Topline Preliminary Estimates

- 10-Year Revenue (Billions) +$1,697

- Long-run GDP -2.0%

- Long-Run Wages -1.2%

- Long-Run FTE Jobs -786,000

Tax Foundation General Equilibrium Model, September 2024.

With less than two months left in the 2024 presidential campaign, Vice President Kamala Harris has sketched out sufficient details of her fiscal and economic agenda for us to provide a preliminary analysis of the budgetary, economic, and distributional effects. On taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

policy, Harris carries forward much of President Biden’s FY 2025 budget, including higher taxes aimed at businesses and high earners. She would also further expand the child tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

(CTC) and various other tax credits and incentives while exempting tips from income tax.

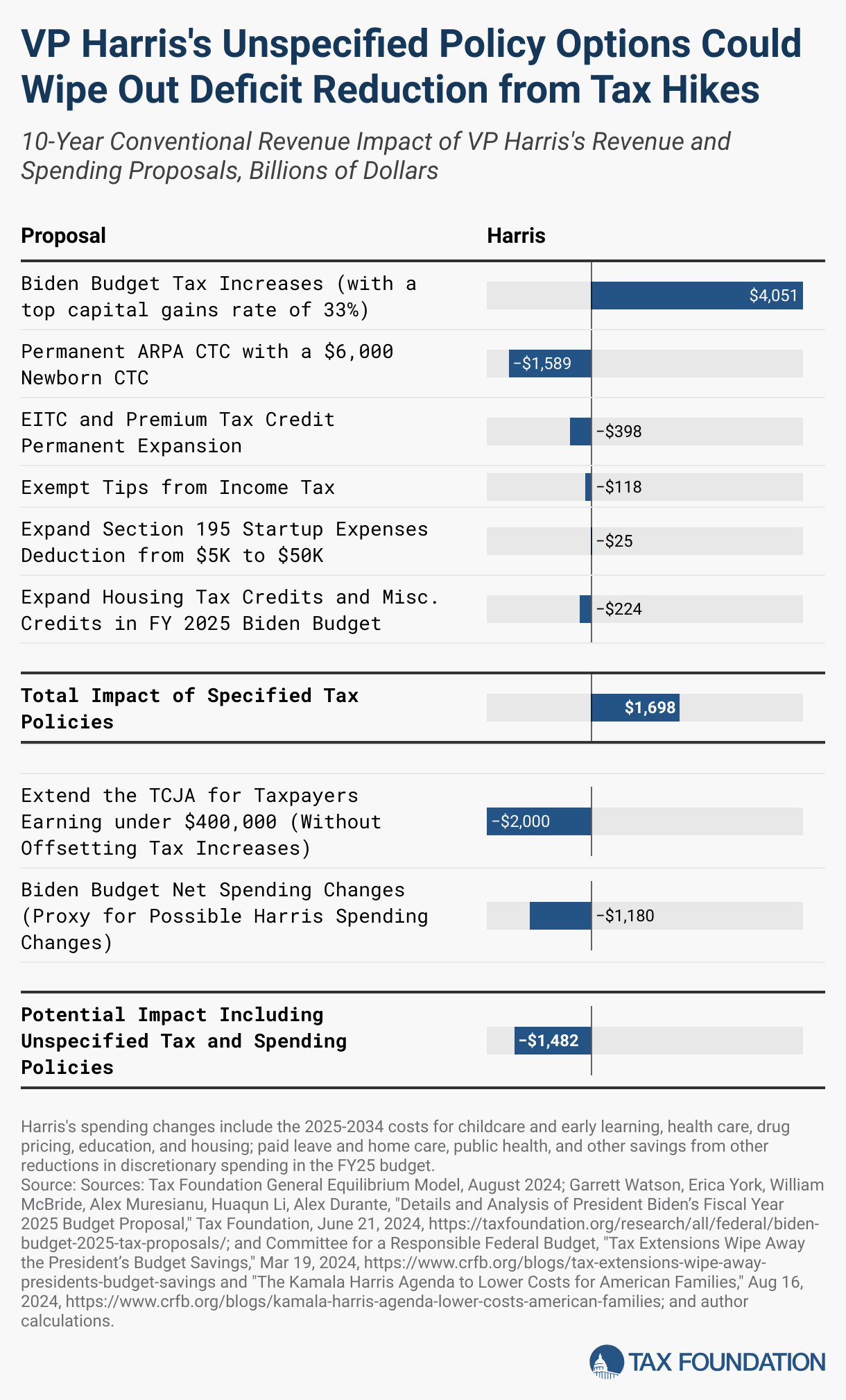

On a gross basis, we estimate that Vice President Harris’s proposals would increase taxes by about $4.1 trillion from 2025 to 2034. After taking various credits and tax cuts into account, Harris would raise about $1.7 trillion over 10 years on a conventional basis, and after factoring in reduced revenue from slower economic growth, the net revenue increase comes to $642 billion. We estimate the proposed tax changes would reduce long-run GDP by 2.0 percent, the capital stock by 3.0 percent, wages by 1.2 percent, and employment by about 786,000 full-time equivalent jobs.

We find the tax policies would raise top tax rates on corporate and individual income to among the highest in the developed world, slowing economic growth and reducing competitiveness. The tax credits and other carveouts would complicate the tax code, run more spending through the IRS, and, together with various price controls, fail to improve affordability challenges in housing and other sectors.

Many tax policies remain unspecified, including how Harris might deal with next year’s expiration of the Tax Cuts and Jobs Act (TCJA). Harris has not clearly indicated if or how her spending priorities align with the FY 2025 budget proposals. Depending on where she lands on these issues, the deficit impacts could be large.

In a possible scenario in which she extends the TCJA for all those earning under $400,000 and adopts all the spending proposals specified in the FY 2025 budget, we estimate the net effect of her policies would increase deficits by $1.5 trillion over the next decade, measured on a conventional basis. Including the economic impacts of the tax increases, the net effect could increase deficits by roughly $2.6 trillion over the next decade.

The wide range of possibilities reflects considerable uncertainty about her fiscal policy stance at this point, leaving a large void regarding how she might deal with the already unprecedented, dangerous, and unsustainable federal debt trajectory.

