Key Findings

-

In calendar year 2019 (the latest economic data), state-local tax burdens averaged 10.3 percent of national income. Burdens rose slightly over the previous year because tax collections modestly exceeded income growth.

-

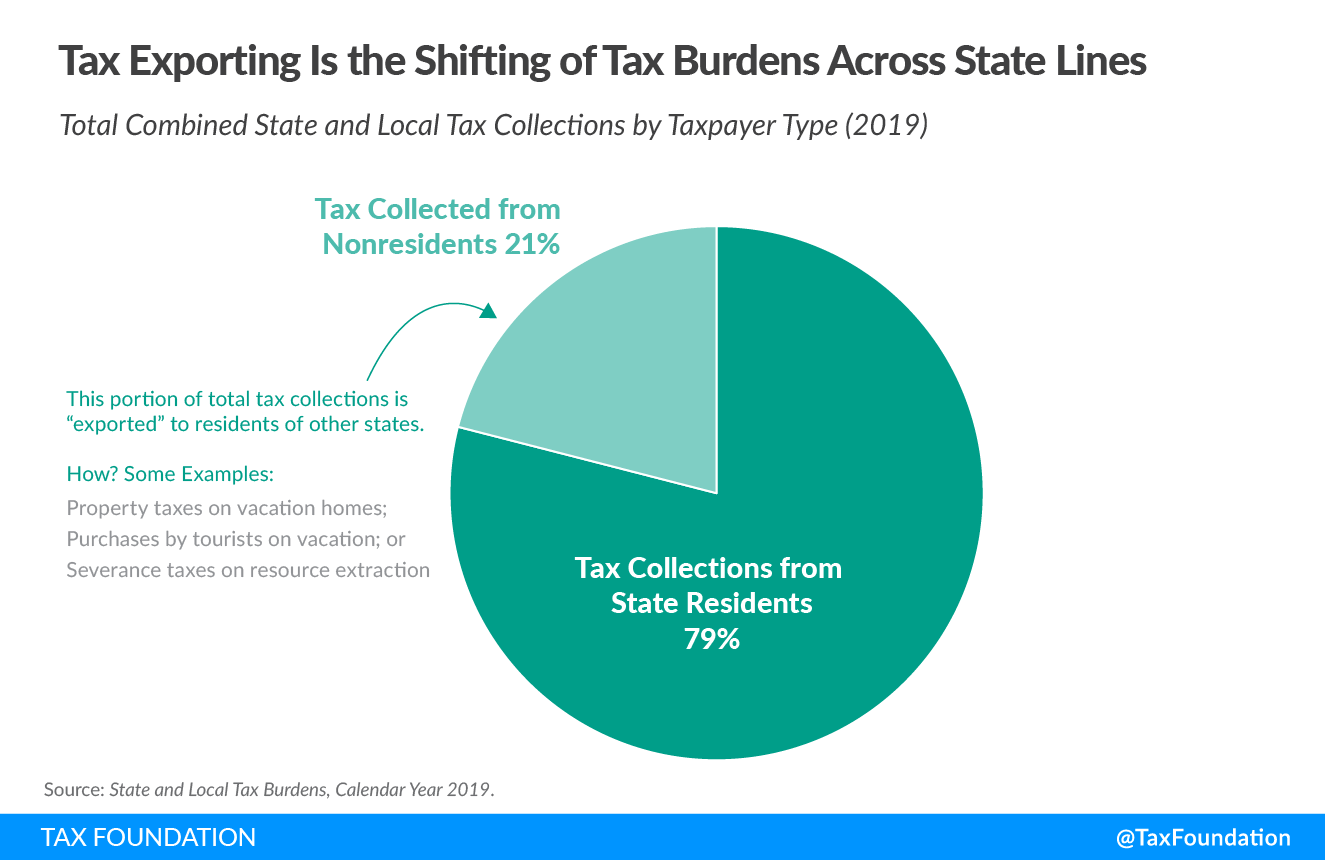

Taxpayers remit taxes to their home state and to other states, and about 21 percent of state tax revenue comes from nonresidents. Our tax burdens analysis accounts for this tax exporting.

