Over the last few years, concerns have been raised that the existing international tax system does not properly capture the digitalization of the economy. Under current international tax rules, multinationals generally pay corporate income tax where production occurs rather than where consumers or, specifically for the digital sector, users are located. However, some argue that through the digital economy, businesses (implicitly) derive income from users abroad but, without a physical presence, are not subject to corporate income tax in that foreign country.

To address these concerns, the Organisation for Economic Co-operation and Development (OECD) has been hosting negotiations with more than 130 countries to adapt the international tax system. The current proposal would require multinational businesses to pay some of their income taxes where their consumers or users are located. According to the OECD, an agreement is expected midyear.

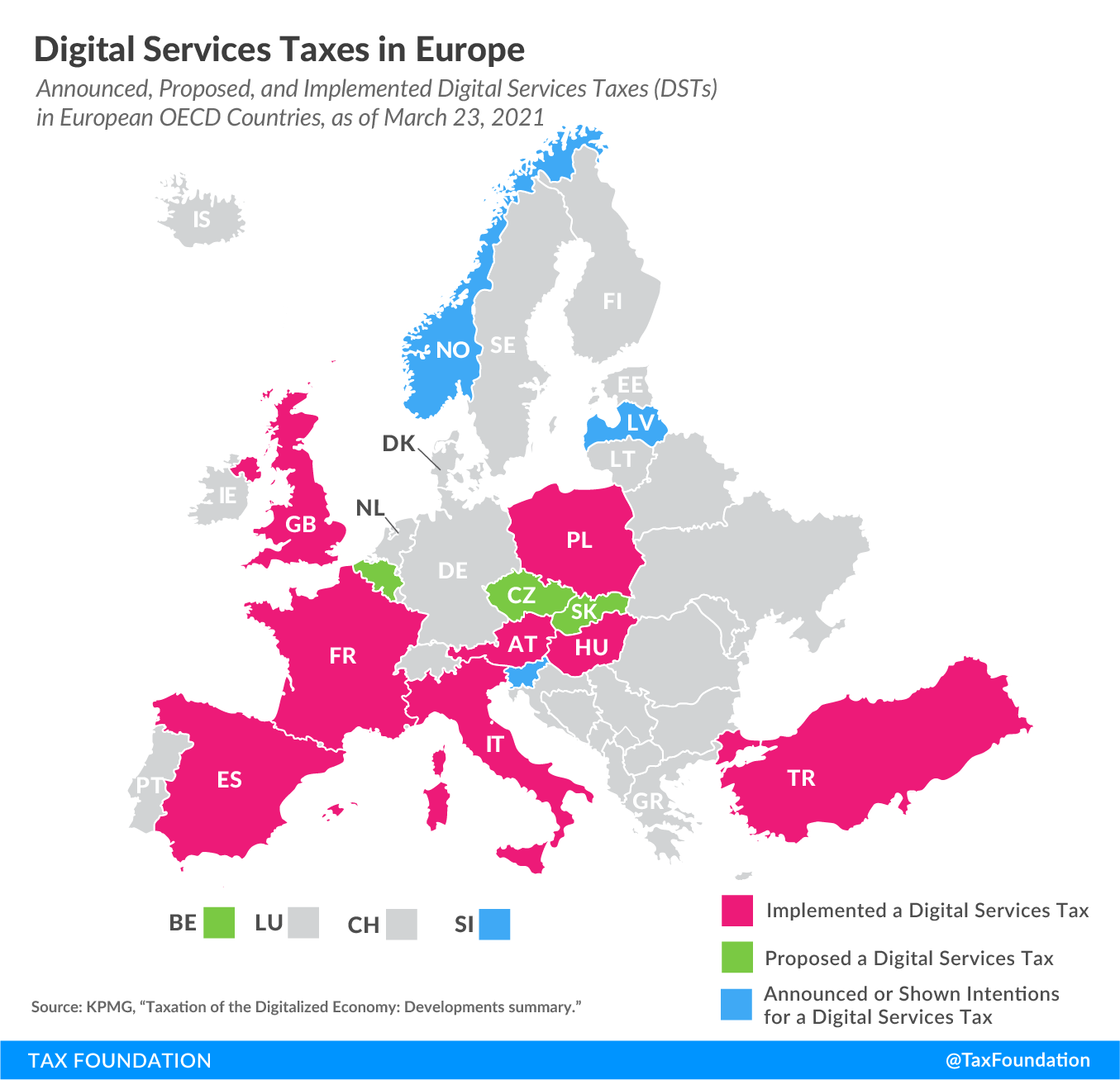

However, despite these ongoing multilateral negotiations, several countries have decided to move ahead with unilateral measures to tax the digital economy. About half of all European OECD countries have either announced, proposed, or implemented a digital services tax (DST), which is a tax on selected gross revenue streams of large digital companies. Because these taxes mainly impact U.S. companies and are thus perceived as discriminatory, the United States has responded with retaliatory threats.

{kind=link}

As of Tuesday, Austria, France, Hungary, Italy, Poland, Spain, Turkey, and the United Kingdom have implemented a DST. Belgium, the Czech Republic, and Slovakia have published proposals to enact a DST, and Latvia, Norway, and Slovenia have either officially announced or shown intentions to implement such a tax.

