Loss carryover provisions allow businesses to either deduct current year losses against future profits (carryforwards) or current year losses against past profits (carrybacks). Many companies have investment projects with different risk profiles and operate in industries that fluctuate greatly with the business cycle. Carryover provisions help businesses “smooth” their risk and income, making the tax code more neutral across investments and over time.

Ideally, a tax code allows businesses to carry over their losses for an unlimited number of years, ensuring that a business is taxed on its average profitability over time. While some countries do allow for indefinite loss carryovers, others have time limits. The following two maps look at this time restriction on loss carryovers, showing the number of years a business is allowed to carry forward and to carry back net operating losses.

{kind=link}

Fifteen out of the 27 European OECD countries allow businesses to carry forward their net operating losses for an unlimited number of years. Of the remaining countries, Luxembourg has the most generous limit, at 17 years, while the Czech Republic, Greece, Hungary, Poland, Slovakia, and Turkey limit their carryforwards to five years.

{kind=link}

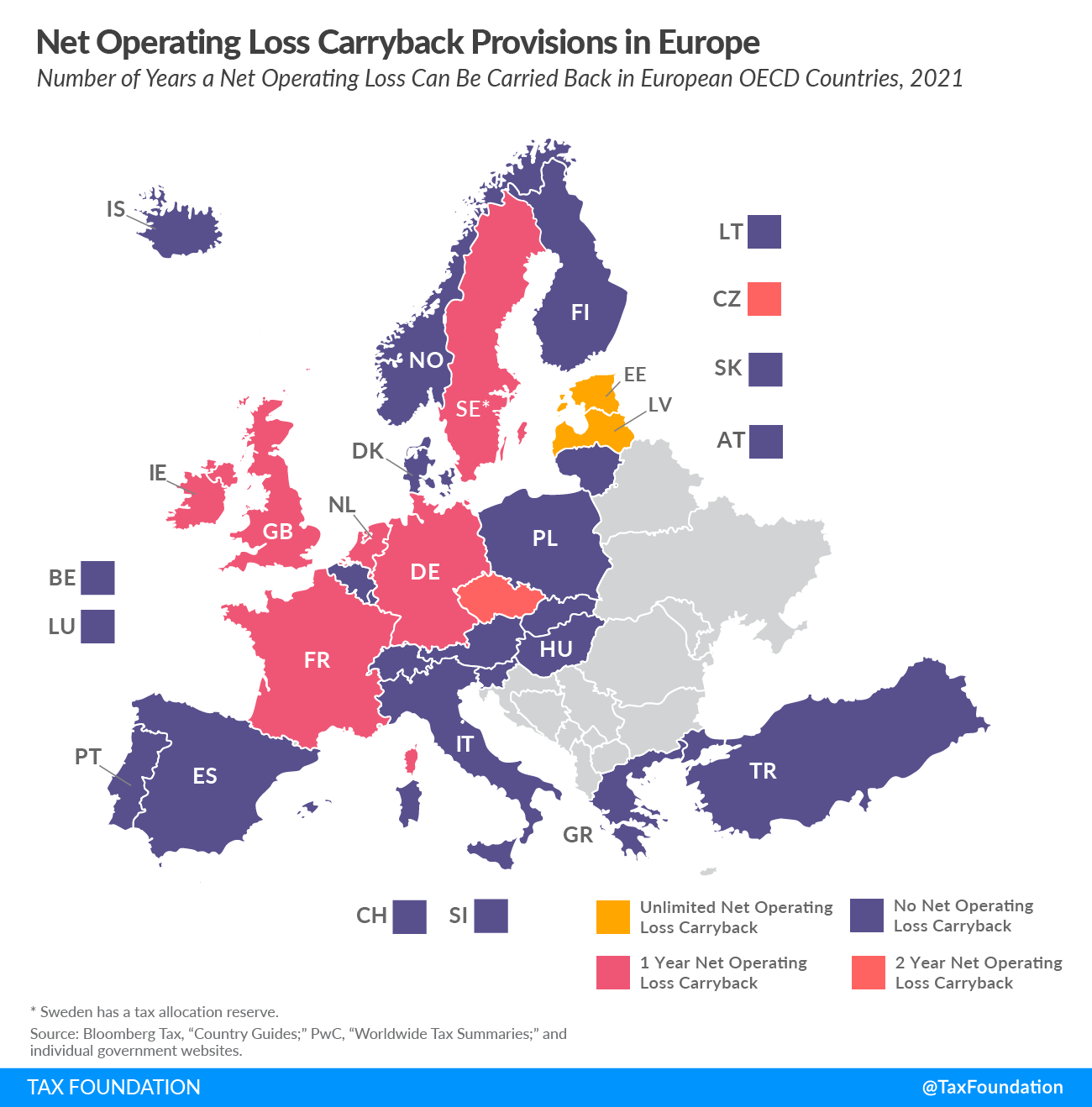

While all European OECD countries allow their businesses to carry forward losses, they tend to be much more restrictive with carryback provisions. Of the nine countries that allow carrybacks, only Estonia and Latvia provide them without a time limit.

It is worth noting that Estonia and Latvia do not explicitly allow for indefinite loss carryovers. Both of their corporate tax systems utilize a so-called “cash-flow tax.” This tax is only levied when a business distributes its profits to its shareholders, making calculating the annual taxable profits—including potential loss deductions—redundant. Compared to a traditional corporate tax system, such a cash-flow tax effectively allows for indefinite loss carryovers.

In addition to year limits, several countries impose deductibility limits. For example, Italy’s loss deduction can only be applied to 80 percent of taxable income.

Finally, in response to the economic effects of COVID-19, a number of countries have implemented temporary loss carryback provisions or increased their deductibility limits. For example, Germany has increased its loss carryback amount from €1 million to €10 million for fiscal years 2020 and 2021.

Was this page helpful to you?

Thank You!

The Tax Foundation works hard to provide insightful tax policy analysis. Our work depends on support from members of the public like you. Would you consider contributing to our work?

Contribute to the Tax Foundation

Share This Article!

Let us know how we can better serve you!

We work hard to make our analysis as useful as possible. Would you consider telling us more about how we can do better?