-

New Yorkers faced the highest burden, with 14.1 percent of income in the state going to state and local taxes. Connecticut (12.8 percent) and Hawaii (12.7 percent) followed.

-

On the other end of the spectrum, Alaska (5.8 percent), Wyoming (7.0 percent), and Tennessee (7.0 percent) had the lowest burdens.

-

State-local tax burdens are often very close to one another and slight changes in taxes or income can translate to seemingly dramatic shifts in rank. For example, Delaware (16th) and Missouri (35th) differ in burden by just over one percentage point. However, while burdens are clustered in the center of the distribution, states at the top and bottom can have substantially different burden percentages.

{kind=link}

| State-Local Effective Tax Rate | Rank | |

|---|---|---|

| Alabama | 9.0% | 38 |

| Alaska | 5.8% | 50 |

| Arizona | 8.7% | 45 |

| Arkansas | 10.4% | 17 |

| California | 11.5% | 8 |

| Colorado | 9.4% | 34 |

| Connecticut | 12.8% | 2 |

| Delaware | 10.3% | 18 |

| District of Columbia | 10.1% | (22) |

| Florida | 8.8% | 43 |

| Georgia | 8.9% | 41 |

| Hawaii | 12.7% | 3 |

| Idaho | 9.6% | 31 |

| Illinois | 11.1% | 10 |

| Indiana | 8.9% | 39 |

| Iowa | 10.8% | 13 |

| Kansas | 10.1% | 22 |

| Kentucky | 9.9% | 25 |

| Louisiana | 9.2% | 36 |

| Maine | 11.0% | 12 |

| Maryland | 11.8% | 6 |

| Massachusetts | 10.5% | 15 |

| Michigan | 10.0% | 23 |

| Minnesota | 12.1% | 5 |

| Mississippi | 9.5% | 33 |

| Missouri | 9.2% | 35 |

| Montana | 10.1% | 21 |

| Nebraska | 10.3% | 19 |

| Nevada | 9.7% | 29 |

| New Hampshire | 9.7% | 28 |

| New Jersey | 11.7% | 7 |

| New Mexico | 8.8% | 44 |

| New York | 14.1% | 1 |

| North Carolina | 9.5% | 32 |

| North Dakota | 8.9% | 42 |

| Ohio | 10.3% | 20 |

| Oklahoma | 8.2% | 46 |

| Oregon | 11.1% | 11 |

| Pennsylvania | 10.4% | 16 |

| Rhode Island | 11.4% | 9 |

| South Carolina | 8.9% | 40 |

| South Dakota | 9.1% | 37 |

| Tennessee | 7.0% | 48 |

| Texas | 8.0% | 47 |

| Utah | 9.6% | 30 |

| Vermont | 12.3% | 4 |

| Virginia | 10.0% | 24 |

| Washington | 9.8% | 27 |

| West Virginia | 9.9% | 26 |

| Wisconsin | 10.7% | 14 |

| Wyoming | 7.0% | 49 |

What Are Tax Burdens?

In this study, we define a state’s tax burden as state and local taxes paid by a state’s residents divided by that state’s share of net national product.[1] This study’s contribution to our understanding of true tax burdens is its focus on the fact that each of us not only pays state and local taxes to our own places of residence, but also to the governments of states and localities in which we do not live.

Tax shifting across state borders arises from several factors, including our movement across state lines during work and leisure time and the interconnectedness of the national economy. The largest driver of this phenomenon, however, is the reality that the ultimate incidence of a tax frequently falls on entities other than those that write the check to the government. For instance, shareholders and employees both shoulder some of the burden of corporate income taxes, even though they are remitted by the company itself. Similarly, renters ultimately bear much of the cost of property taxes on their rental unit, even though their landlord receives the tax bill.

