australian retirement system is a mandatory savings scheme, the Superannuation Guarantee. Superannuation had existed prior to the 1992 reform but had covered fewer than half of all workers.[55] The system mandates that an employer contribute 11.5 percent of their employee’s pre-tax wages, up to a specified dollar cap, to an investment fund of the employer’s choice.[56] Employees may make additional pre-tax contributions if they wish, although contributions beyond a certain cap face an additional tax of 15 percent.[57] Employees can access their funds as early as 60, and can receive their payments either as a lump sum or an annuity.[58] They may access their benefits even earlier than their retirement age if they face a “severe financial hardship” or medical emergency without incurring any additional financial penalty.[59]

To encourage additional saving, the contribution caps are relaxed under certain circumstances, and low-income earners may receive additional benefits. For employees with incomes below a certain threshold, the government will match half of every dollar in additional after-tax contributions, up to a specified amount. Proceeds from the sale of businesses may be invested in the account without incurring additional penalties, and first-time homebuyers may make contributions for such purposes without facing penalties.

Singapore

Singapore is another country with a mandatory savings scheme, which dates back to 1955 when Singapore was still under British colonialist rule.[60] The Central Provident Fund covers savings more broadly but limits personal choice in various ways.[61] The fund is split into three interest-bearing accounts: The Ordinary Account, which pays a baseline rate of 2.5 percent interest and can be used to save for housing, higher education, and other needs; the Special Account, which pays a baseline rate of 4 percent interest and covers retirement; and the Medisave Account, which pays a baseline rate of 4 percent interest and covers medical needs. Participants below age 55 can earn additional interest on their balances, up to 6 percent.[62]

More aggressive investors, who might want to seek returns higher than the interest rates these accounts pay, may invest their savings from their Ordinary and Special Accounts in other assets such as stocks and bonds, provided their total savings is above a specific threshold.[63]

The required contribution rates to the Fund are high. Employees under age 55 and employers must contribute 20 percent and 17 percent of pre-tax compensation, respectively, split across the three accounts.[64] Employers may make additional taxable contributions on behalf of their employees, and employees may also “top-up” their contributions to meet their retirement needs.[65]

At age 55, the Ordinary and Special Accounts are combined into the Retirement Account; employees may withdraw their contributions for any purpose, provided they have met the basic retirement sum, and the account continues to earn 4 percent interest.[66] At age 65, people may apply to receive a monthly annuity from their account. All withdrawals are subject to the personal income tax.[67]

Although the Singapore system is a type of defined contribution system, it is not entirely self-funding because the interest paid on the accounts is a liability to the Singaporean government. The degree of paternalism within the program, including forcing savings beyond what the typical American may be able to stomach, would make it perhaps not the ideal system for the US to emulate. Nonetheless, Singapore provides yet another successful example of what a non-pay-as-you-go retirement system could look like.

Sweden

Sweden was once in a similar position to what the US is in now. In the late 1980s, actuarial estimates showed Sweden’s then pay-as-you-go system was approaching a crisis due to rising life expectancies and low economic growth, which reduced payroll tax revenue.[68] The Swedish Parliament then pursued a comprehensive reform of the program in the 1990s. First, Sweden added a fully funded defined contribution system, with the government withholdingWithholding is the income an employer takes out of an employee’s paycheck and remits to the federal, state, and/or local government. It is calculated based on the amount of income earned, the taxpayer’s filing status, the number of allowances claimed, and any additional amount of the employee requests.

2.3 percent of pre-tax wages and placing it into individual pension accounts.[69] Workers could choose from up to five different funds to invest their money, based on their own appetite for risk. The average return since 1995 has been nearly 10 percent.

In addition, employees would be required to contribute 16 percent of their pre-tax wages to a hybrid pay-as-you-go system, with the funds deposited into “notional” accounts.[70] The benefits are based on contributions from lifetime earnings, like standard defined contribution plans, and the annuities paid reflect changes in life expectancy. Upon retirement, the annuity is calculated by dividing the accumulated assets by the unisex life expectancy. The account is indexed for average per capita earnings, so it generally rises with the growth of the economy. Because of the indexing, the account is not fully funded like typical defined contribution pensions.[71]

In the event the government is unable to meet its obligations, an adjustment mechanism automatically reduces indexation until balance is restored.[72] This adjustment mechanism ensures that the government can continue to meet its obligations without needing to increase the contribution rate or alter the normal retirement age. It has only been activated once, in 2010 following the 2008 financial crisis, and the standard indexing rules were reapplied in 2019.

