This week’s taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

map will consider the effects of an alternative form of corporate taxation, known as the gross receipt tax (GRT). States with this harmful tax can and should move away from it by adopting a well-structured low-rate, broad-based corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

or adjusting their existing corporate income tax to account for the lost revenue associated with repealing their gross receipt tax.

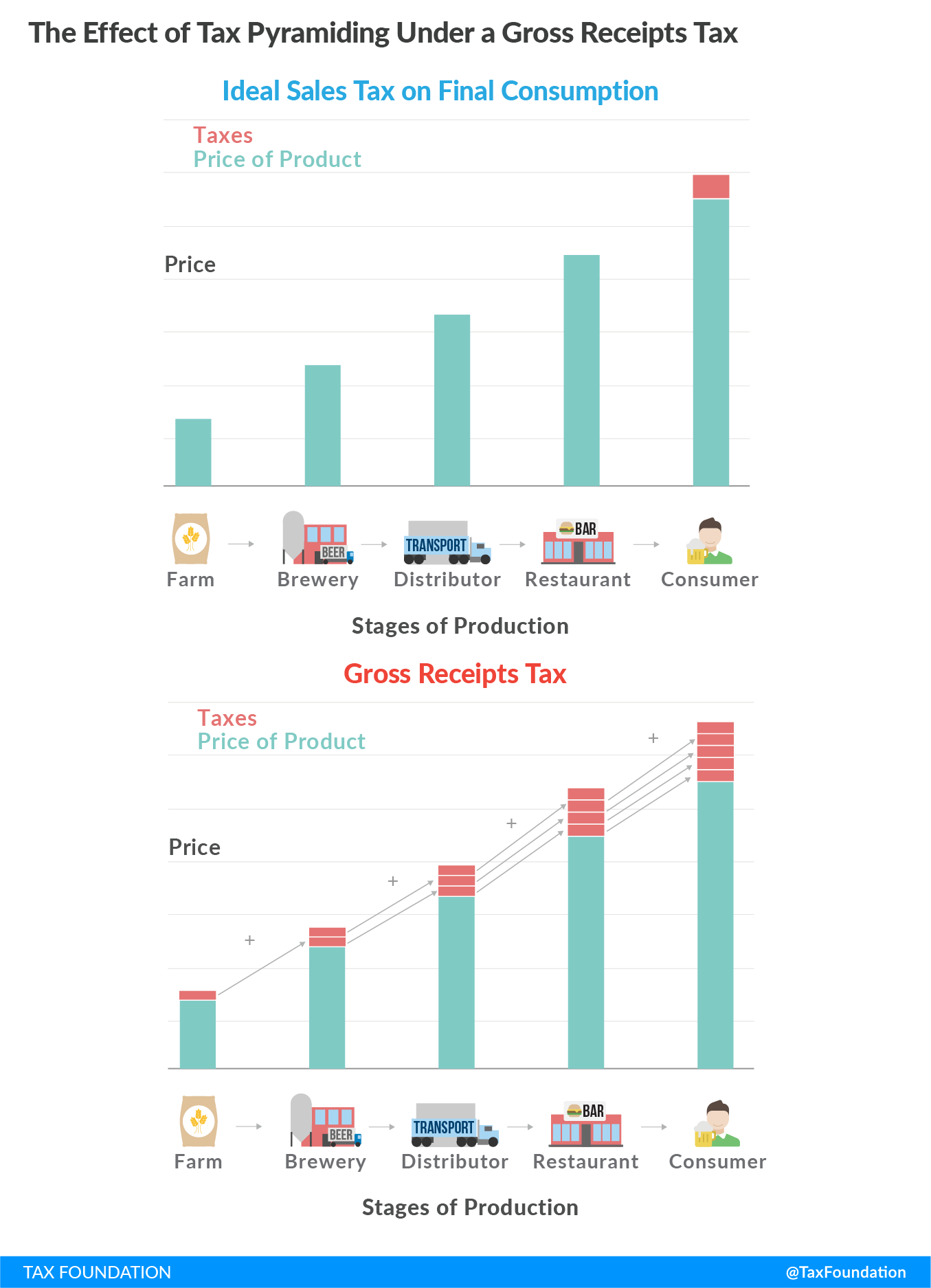

Gross receipt taxes are assessed against firms’ gross sales in a particular state prior to adjusting for firms operating costs, including compensation, dividends, materials costs, and other costs of doing business. However, some states allow for partial offsets to their gross receipt tax liability based on a variety of factors including credits, deductions, and exclusions of certain qualifying business expenditures.