Detailed Harris Tax Proposals

Harris’s tax plan relies on higher taxes on businesses and high earners to raise new revenues as outlined in President Biden’s FY 2025 budget with some revisions (to capital gains taxes, as noted), combined with several tax credits. All provisions are modeled as starting in calendar year 2025 unless otherwise noted.

Major business provisions modeled:

- Increase the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

rate from 21 percent to 28 percent - Increase the corporate alternative minimum tax introduced in the InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

Reduction Act from 15 percent to 21 percent - Quadruple the stock buyback tax implemented in the Inflation Reduction Act from 1 percent to 4 percent

- Make permanent the excess business loss limitation for pass-through businesses

- Further limit the deductibility of employee compensation under Section 162(m)

- Increase the global intangible low-taxed income (GILTI) tax rate from 10.5 percent to 21 percent, calculate the tax on a jurisdiction-by-jurisdiction basis, and revise related rules

- Repeal the reduced tax rate on foreign-derived intangible income (FDII)

Major individual, capital gains, and estate taxAn estate tax is imposed on the net value of an individual’s taxable estate, after any exclusions or credits, at the time of death. The tax is paid by the estate itself before assets are distributed to heirs.

provisions modeled:

- Expand the base of the net investment income tax (NIIT) to include nonpassive business income and increase the rates for the NIIT and the additional Medicare tax to reach 5 percent on income above $400,000

- Increase top individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

rate to 39.6 percent on income above $400,000 for single filers and $450,000 for joint filers - Tax long-term capital gains and qualified dividends at 28 percent (as opposed to 39.6 percent as in the Biden budget) for taxable incomeTaxable income is the amount of income subject to tax, after deductions and exemptions. For both individuals and corporations, taxable income differs from—and is less than—gross income.

above $1 million and tax unrealized capital gains at death above a $5 million exemption ($10 million for joint filers) - Limit retirement account contributions for high-income taxpayers with large individual retirement account (IRA) balances

- Tighten rules related to the estate tax

- Tax carried interest as ordinary income for people earning more than $400,000

- Limit 1031 like-kind exchanges to $500,000 in gains

- Exempt tipped income from income taxation for occupations where tips are currently customary

- Expand the Section 195 deduction limit for startup expenses from $5,000 to $50,000.