Individuals may begin drawing from their notional accounts as early as 63 and do not need to stop working to draw benefits. For this reason, Sweden generally has a flexible retirement age. Workers are “entitled to work” until they are age 69, at which point, if they want to work longer, they must receive approval from their employer.[73] Though if an individual retires before the full retirement age, their benefits will be smaller because the pension is based on the assets at retirement and the expected remaining life length. All withdrawals are subject to Sweden’s personal income tax.

Finally, a guaranteed pension that is not based on earnings supplements the system, functioning as a safety net for low-income workers, and those annuities are also taxed.[74] It is financed from general revenues, and generally “tops up” the pension a worker already receives through the notional accounts to ensure they meet a minimum baseline. Unlike withdrawals from the notional accounts, a worker cannot begin receiving the guaranteed pension until they turn 65.

One issue with any structural reform of this size is how to handle the transition to a new system. Under the old Swedish defined benefit system, retirees received a flat-rate pension based on 60 percent of an average of their highest 15 years in earnings.[75] People born before 1938 continued to receive their benefits based on the old formula, although their benefits were indexed based on new rules to keep costs down. People born between 1938 and 1953, the earliest of which turned 65 in 2003, began to receive benefits under a combination of both the old and new rules.

Some may argue that the viability of any pension reform depends on a country’s starting place. Australia already had superannuation in place, for instance, and Singapore did not have an ailing pension system before implementing its reform. But Sweden provides a definitive example of how a country can achieve radical reforms even when the risks of transitioning seem insurmountable from the outset.

Chile

Prior to 1980, Chile had a pay-as-you-go retirement system, where contributions were paid into a collective capitalization fund. The funds were poorly managed, and contribution rates reached nearly 26 percent of wages by 1973.[76] The fund was rapidly approaching insolvency, with the present value of the liabilities exceeding 100 percent of GDP by 1971. The problems were further compounded by a declining worker-to-retiree ratio, falling to 2.5 by 1979.

The Chilean government responded to the crisis by privatizing the entire system in 1980. Participation in the new system was mandatory for people who worked for an employer, but people could choose which private pension administrators (the Administradoras de Fondo de Pensiones, or AFPs) would manage their funds. Upon retirement, retirees could choose to purchase an annuity from an insurance or withdraw their funds based on another actuarily fair schedule, both of which are subject to Chile’s personal income tax. Contribution rates were lowered to 10 percent.

While the system was largely privatized, the government still played a role in ensuring that retirees would have sufficient savings for retirement. First, they guaranteed a minimum pension for low-wage employees, equal to 85 percent of the minimum wage. Second, they would regulate the types of assets in which workers could invest, although these rules have been increasingly relaxed over time.

By 1998, the reformed retirement system covered nearly 62 percent of the workforce. The remaining were either self-employed workers, who had the option to participate in retirement accounts, or the informal sector. Between 1985 and 1997, private managed funds increased from 10 percent to almost 45 percent of GDP.

The system also included a “backstop” to ensure retirees see adequate returns each year. In any year, an AFP cannot pay a return lower than 2 percentage points of the system’s average. If this happens, the difference is made up from a reserve fund. Initially, this minimum floor for returns, and the fact that each AFP cannot offer more than one fund, reduced competition and resulted in most AFPs having similar portfolios for the first two decades of Chile’s reformed system. However, deregulatory efforts in the 2000s allowed AFPs to offer a second fund, and this has been expanded further to five funds based on differing levels of risk.[77]

To handle the transition to the new system and attempt to fulfill obligations to contributors under the old system, Chile issued bonds to those workers who were placed in an individual retirement account and earned 4 percent interest. The principal for each bond was based on a formula accounting for how much the worker had contributed under the previous system. The transitional costs were expensive, reaching 5 percent of GDP by 1983, but by the mid-2010s, the government had fulfilled its remaining obligations.[78]

The Chilean retirement system, like any retirement system, is not perfect. Further reforms are necessary. To start, the pension system is still overregulated, and in some instances, this has led to worse outcomes for retirees. One study found that while one of the funds offered was designed to be the riskiest, and therefore provide the highest return, it delivered returns inconsistent with its risk profile.[79] One analysis found that the regulations have led to suboptimal asset allocations and reduced returns by as a much as 2 percentage points.[80]