Gross receipt taxes are imposed along every step in the production process, which increases businesses’ tax burden through a harmful process known as tax pyramidingTax pyramiding occurs when the same final good or service is taxed multiple times along the production process. This yields vastly different effective tax rates depending on the length of the supply chain and disproportionately harms low-margin firms. Gross receipts taxes are a prime example of tax pyramiding in action.

.

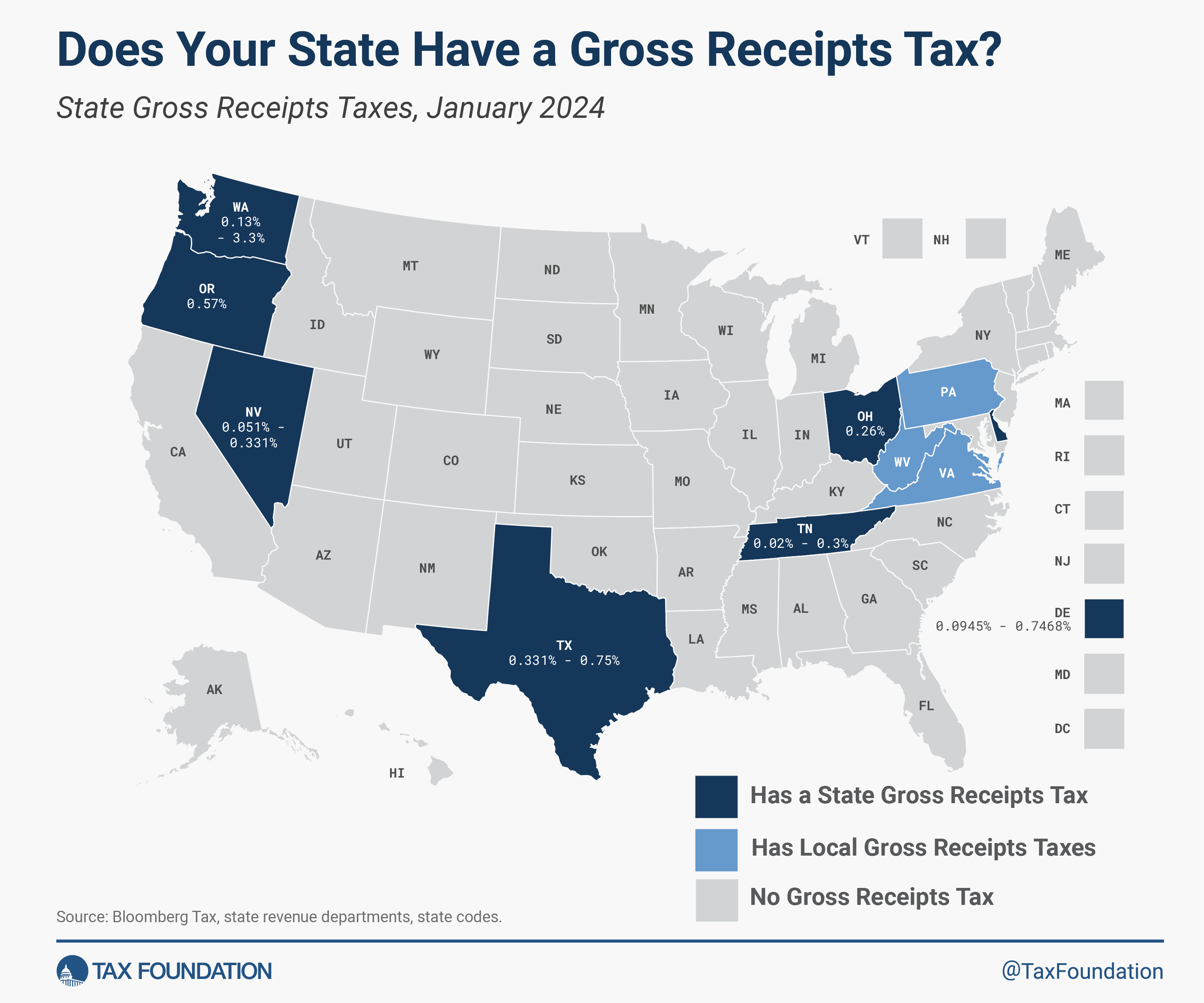

Seven states currently have a state-level gross receipts taxA gross receipts tax, also known as a turnover tax, is applied to a company’s gross sales, without deductions for a firm’s business expenses, like costs of goods sold and compensation. Unlike a sales tax, a gross receipts tax is assessed on businesses and apply to business-to-business transactions in addition to final consumer purchases, leading to tax pyramiding.

: Delaware, Nevada, Ohio, Oregon, Tennessee, Texas, and Washington. Three more states—Pennsylvania, Virginia, and West Virginia—allow municipalities to assess gross receipt taxes at the local level, but do not assess gross receipts taxes at the state level. To count under our definition of gross receipt taxes, they must be imposed against a wide enough swath of businesses to act like an alternative corporate income tax. Many states impose pro forma gross receipts taxes against mineral extraction services and other select industries that more closely resemble severance or excise taxes. We exclude those states’ gross receipt taxes in this analysis. We also omit certain broad-based sales taxes like those in New Mexico or Hawaii that straddle the line between sales and gross receipts taxes but are ultimately better categorized as poorly designed sales taxes.

Gross receipt taxes are an old idea. They were adopted in France and Spain starting in 1292 and 1342, respectively, and showed up in other medieval economies as well. The peak period of gross receipts taxation in the United States came during the Great Depression, as states sought to regain lost revenue because of decreased economic activity and anemic tax bases.