Major tax credit provisions modeled:

- Revive and make permanent the American Rescue Plan Act (ARPA) child tax credit (CTC) and increase the CTC for newborns to $6,000 in the first year of life

- Permanently extend the ARPA earned income tax credit (EITC) expansion for workers without qualifying children

- Provide a $25,000 tax credit for first-time homebuyers over four years

We also modeled various miscellaneous provisions for corporations, pass-through businesses, and individuals, including several energy-related tax hikes largely pertaining to fossil fuel production. While the Biden budget improperly characterized fossil fuel provisions as subsidies, many are deductions for costs (or approximations of costs) incurred.

Major provisions not modeled by us, but included in total fiscal impacts based on Biden administration estimates:

- Repeal the base erosion and anti-abuse tax (BEAT) and replace it with an undertaxed profits rule (UTPR) consistent with the Organisation for Economic Co-operation and Development (OECD)/G20 global minimum tax model rules

- Replace FDII with unspecified research and development (R&D) incentives

- Create a 25 percent “billionaire minimum tax” to tax unrealized capital gains of high-net-worth taxpayers

- Permanently extend the ARPA premium tax credits (PTCs) expansion (we do include PTCs in our distributional analysis)

- Changes to tax compliance and administration

Long-Run Economic Effects of Vice President Harris’s Tax Proposals

We estimate the tax changes in Harris’s tax proposals would reduce long-run GDP by 2.0 percent, the capital stock by 3.0 percent, wages by 1.2 percent, and employment by about 786,000 full-time equivalent jobs. Harris’s tax proposals would decrease American incomes (as measured by gross national product, or GNP) by 1.8 percent in the long run, reflecting offsetting effects of increased taxes and reduced deficits, as debt reduction reduces interest payments to foreign owners of the national debt.

Raising the corporate income tax rate to 28 percent is the largest driver of the negative effects, reducing long-run GDP by 0.6 percent, the capital stock by 1.1 percent, wages by 0.5 percent, and full-time equivalent jobs by 125,000.

Our economic estimates likely understate the effects of the Harris tax plan since they exclude two novel and highly uncertain yet large tax increases on high earners and multinational corporations, namely a new minimum tax on unrealized capital gains and a UTPR consistent with the OECD/G20 global minimum tax model rules. Nor do we include the proposed unspecified R&D incentives that would replace the lower tax rate on foreign-derived intangible income FDII.

Revenue and Debt Effects of Vice President Harris’s Tax Proposals

Across the major provisions modeled by Tax Foundation, we estimate that Harris’s tax plan would raise $2.2 trillion of tax revenue from corporations and $1.2 trillion from individuals from 2025 through 2034.

For tax proposals from the Biden FY 2025 budget, we relied on estimates from the White House Office of Management and Budget (OMB) for provisions we did not model, including the billionaire minimum tax, UTPR, various international tax changes for oil and gas companies, smaller international tax changes, improvements to tax compliance and administration, and unspecified R&D incentives to replace FDII.

In total, accounting for all provisions, we estimate the budget would raise just over $4.1 trillion in gross revenue from tax changes over the 10-year budget window.

