issues and explore the world through the lens of tax policy. Learn more about taxes with TaxEDU.

World War II shaped many aspects of the modern world, including the US tax code. But the dramatic changes to our system that military mobilization required didn’t subside when the fighting finished; they’ve persisted to today.

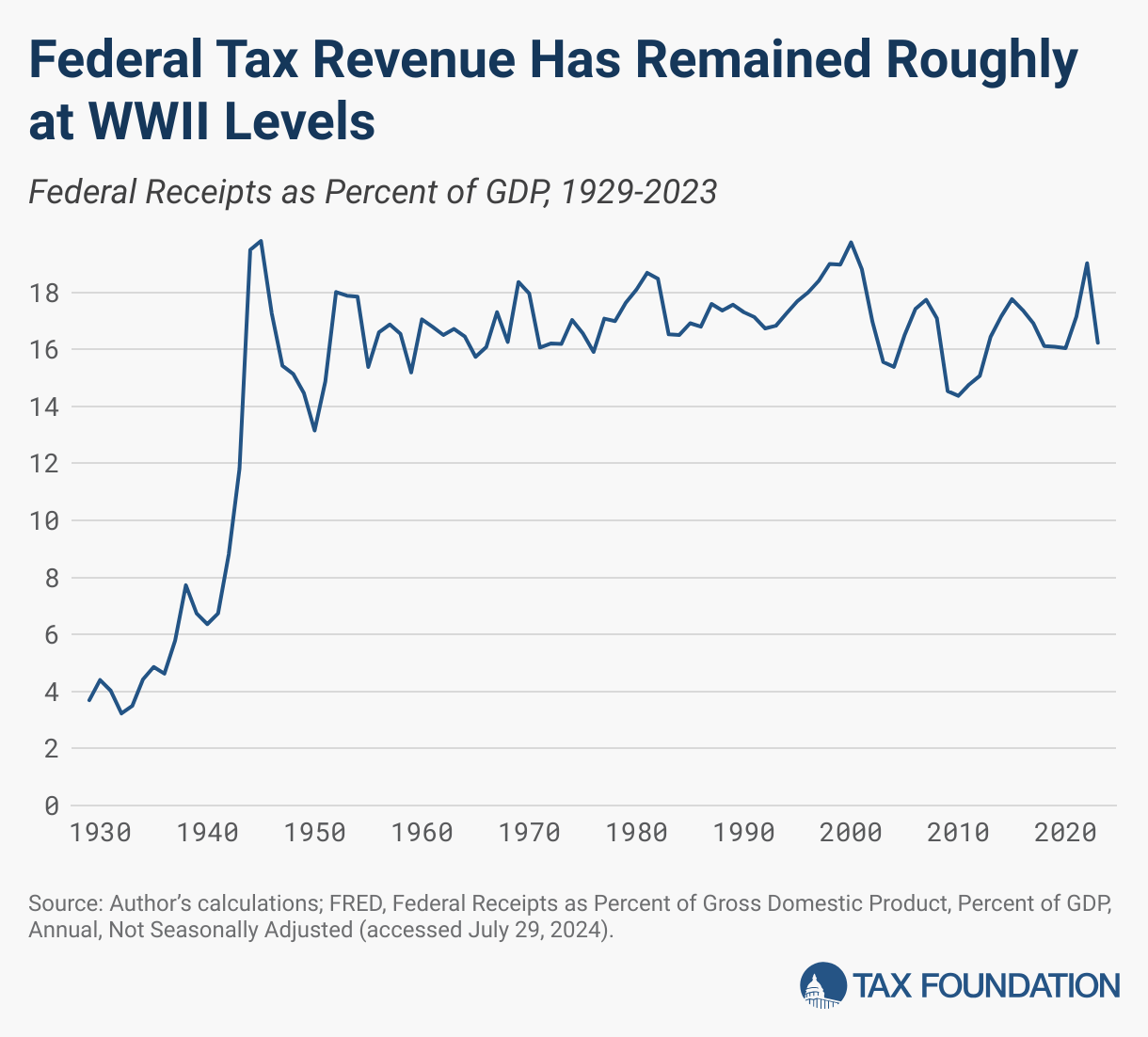

WWII Changed How Much Revenue We Raise

World War II changed how much tax revenue we collect. Before 1941, the US federal government rarely collected more than 5 percent of GDP in tax revenue. Even during the height of US participation in World War I, federal receipts (how much the government takes in) did not exceed 10 percent of national income. In fact, before US entrance into World War II, state and local governments raised more revenue than the federal government.