Increasing the contribution rate will also be necessary to increase replacement rates and ensure workers are adequately saving enough.[81] The Chilean contribution rate of 10 percent is well below the OECD average of 19 percent.[82] Moreover, the current retirement age, 65 for men and 60 for women, has not been raised since 1924, even as life expectancy in the country has risen.[83] These factors, compounded with Chile’s large informal sector (which is exempt from the mandatory contributions), suggest many Chileans have not saved enough for retirement.[84]

Nevertheless, despite recent attempts by Chile’s new left-of-center government under Gabriel Boric to replace the system with a traditional defined benefit pension, Chileans like that they own their accounts and that it gives them something to pass onto their heirs.[85] If anything, the proposed reforms are more likely to move in the direction of Sweden’s hybrid system to preserve the individual accounts for workers.

Conclusion

For the past few decades, politicians have been reluctant to change anything fundamental in the Social Security system, even though the system is rapidly approaching insolvency. This situation is not unique to the US, as other countries have similarly struggled to fund their defined benefit systems amidst aging populations and declining worker-per-retiree ratios. The Bowles-Simpson framework provided a good starting point, but to truly solve the funding problem, we will have to look at more fundamental solutions, including successful reforms in other countries. The financial health of future retirees, and of the US federal government, depends on it.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

[1] Congressional Budget Office, The Federal Budget in Fiscal Year 2023: An Infographic, Mar. 5, 2024, https://www.cbo.gov/publication/59727.

[2] Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, The 2024 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, Social Security Administration, May 6, 2024, https://www.ssa.gov/OACT/TR/2024/tr2024.pdf.

[3] Ibid.

[4] Garrett Watson, “Exempting Social Security Benefits from Income Tax Is Unsound and Fiscally Irresponsible,” Tax Foundation, Aug. 2, 2024, https://taxfoundation.org/blog/trump-social-security-tax/.

[5] Sean Williams, “Kamala Harris on Social Security: 10 things you need to know,” USA Today, Aug. 4, 2024, https://www.usatoday.com/story/money/2024/08/04/kamala-harris-on-social-security-10-things-you-need-to-know/74577592007/.

[6] Social Security Administration, “COLA Fact Sheet 2024,” https://www.ssa.gov/news/press/factsheets/colafacts2024.pdf.

[7] Ibid.

[8] Social Security Administration, “Social Security Benefits Amounts,” https://www.ssa.gov/OACT/COLA/Benefits.html.

[9] Social Security and Medicare Boards of Trustees, “A Summary of the 2024 Annual Reports,” Social Security Administration, https://www.ssa.gov/OACT/TRSUM/index.html.

[10] Social Security Administration, “Normal Retirement Age,” https://www.ssa.gov/OACT/ProgData/nra.html

[11] Social Security Administration, “Social Security Benefits Amounts,” https://www.ssa.gov/OACT/COLA/Benefits.html.

[12] Social Security Administration. “Primary Insurance Amount,” https://www.ssa.gov/OACT/COLA/piaformula.html.

[13] Social Security Administration, “Contribution and Benefit Base,” https://www.ssa.gov/oact/cola/cbb.html.

[14] Social Security and Medicare Boards of Trustees, “The 2024 OASDI Trustees Report,” https://www.ssa.gov/OACT/TR/2024/tr2024.pdf; see Table VI.D4.

[15] Ibid. See Table V.C7.

[16] Social Security Administration, “Social Security History: Ratio of Social Security Covered Workers to Beneficiaries Calendar Years 1940-2013,” https://www.ssa.gov/history/ratios.html.

[17] Peter G. Peterson Foundation, “The Ratio of Workers to Social Security Beneficiaries is at a Low and Projected to Decline Further,” Aug. 4, 2022, https://www.pgpf.org/blog/2022/08/the-ratio-of-workers-to-social-security-beneficiaries-is-at-a-low-and-projected-to-decline-further.

[18] Social Security and Medicare Boards of Trustees, “A Summary of the 2024 Annual Reports,” Social Security Administration, https://www.ssa.gov/OACT/TRSUM/index.html.

[19] Edward Lazear, “The Muth of the Great Wages Decoupling,” Hoover Institution, Mar. 6, 2014, https://www.hoover.org/research/myth-great-wages-decoupling.

[20] C. Eugene Steuerle and Karen E. Smith, “Social Security and Medicare Benefits and Taxes: 2023,” Urban Institute, July 2023, https://www.urban.org/sites/default/files/2023-12/social_security_medicare_tpc.pdf#page=25.