Tax cuts, like the tax exemptionA tax exemption excludes certain income, revenue, or even taxpayers from tax altogether. For example, nonprofits that fulfill certain requirements are granted tax-exempt status by the Internal Revenue Service (IRS), preventing them from having to pay income tax.

for tip income, the expanded deduction for startup expenses, and the unspecified incentive to replace FDII, reduce gross revenue by $235 billion, while expanded tax credits reduce the revenue by another $2.2 trillion. This results in a net tax increase of about $1.7 trillion over 10 years on a conventional basis.

On a dynamic basis, factoring in reduced tax revenues resulting from the smaller economy, we estimate Harris’s tax plan would raise about $642 billion over 10 years.

The economic harm from Harris’s tax hikes would also greatly reduce the ability to address an emerging debt crisis. Under current law, the debt-to-GDP ratio will hit 201 percent in 40 years, while the Harris tax plan on a conventional basis would reduce the debt-to-GDP ratio to 189 percent. However, after factoring in reduced tax collections and a smaller economy, the debt-to-GDP ratio would decline only slightly, to 200 percent.

Adding more uncertainty and potentially increasing deficits substantially, Harris may extend the TCJA for people making under $400,000, as the FY 2025 budget mentions but does not formally include in the budget accounting. Harris could accomplish TCJA extension in many ways, but all possibilities would likely have a high fiscal cost, given that about 98 percent of taxpayers earn less than $400,000.

For instance, the Committee for a Responsible Federal Budget has estimated the cost of TCJA permanence for people earning less than $400,000 could range from about $1.5 trillion to $2.5 trillion over 10 years.

Nor has Vice President Harris specifically outlined her proposed changes to federal spending. While we do not assume a specific spending plan as part of our formal score, Harris has proposed investing in affordable childcare and long-term care programs, among other unspecified spending proposals, which would reduce net revenue collection further.

To tally up the range of potential deficit impacts from Harris’s proposals, we include as a proxy for potential spending the net change in spending under the FY 2025 budget of $1.18 trillion covering childcare and early learning, health care, drug pricing, education, and housing; paid leave and home care; public health; and some additional savings from other reductions in discretionary spending (note that we only include the spending changes over the 10-year budget window).

Assuming $1.18 trillion of additional spending and a $2 trillion revenue loss for TCJA extension, Harris’s combined fiscal policies could add as much as $1.5 trillion to deficits over the next decade on a conventional basis.

Under this scenario, and after accounting for the economic effects of the tax increases, we estimate deficits could increase by roughly $2.6 trillion over the next decade on a dynamic basis.

Alternatively, Harris could specify additional tax increases to offset the cost of TCJA extension, which would have additional negative impacts on the economy, or Harris could simply allow the TCJA to expire. Harris could also abandon part or all of the FY 2025 spending proposals.

Distributional Effects of Vice President Harris’s Tax Proposals

Vice President Harris’s tax plan would raise marginal income tax rates faced by higher earners and corporations while expanding tax credits for lower-income households, resulting in substantially increased redistribution of income through the tax code. Our modeling of the distributional effects on after-tax incomeAfter-tax income is the net amount of income available to invest, save, or consume after federal, state, and withholding taxes have been applied—your disposable income. Companies and, to a lesser extent, individuals, make economic decisions in light of how they can best maximize their earnings.

only includes specified tax proposals and does not include the impact of drug pricing provisions, the 25 percent billionaire minimum tax, the undertaxed profits rule, miscellaneous tax credits, IRS enforcement, or spending program changes.

The Harris tax plan would redistribute income from high earners to low earners. The bottom 60 percent of earners would see increases in after-tax income in 2025, while the top 40 percent of earners would see decreases. After-tax income for the bottom quintile would increase by 16.5 percent, largely from expanded tax credits. In contrast, the top 1 percent of earners would experience a 9.5 percent decrease in after-tax income.

The bottom quintile would see a slightly smaller 13.6 percent increase in after-tax income in 2034 on a conventional basis, while the top two quintiles would see decreases in their after-tax incomes. The top 1 percent would see a 7.3 percent decrease in after-tax income.