The proposed and implemented DSTs differ significantly in their structure. For example, while Austria and Hungary only tax revenues from online advertising, France’s tax base is much broader, including revenues from the provision of a digital interface, targeted advertising, and the transmission of data collected about users for advertising purposes. The tax rates range from 1.5 percent in Poland to 7.5 percent in both Hungary and Turkey (although Hungary’s tax rate is temporarily reduced to 0 percent).

Although these DSTs are generally considered to be interim measures until an agreement is reached at the OECD level, it is unclear whether all will be repealed at that point. In addition, the European Union (EU) intends to implement its own digital levy from 2023 onwards, with a bill outlining the details expected midyear. At the same time, the United Nations (UN) is considering adding special provisions for income from automated digital services to the UN Model Tax Convention (see Article 12B), which would apply to treaty parties who agree to its inclusion.

| Country | Tax Rate | Scope | Global Revenue Threshold | Domestic Revenue Threshold | Status |

|---|---|---|---|---|---|

| Austria (AT) | 5% | Online advertising | €750 million (US $840 million) | €25 million ($28 million) | Implemented (Effective from January 2020) |

| Belgium (BE) | 3% | Selling of user data | €750 million ($840 million) | €5 million ($5.6 million) | Proposed (A DST was first introduced in January 2019 but was rejected in March 2019; an adjusted DST proposal was reintroduced in June 2020; however, the new government, sworn in October 1, 2020, has announced it will wait for a global solution) |

| Czech Republic (CZ) | 5% | · Targeted advertising · Use of multilateral digital interfaces · Provision of user data (additional thresholds apply) |

€750 million ($840 million) | CZK 100 million ($4 million) | Proposed (Discussions delayed due to COVID-19 pandemic; there is a proposed amendment that reduces the tax rate from 7% to 5%) |

| France (FR) | 3% | · Provision of a digital interface · Advertising services based on users’ data |

€750 million ($840 million) | €25 million ($28 million) | Implemented (Retroactively applicable as of January 1, 2019) |

| Hungary (HU) | 7.5% | Advertising revenue | HUF 100 million ($344,000)) | N/A | Implemented (As a temporary measure, the advertisement tax rate has been reduced to 0%, effective from July 1, 2019 through December 31, 2022) |

| Italy (IT) | 3% | · Advertising on a digital interface · Multilateral digital interface that allows users to buy/sell goods and services · Transmission of user data generated from using a digital interface |

€750 million ($840 million) | €5.5 million ($6 million) | Implemented (Effective from January 2020) |

| Latvia (LV) | 3% | – | – | – | Announced/Shows Intentions (The Latvian government commissioned a study to determine the increase of tax revenue based on the assumption that the country levies a 3% DST) |

| Norway (NO) | – | – | – | – | Announced/Shows Intentions (Plans to introduce a unilateral measure in 2021 if the OECD does not reach a consensus solution in 2020) |

| Poland (PL) | 1.5% | Audiovisual media service and audiovisual commercial communication | – | – | Implemented (Effective from July 2020; there is a separate proposal to tax advertisement revenues of broadcasters, tech companies, and publishers) |

| Slovakia (SK) | – | – | – | – | Proposed (The Ministry of Finance opened a consultation on a proposal to introduce a DST on revenue of nonresidents from provision of services such as advertising, online platforms, and sale of user data; however, there were no further steps taken and none of the political parties has put forward digital tax as its priority agenda) |

| Slovenia (SI) | – | – | – | – | Announced/Shows Intentions (The Ministry of Finance announced a government proposal to submit a draft bill to the National Assembly introducing a digital services tax by April 1, 2020; however, there has been no development so far) |

| Spain (ES) | 3% | · Online advertising services · Sale of online advertising · Sale of user data |

€750 million ($840 million) | €3 million ($3 million) | Implemented (Effective from January 2021) |

| Turkey (TR) | 7.5% | Online services including advertisements, sales of content, and paid services on social media websites | €750 million ($840 million) | TRY 20 million ($4 million) | Implemented (Effective from March 2020; the president can reduce the DST rate as low as 1% or increase it as much as 15%) |

| United Kingdom (GB) | 2% | · Social media platforms · Internet search engine · Online marketplace |

£500 million ($638 million) | £25 million ($32 million) | Implemented (Retroactively applicable as of April 1, 2020) |

|

Sources: KPMG, “Taxation of the digitalized economy: Developments summary,” Jan. 15, 2021, https://tax.kpmg.us/content/dam/tax/en/pdfs/2020/digitalized-economy-taxation-developments-summary.pdf; and Bloomberg Tax, “Poland’s Government Plans to Approve New Ad Tax Bill in 1Q,” Feb. 2, 2021, https://www.news.bloombergtax.com/daily-tax-report/polands-government-plans-to-approve-new-ad-tax-bill-in-1q. |

|||||

Was this page helpful to you?

Thank You!

The Tax Foundation works hard to provide insightful tax policy analysis. Our work depends on support from members of the public like you. Would you consider contributing to our work?

Contribute to the Tax Foundation

Share This Article!

Let us know how we can better serve you!

We work hard to make our analysis as useful as possible. Would you consider telling us more about how we can do better?