[21] Gopi Shah Goda and Andrew Biggs, “Strengthening the Social Security safety net,” Stanford Institute for Economic Policy Research, April 2023, https://www.aei.org/wp-content/uploads/2023/04/SIEPR-Policy-Brief-April-2023.pdf?x85095.

[22] James Girola, “The Long-Term Real Interest Rate for Social Security,” U.S. Department of Treasury, 2005, https://home.treasury.gov/system/files/226/long-term-rates-socialsecurity.pdf; James Royal, “What is the Average Stock Market Return,” NerdWallet, May 3, 2024, https://www.nerdwallet.com/article/investing/average-stock-market-return.

[23] Social Security Administration, “Fact Sheet: Social Security,” https://www.ssa.gov/news/press/factsheets/basicfact-alt.pdf#:~:text=%CE%BF%20Social%20Security%20benefits%20represent%20about%2030%25%20of,Security%20for%2090%25%20or%20more%20of%20their%20income.

[24] Pension Rights Center, “How many American workers participate in workplace retirement plans?,” Oct. 23, 2023, https://pensionrights.org/resource/how-many-american-workers-participate-in-workplace-retirement-plans/.

[25] Andrew Van Dam, “How Inheritance Data Secretly Explains U.S. Inequality,” The Washington Post, Nov. 10, 2023, https://www.washingtonpost.com/business/2023/11/10/inheritance-america-taxes-equality/.

[26] Dylan Matthews “The bizarre true story of the last time America raised its retirement age,” Apr. 21, 2023, https://www.vox.com/policy/2023/4/21/23663654/social-security-retirement-age-1983-greenspan-ball.

[27] Gopi Shah Goda and Andrew Biggs, “Strengthening the Social Security safety net,” Stanford Institute for Economic Policy Research, April 2023, https://www.aei.org/wp-content/uploads/2023/04/SIEPR-Policy-Brief-April-2023.pdf?x85095.

[28] Office of the Actuary Social Security Administration, “Summary of the 1984 Trustees Report,” Apr. 5, 1984, https://www.ssa.gov/oact/TRSUM/historical/1984.pdf.

[29] Boards of Trustees, “Status of the Social Security and Medicare Programs: A Summary of the 1993 Annual Reports,” Social Security Administration, https://www.ssa.gov/history/pdf/1993.pdf.

[30] Stephen J. Entin, “A Simple Change to Restore Social Security Solvency,” Tax Foundation, September 2015, https://files.taxfoundation.org/legacy/docs/TaxFoundation_FF478.pdf.

[31] US Government Printing Office, “Report of the Consultant Panel on Social Security to the Congressional Research Service,” August 1976, http://www.socialsecurity.gov/history/reports/hsiao/hsiaoIntro.html.

[32] John Cogan and Daniel Heil, “Social Security Wage Indexing Revisited,” Hoover Institution, 2023, https://www.hoover.org/sites/default/files/research/docs/23116-Cogan-Heil.pdf.

[33] Stephen J. Entin, “A Simple Change to Restore Social Security Solvency,” Tax Foundation, September 2015, https://files.taxfoundation.org/legacy/docs/TaxFoundation_FF478.pdf.

[34] Andrew Biggs, “Changes to Household Retirement Savings since 1989,” American Enterprise Institute, 2020, https://www.aei.org/wp-content/uploads/2020/05/Changes-to-Household-Retirement-Savings-Since-1989.pdf.

[35] Federal Reserve Board, “Economic Well-Being of U.S. Households in 2023,” https://www.federalreserve.gov/consumerscommunities/shed.htm.

[36] CBS News, “Social Security Lock Box,” May 22, 1999, https://www.cbsnews.com/news/social-security-lock-box/.

[37] Office of Rep. Tim Walberg, “Social Security,” https://walberg.house.gov/issues/social-security.

[38] Charles Blahous, “Correcting the Historical Record on President Bush’s Social Security Reform Efforts,” Hoover Institution, May 26, 2011, https://www.hoover.org/research/correcting-historical-record-president-bushs-social-security-reform-efforts.

[39] William A. Galston, “Why the 2005 Social Security Initiative Failed, and What it Means for the Future,” Brookings Institution, Sep. 21, 2007, https://www.brookings.edu/articles/why-the-2005-social-security-initiative-failed-and-what-it-means-for-the-future/.

[40] Alex Durante, “Tackling America’s Debt and Deficit Crisis Requires Social Security and Medicare Reform,” Tax Foundation, May 23, 2023, https://taxfoundation.org/blog/medicare-social-security-reform-us-debt-deficits/.