On a long-term dynamic basis, the smaller economy would reduce after-tax incomes relative to the conventional analysis. On average, tax filers in the top three quintiles would experience a drop in after-tax incomes, while the bottom quintile would still see an increase, albeit reduced to 11.8 percent, driven by the permanent changes to the CTC, EITC, and PTC.

Analysis of Harris’s Tax Credit and Tax Cut Proposals

Like the Biden administration, Harris’s tax plan puts a heavy emphasis on tax credits. Harris would restore the CTC expansion under the 2021 American Rescue Plan Act, which increased the credit from $2,000 under current law to $3,000 for older children and $3,600 for younger children for 2021 only. She would further increase the credit amount for newborns to $6,000, resulting in a CTC that provides $6,000 for children under one year old, $3,600 for children two through five, and $3,000 for children six and older. The ARPA expansion also removed work and income requirements to claim the credit, providing the maximum credit to qualifying individuals regardless of whether they had earned income, thus much of the expansion is technically spending administered by the IRS.

Tax Foundation estimates Harris’ CTC expansion would cost about $1.6 trillion over 10 years on a conventional basis. The expansion would shrink long-run economic output by about 0.1 percent by removing the credit’s phase-in and lengthening the credit’s phaseout, thus raising marginal tax rates for workers along both ranges. The smaller economy would result in further revenue losses for the federal government, increasing the fiscal cost to $1.7 trillion over the next decade.

Harris would extend or make permanent the expansion of health insurance PTC subsidies enacted under ARPA, which are set to expire at the end of 2025, and expand the EITC for single and joint filers who do not claim children on their tax returns. Over 10 years, permanence for the PTCs would cost about $238 billion, and the EITC expansion about $160 billion.

Harris also proposes several new housing tax incentives and penalties. For housing construction, she would expand the low-income housing tax credit (a similar proposal in the FY 2025 budget would cost $37 billion over a decade) and create a tax credit for the construction of starter homes. However, Harris would limit deductions for interest and depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment.

for large property investors.

Expanding a proposal in the FY 2025 budget, the Harris campaign proposes providing an average of $25,000 for all eligible first-time homebuyers, with additional support for first-generation homebuyers. Depending on how the subsidy is structured and limited, the fiscal cost would be about $100 billion over four years, based on the plan’s aim of reaching 4 million first-time homebuyers. Other housing credits and related subsidies specified in the FY 2025 budget would cost approximately another $100 billion over the next decade.

While the details are unclear, Harris has announced she would end taxes on tips for service and hospitality workers and work with Congress to establish guardrails on the policy. The exemption itself, and any safeguards added, would add to the complexity of the tax code overall while failing to benefit many low-income earners, given the small share of the population working in tipped occupations. We estimate that an exemption could cost around $118 billion over the 10-year budget window on a conventional basis.

Harris has proposed expanding the Section 195 deduction for business startup costs from its current level of $5,000 to $50,000. Based on past revenue estimates of similar proposals from the Joint Committee on Taxation, we estimate the change would reduce revenue by about $24.5 billion over the 10-year budget window on a conventional basis. The economic impacts are uncertain but small given the revenue impact; to the extent the policy allows more businesses to recover costs, it will boost business investment and potentially economic dynamism.

Subsidies and Price Controls Likely to Backfire

Many, but not all, of Harris’s housing policy proposals flow through the tax code. In terms of non-fiscal policy levers, the Harris plan includes regulatory streamlining to make construction easier, a crackdown on certain pricing tools in rental property management, and a new fund for public housing.

Harris’s reliance on subsidies for supply-constrained housing would be economically harmful for families, as it would boost demand and lead to higher housing prices. While some of her policies do target supply, like the expanded low-income housing tax credit and the credit for starter homes, these boutique tax breaks have not been effective historically.

Subsidies for different niches of the housing market are a poor substitute for better tax treatment of housing investment broadly. Multifamily housing construction still has not recovered to 1986 levels, as the Tax Reform Act of 1986 reduced the deductibility of investment.