US entry into the war prompted a dramatic increase in military spending, which needed to be at least partly paid for with tax revenue. During the war, federal receipts as a share of GDP rose from 6.7 percent in 1941 to 8.8 percent in 1942, 11.8 percent in 1943, 19.5 percent in 1944, and 19.8 percent in 1945.

But here’s the kicker: over the course of the nearly 80 years since the conflict’s end, tax revenue has remained at those elevated levels. Since 1941, federal receipts dipped below 15 percent of GDP in only six years.

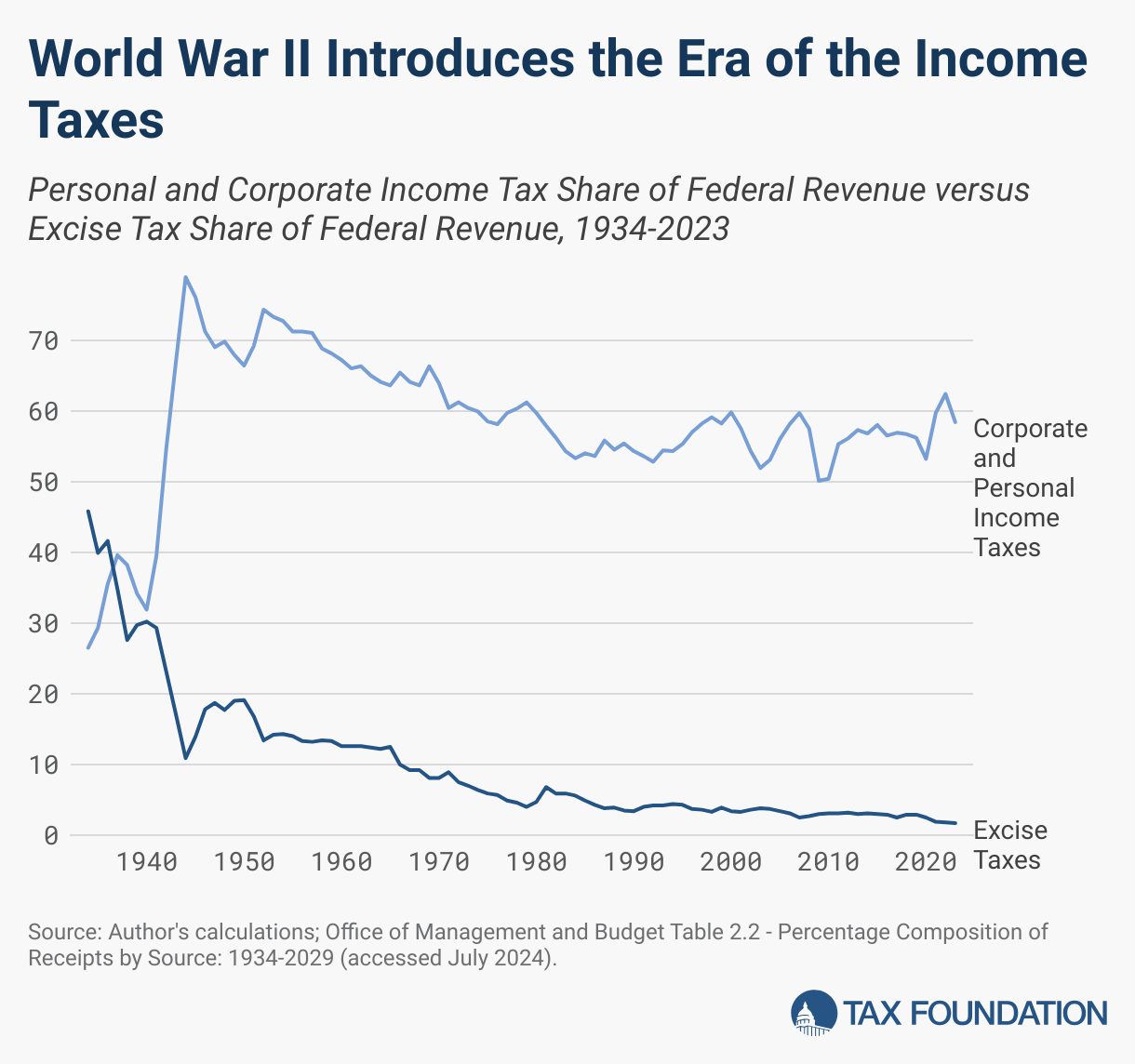

WWII Changed How We Raise Revenue

World War II also drove changes in which taxes we used to raise revenue. In the 19th century, the federal government relied heavily on tariffs (taxes on imports) to finance government services. Government spending was much lower in the 1800s, so taxes on imports could raise sufficient revenue. The personal income tax had already been introduced (first temporarily during the American Civil War, then permanently in 1913), but it was not the dominant revenue stream it is today.

Since the introduction of the income tax, tariffs had diminished dramatically as a share of revenue. They still played a significant role though: in 1937, for instance, customs duties accounted for almost 10 percent of US federal receipts, generating almost $500 million of the federal government’s $5.2 billion in revenue. Instead, the largest revenue source for the federal government pre-war was excise taxes: taxes on the production or sale of specific goods. Liquor and tobacco taxes generated the most revenue (each accounting for more than 10 percent of federal tax revenue in 1940), but excise taxes were not limited to “sin” products.

During the war, though, leaning on narrow, product-specific excise taxes or tariffs simply would not be able to raise the kind of revenue the government needed for the war effort. And as Congress rejected the idea of a national sales taxA sales tax is levied on retail sales of goods and services and, ideally, should apply to all final consumption with few exemptions. Many governments exempt goods like groceries; base broadening, such as including groceries, could keep rates lower. A sales tax should exempt business-to-business transactions which, when taxed, cause tax pyramiding.

in 1942, higher income taxes it was.