[41] The National Commission on Fiscal Responsibility and Reform, “The Moment of Truth,” December 2010, https://web.archive.org/web/20121214121412/http:/www.fiscalcommission.gov/sites/fiscalcommission.gov/files/documents/TheMomentofTruth12_1_2010.pdf.

[42] Rob McClelland, “Differences Between the Traditional CPI and the Chained CPI,” Congressional Budget Office, Apr. 19, 2023, https://www.cbo.gov/publication/44088.

[43] Office of Sen. Bill Cassidy, “ICYMI: We Can Fix Social Security Before it Reaches the Fiscal Cliff,” Mar. 8, 2024, https://www.cassidy.senate.gov/newsroom/press-releases/icymi-we-can-fix-social-security-before-it-reaches-the-fiscal-cliff/.

[44] Congressman John B. Larson, “Social Security 2100: A Sacred Trust,” https://larson.house.gov/sites/evo-subsites/larson.house.gov/files/Social%20Security%202100%20-%20Fact%20Sheet%20117th.pdf.

[45] Office of Sen. Bernie Sanders, “The Right to a Secure Retirement,” https://berniesanders.com/issues/expand-social-security/.

[46] Social Security Administration, “Financial Estimates for the OASDI Trust Fund Program,” https://www.ssa.gov/OACT/solvency/provisions/tables/table_run131.html.

[47] Tax Foundation, “Options for Reforming America’s Tax Code 2.0,” 2021, https://taxfoundation.org/research/federal-tax/tax-reform-options/?option=34.

[48] Brian Riedl, “The Limits of Taxing the Rich,” Manhattan Institute, Sep. 21, 2023, https://manhattan.institute/article/the-limits-of-taxing-the-rich.

[49] Rachael Rosel, “Official super numbers show why Aussie system is ‘envy of the world’,” StartsAt60, Aug. 25, 2020, https://startsat60.com/media/money/retirement-income/superannuation-returns-investment-apra-june-2020.

[50] Patrick Collinson, “Australia May Hold Key to Pensions,” The Guardian, Oct. 11, 2004, https://www.theguardian.com/money/2004/oct/12/business.australia.

[51] Julie Agnew, “Australia’s retirement system: Strengths, weaknesses, and reforms,” Center for Retirement Research at Boston College, April 2013, https://dlib.bc.edu/islandora/object/bc-ir:104693/datastream/PDF/view.

[52] Rafal Chonik and John Piggott, “Chapter 14: The Australian Retirement Income System: Comparisons with and Lessons for the United States,” Pension Research Council, Nov. 12, 2015, https://pensionresearchcouncil.wharton.upenn.edu/wp-content/uploads/2017/05/Chapter-14.pdf.

[53] Ibid.

[54] Ibid.

[55] Ibid.

[56] Australian Taxation Office, “How much super to pay,” Jun. 30, 2024, https://www.ato.gov.au/businesses-and-organisations/super-for-employers/paying-super-contributions/how-much-super-to-pay.

[57] SuperGuide, “Key superannuation rates and thresholds for 2024-2025,” Jul. 1, 2024, https://www.superguide.com.au/how-super-works/super-rates-and-thresholds.

[58] Jim Hennington, “Making sense of Australia’s Retirement Age Rules,” Jubilacion Australia, Feb. 7, 2023, https://jubilacion.com.au/retirement-age-rules/.

[59] Australian Taxation Office, “When You Can Access Your Super Early,” https://www.ato.gov.au/individuals-and-families/super-for-individuals-and-families/super/withdrawing-and-using-your-super/early-access-to-super/when-you-can-access-your-super-early, accessed Sep. 12, 2024.

[60] Singapore National Library Board, “Central Provident Fund is Introduced, https://www.nlb.gov.sg/main/article-detail?cmsuuid=c2330166-bd07-4266-a073-11e8d8efa4e8#2, accessed Sep. 12, 2024.

[61] Lee Kuan Yew School of Public Policy, “Saving the CPF: Restoring public trust in Singapore’s retirement savings system,” National University of Singapore, https://lkyspp.nus.edu.sg/docs/default-source/case-studies/cpf-case_final_feb2015.pdf?sfvrsn=eac0960b_2.

[62] Ministry of Manpower, “What is the Central Provident Fund (CPF),” https://www.mom.gov.sg/employment-practices/central-provident-fund/what-is-cpf.