Instead of reversing that poor tax treatment, the Harris package would further penalize rental housing construction by peeling back depreciation and interest deductions for certain large property investors, reducing investment incentives. These penalties would be in addition to a Biden-Harris administration proposal aimed at capping rent increases by disallowing certain deductions for depreciation.

Harris would deploy economically ruinous price controls in several other ways. Harris would cap the cost of insulin at $35 and out-of-pocket expenses for prescription drugs at $2,000 for all households, accelerate the speed of Medicare negotiations for prescription drug prices as part of the Inflation Reduction Act, and ban certain price increases for food and groceries.

Price controls harm consumers by reducing incentives to produce price-controlled goods. For example, the price controls on prescription drugs are likely deterring new drug development, resulting in up to 135 fewer drugs brought to market through 2039. Harris’s proposed price controls for groceries poorly address a problem that does not exist, as grocery profit margins are much lower than average across industries.

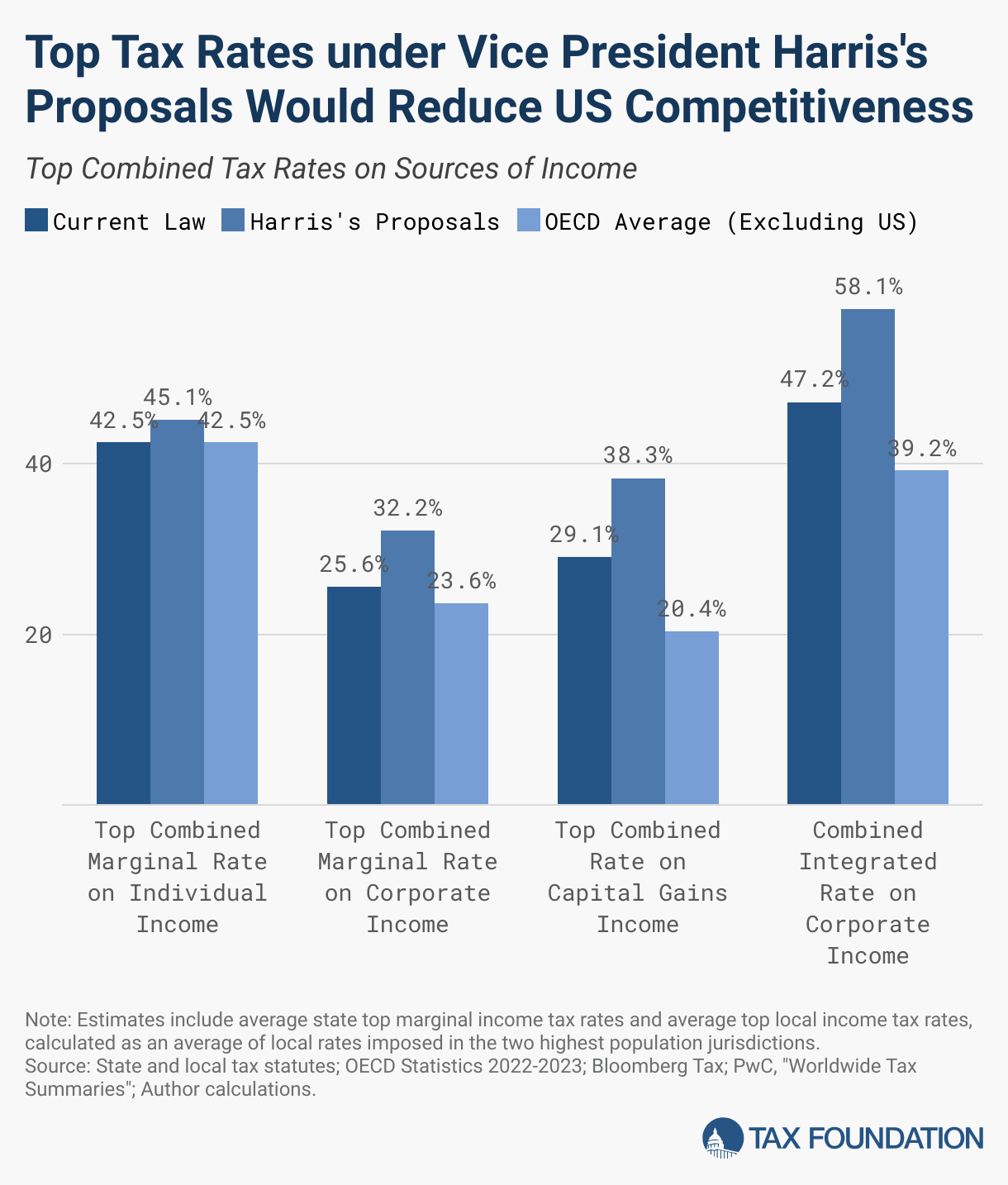

Top Tax Rates Would Be among the Highest in the Developed World

Harris’s subsidies would largely be funded by raising top tax rates on corporate and individual income to levels far above international norms.

The current top combined corporate tax rate—including the average of state rates—is 25.6 percent. Harris would increase it to 32.2 percent, the second-highest corporate tax rate in the OECD (behind Colombia’s 35 percent).

The current top combined personal tax rate is 42.5 percent, consisting of the top federal rate (37 percent) and the average of state and local rates. This is about equal to the OECD average. Under Harris, the top combined rate would rise to 45.1 percent before accounting for the proposed 5 percent additional Medicare tax, half of which falls on the employer. Including the employee-side portion would raise the top rate to 47.6 percent.

The current top combined capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment.

rate is 29.1 percent, consisting of the 20 percent capital gains tax rate, the 3.8 percent NIIT, and the average of state and local income tax rates on capital gains. By taxing high earners’ capital gains at 28 percent and raising the NIIT to 5 percent, Harris’s proposals would raise the top tax rate on capital gains to 38.3 percent—the second highest in the OECD (behind Denmark’s 42 percent). Similarly, under Harris’s proposals, the top tax rate on dividends would be nearly the highest in the OECD.