In recent decades, gross receipts taxes have fallen out of favor, and they were long ago eliminated from most states’ tax toolkits. Of those that survived into, or were adopted during, the 21st century, four have since been repealed, with Indiana, New Jersey, Kentucky, and Michigan eliminating their GRTs between 2002 and 2011. Policymakers increasingly recognized that these taxes were structurally unsound, distorted firms’ incentive to reinvest in their business models, and eliminated the profits of businesses with already narrow profit margins. Modern research aligns with the experience of taxpayers of old. In the Old World, gross receipt taxes were regarded as “iniquitous in their collection, unjust in their burdens, and unpopular with taxpayers.”

States often differentiate their gross receipt tax rates based on the type of industry or the level of gross receipts earned by the firm. Gross receipts taxes are typically assessed prior to any deductions or exclusions of the cost of goods sold or compensation to employees or shareholders. However, this is not always the case since multiple states with gross receipt taxes allow firms to exclude portions of their gross receipts from the tax baseThe tax base is the total amount of income, property, assets, consumption, transactions, or other economic activity subject to taxation by a tax authority. A narrow tax base is non-neutral and inefficient. A broad tax base reduces tax administration costs and allows more revenue to be raised at lower rates.

, or apply credits, deductions, or exclusions. These carveouts provide both benefits and trade-offs. Offering a deduction for some or all of the taxpayer’s choice of compensation or the cost of goods sold, for instance, moves the tax modestly closer to being imposed on a net income tax base, which is good, but it does so at further expense to tax neutrality, as taxpayers may find themselves taxed on labor but not capital investment, or vice versa, with all the distortions this entails.

Tennessee has the lowest gross receipts tax rate at 0.02 percent, while Washington’s Business and Occupation (B&O) Tax is imposed at rates as high as 3.3 percent, with major classifications facing rates of 0.471 percent for retailing, 0.484 percent for wholesaling and manufacturing, and 1.5 to 1.75 percent for most services.