[63] Ministry of Manpower, “How you can use your CPF,” https://www.mom.gov.sg/employment-practices/central-provident-fund/how-you-can-use-your-cpf.

[64] Central Provident Fund Board, “How much CPF contributions to pay,” Apr. 1, 2024, https://www.cpf.gov.sg/employer/employer-obligations/how-much-cpf-contributions-to-pay.

[65] Central Provident Fund Board, “Boost Your Retirement Savings with Cash Top-Ups and CPF Transfers,” Sep. 12, 2024, https://www.cpf.gov.sg/member/growing-your-savings/saving-more-with-cpf/top-up-to-enjoy-higher-retirement-payouts.

[66] Central Provident Fund Board, “How CPF works,” https://www.cpf.gov.sg/member/cpf-overview.

[67] Inland Revenue Authority of Singapore, “Lump Sum Payments,” Sep. 12, 2024, https://www.iras.gov.sg/taxes/individual-income-tax/employers/understanding-the-tax-treatment/lump-sum-payments.

[68] Edward Palmer, “Swedish Pension Reform: How Did It Evolve, and What Does It Mean for the Future?,” National Bureau of Economic Research, January 2002, https://www.nber.org/system/files/chapters/c10673/c10673.pdf.

[69] Johan Norberg, “How Sweden Saved Social Security,” Cato Institute, Feb. 22, 2023, https://www.cato.org/commentary/how-sweden-saved-social-security.

[70] Edward Palmer, “Swedish Pension Reform: How Did It Evolve, and What Does It Mean for the Future?,” National Bureau of Economic Research, January 2002, https://www.nber.org/system/files/chapters/c10673/c10673.pdf.

[71] Regeringskansliet, “The Swedish pension system and pension projections until 2070,” Dec. 10, 2020, https://economy-finance.ec.europa.eu/system/files/2021-05/se_-_ar_2021_final_pension_fiche.pdf.

[72] Ibid.

[73] Nordic Co-operation, “Retirement Pension in Sweden,” https://www.norden.org/en/info-norden/retirement-pension-sweden, accessed Sep. 12, 2024.

[74] Hanna Aspegren et al., “Pension Reform in Sweden: Sustainability & Adequacy of Public Pensions,” European Commission, July 2019, https://economy-finance.ec.europa.eu/system/files/2020-11/eb048_en.pdf.

[75] Regeringskansliet, “The Swedish pension system and pension projections until 2070,” Dec. 10, 2020, https://economy-finance.ec.europa.eu/system/files/2021-05/se_-_ar_2021_final_pension_fiche.pdf.

[76] Sebastian Edwards and Alejandra Cox Edwards, “Social Security Privatization and Labor Markets: The Case of Chile,” 2002, https://www.anderson.ucla.edu/sites/default/files/document/2022-12/ss%20reform.pdf.

[77] Arturo Cifuentes, “Chile’s pioneering pension system now needs reform,” Financial Times, Dec. 28, 2023, https://www.ft.com/content/7f2c2d17-8b47-4ad3-bf9a-6e342e6d66c6.

[78] Ibid.

[79] Bernardo Pagnoncelli et al., “A Useful (But Painful) Risk-Management Lesson from the Chilean Pension System,” Portfolio Management Research, May 17, 2023, https://www.pm-research.com/content/iijretire/early/2023/05/17/jor20231135.

[80] Arturo Cifuentes, “Chile’s pioneering pension system now needs reform,” Financial Times, Dec. 28, 2023, https://www.ft.com/content/7f2c2d17-8b47-4ad3-bf9a-6e342e6d66c6.

[81] Samuel Pienknagura and Christopher Evans, “Assessing Chile’s Pension System: Challenges and Reform Options,” International Monetary Fund, Sep. 10, 2021, https://www.imf.org/en/Publications/WP/Issues/2021/09/09/Assessing-Chile-s-Pension-System-Challenges-and-Reform-Options-465415.

[82] Sebastian Edwards, The Chile Project: The Story of the Chicago Boys and the Downfall of Neoliberalism (Princeton, NJ: Princeton University Press, 2023), 244.

[83] Cecilia Cifuentes, “Untangling Chile’s Pension Reform,” Americas Quarterly, Jun. 26, 2024, https://www.americasquarterly.org/article/untangling-chiles-pension-reform/.

[84] Sebastian Edwards, The Chile Project: The Story of the Chicago Boys and the Downfall of Neoliberalism (Princeton, NJ: Princeton University Press, 2023), 244-245.

[85] Ibid, 252.

Share