The combined integrated rate on corporate income reflects the two layers of tax corporate income faces: first at the entity level through corporate taxes and again at the shareholder level through capital gains and dividends taxes. Currently, the top combined integrated tax rate on corporate income distributed as capital gains is 47.2 percent. Under Harris’s proposals, it would rise to 58.1 percent—the highest in the OECD.

By placing a higher burden on work, saving, and investment, the Harris tax plan would reduce competitiveness and weaken key drivers of US economic growth, shrinking GDP by about 2.0 percent over the long run.

Where Do the Candidates Stand on Taxes?

Tax policy has become a significant focus of the US 2024 presidential election.

Modeling Notes

We use the Tax Foundation General Equilibrium Tax Model to estimate the impact of tax policies, including recent updates allowing detailed modeling of US multinational enterprises. The model produces conventional and dynamic revenue and distributional estimates of tax policy. Conventional estimates hold the size of the economy constant and attempt to estimate potential behavioral effects of tax policy. Dynamic revenue estimates consider both behavioral and macroeconomic effects of tax policy on revenue. The model also produces estimates of how policies impact measures of economic performance such as GDP, GNP, wages, employment, capital stock, investment, consumption, saving, and the trade deficit.

Note, however, that our conventional and dynamic estimates for the stock buyback tax do not account for behavioral shifting from buybacks to dividends, which would also shift the individual income tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

from capital gains to dividends.

Regarding Vice President Harris’s proposed changes to the GILTI regime, we modeled most of the major changes, including the 75 percent GILTI inclusion rate, country-by-country application, the reduction in the foreign tax credit (FTC) haircut to 5 percent, elimination of the qualified business asset investment (QBAI) exemption, and elimination of the foreign oil and gas extraction income (FOGEI) exclusion. We did not model the changes allowing carryforward of GILTI foreign tax credits (FTCs) and losses, repeal of the high-tax exemption for subpart F, or the tax increases on dual capacity taxpayers.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share