As tax historian Joseph Thorndike has put it, the income tax went from a “class tax to a mass tax”: not only did the tax rates rise, but the exemptions were also dramatically lowered, increasing the number of income taxpayers. Notably, the federal government also introduced the concept of income tax withholding, shifting the responsibility of regularly sending income tax payments to the IRS away from employees onto employers instead.

WWII Changed Investment Incentives

Now these big-picture changes to taxation seem to all move in one direction: toward higher taxes. Given the need for revenue to fund a massive military buildup, that is unsurprising. However, some wartime tax reforms reduced taxes to incentivize investment in a little-known chapter of the Second World War.

In 1940, President Franklin Delano Roosevelt appointed William “Bill” Knudsen, then president of General Motors (his predecessor, Alfred P. Sloan, had moved on to become chairman of the GM board and, among other things, the founder of Tax Foundation) to lead the process of rearming and reinvesting in military hardware. One of Knudsen’s initial priorities was shorter amortization periods for defense investment. In short, his policy idea would allow businesses to take deductions sooner for building factories or installing equipment.

After 1940 (and particularly after America’s full entry into the war in December 1941), the importance of accelerated deductions waned compared to massive direct support for defense investment in the form of government contracts for planes, ships, and all other manner of war material. Nevertheless, faster deductions helped lay the foundations for America’s role as the Arsenal of Democracy.

They also helped lay the foundation for a broader tax policy debate. When people think about tax policy, they often think about the tax rate. But the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

, namely the amount of income actually subject to tax, is just as important. And the move toward accelerated depreciation specifically related to the war effort in 1940 set the stage for a broader debate over how companies should be able to deduct their investment costs that has continued through to the present day.

Confused? Boost Your Tax Knowledge with TaxEDU

Tax policy can be complex. Thankfully our resources for understanding them aren’t.

Share