Nevada’s Commerce Tax is a prime example of a state with a poorly structured and legally tenuous gross receipts tax. Nevada allows businesses to exempt the first $4 million of gross revenue, thus eliminating many small and medium-sized businesses in Nevada from the Commerce Tax altogether. But for businesses still subject to the tax, there’s a troublesome structural problem. In addition to the Commerce Tax, Nevada also imposes a payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue.

, known as the Modified Business Tax, and connects the two taxes through a credit that “favors companies with in-state payroll.” Businesses with a majority of their payroll located in Nevada can eliminate up to 50 percent of their Commerce Tax liability through the credit against the Nevada Modified Business Tax. Legal experts term this sort of tax a “tandem tax.” The courts have ruled similar tandem taxes unconstitutional since they violate the internal consistency test of the Commerce Clause of the United States Constitution. The internal consistency test simply determines whether a particular tax is constitutional by determining whether “interstate commerce would be burdened if every state imposed the same tax law” as Nevada in this case.

The Washington Court of Appeals also recently handed down a decision that expands the reach of the Washington Business and Occupations (B&O) tax to investment income that is not incidental to the main purpose of a business. This policy taxes earnings based on the flow of capital into and out of a business. Thus, it more closely resembles a capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment.

and tries to have it both ways regarding methods of taxing business activity, taxing gross receipts and non-receipt income. It also penalizes business investment. This is especially harmful since it will broaden the base of the Washington B&O tax while not making concurrent reductions to the rate in an effort to offset, reduce, or eliminate the Washington B&O tax.

In Oregon, the state senate has proposed increasing the exclusion for its gross receipts tax, the Commercial Activity Tax (CAT) from $1 million to $5 million. According to the NFIB, this would exempt more than 70 percent of the businesses currently subject to the tax. Given the compliance costs of the tax and the way that tax pyramiding can be more of an issue for smaller businesses (which are less vertically integrated, meaning that they do less in-house and have more points of exposure to a GRT), it addresses one concern while potentially further solidifying the continuance of a harmful tax. Exemptions and filing thresholds have their place, but policymakers should also explore lowering the overall rate or even seeking to phase the tax out altogether.

Finally, Ohio recently amended its Commercial Activity Tax in a similar manner to that of Oregon. As of January 1, 2024, Ohio eliminated the alternative minimum CAT payment and adopted a phased increase of its exclusion amount from its prior $1 million in tax year 2023 to $3 million in tax year 2024, capped at $6 million in tax year 2025. Again, this is generally welcome news, as the tax is highly burdensome to many small businesses. At the same time, these changes make it difficult for Ohio legislators to address the harmful economic and business investment effects of the Ohio CAT as it applies to businesses still subject to the tax. In Ohio, however, the CAT was a replacement for three different business taxes—the corporate income tax, the business tangible personal property taxA property tax is primarily levied on immovable property like land and buildings, as well as on tangible personal property that is movable, like vehicles and equipment. Property taxes are the single largest source of state and local revenue in the U.S. and help fund schools, roads, police, and other services.

, and a capital stock tax—and represented a substantial net tax reduction when adopted, so the business community, while cognizant of the economically harmful design of the tax, has demonstrated mixed feelings about it. For many businesses, better a low-rate, low-collection tax, however inefficiently designed, than a more neutral, but also more aggressive, tax. Of course, these are not Ohio’s only options, and there remain better alternatives to the CAT which policymakers shouldn’t ignore.

Gross receipt taxes are harmful to businesses’ investment decisions and are opposed by the middle class due to their perverse economic outcomes. They can and should be left in the dustbin of history. If states intend to levy a broad-based business tax, a properly corporate income tax that allows businesses to deduct the cost of goods sold, as well as qualifying business investments and inputs, is—while far from an ideal tax—demonstrably better than a tax on gross receipts.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Share

Previous Versions

-

Gross Receipts Taxes by State, 2023

4 min read

-

Gross Receipts Taxes by State, 2022

4 min read

-

Gross Receipts Taxes by State, 2021

3 min read

-

Gross Receipts Taxes by State, 2020

3 min read