What Is Tax Incidence?

The incidence of a tax is a measure of which entity pays the tax. But there are two very different types of tax incidence: legal incidence and economic incidence.

The legal incidence of taxes is borne by those with the legal obligation to remit tax payments to state and local governments. Legal incidence is established by law and tells us which individuals or companies must physically send tax payments to state and local treasuries.

The legal incidence of taxes is generally very different from the final economic burden. Because taxes influence the relative prices facing individuals, they lead to changes in individual behavior. Tax-induced changes in behavior cause some portion (or all) of the economic burden of taxes to be shifted from those bearing the legal incidence onto others in society. For example, the legal incidence of corporate income taxes typically falls on companies. But economists agree that some portion of the tax is shifted forward to others, in the form of higher prices for consumers, lower wages for workers, reduced returns to shareholders, or some combination of the three.

Once tax-induced changes in behavior throughout the economy are accounted for, the final distribution of the economic burden of taxes is called the economic incidence. It is also referred to as the tax burden faced by individuals in their roles as consumers, workers, and investors.

What Is Tax Exporting?

Beyond the fact that tax burdens are often ultimately borne by people who do not directly remit them, taxes imposed by state and local governments are often borne—in both their legal and economic incidences—by nonresidents. When some share of the burden of a tax imposed in one state is borne by people who live elsewhere, it is known as tax exporting.

{kind=link}

Wyoming provides good examples of tax exporting. Fifty-seven percent of Wyoming’s state and local tax collections came from residents of other states in 2019. The main driver was state taxes on oil extraction (severance taxes and taxes on oil production and pipeline property).

The burden of Wyoming oil taxes does not fall predominantly on Wyoming residents. Ignoring this fact and comparing Wyoming tax collections directly to Wyoming income makes the tax burden of Wyoming residents look much higher than it actually is.

This study assumes that much of the economic burden of severance taxes falls on capital, such as oil industry investors, rather than on Wyoming taxpayers. Notably, it does not assume that the burden substantially falls on consumers (including drivers who purchase motor fuel), since prices are set by global energy markets. The same is true for states like North Dakota and Alaska where, once the adjustment is made, the aggregate tax burden falls from among the nation’s highest to the lowest. Alaska itself, while still third highest for exporting of tax burdens, has seen the amount exported fall precipitously in recent years as oil revenues have plummeted.

Resource-rich states are only some of the more extreme examples of tax exporting. Major tourist destinations like Florida and Nevada are able to tax tourists, who are most often nonresidents, in addition to exporting many tax costs to investors. Some states have large numbers of residents employed out of state who pay individual income taxes to the states in which they work. When a metropolitan area attracts workers from nearby states, a large portion of wage income in a state can be earned by border-crossing commuters. On the other hand, some states have reciprocity agreements in which they tax their own residents, regardless of where they work.

Every state’s economic activity is different, as is every state’s tax code. As a result, each varies in its ability to export its tax burden. Economists have been studying this phenomenon since at least the 1960s when public finance economist Charles McLure estimated that states were extracting between 15 and 35 percent of their tax revenue from nonresidents.[2]

Much interstate tax collecting occurs through no special effort by state and local legislators or tax collectors. Tourists spend as they travel and many of their transactions are taxed. People who own property out of state pay property taxes in those states. And the burden of business taxes is borne by the employees, shareholders, and customers of those businesses wherever they may live. In many states, however, lawmakers have made a conscious effort to levy taxes specifically on nonresidents. Common examples include tax increases on hotel rooms, rental cars, and restaurant meals, and local sales taxes in resort areas.

What Is the Difference between Tax Burdens and Tax Collections?

The distinction between tax burdens and tax collections is crucial to understanding tax shifting across state lines. Because tax collections represent a tally of tax payments made to state and local governments, they measure legal incidence only. In contrast, our tax burdens estimates allocate taxes to states that are economically affected by them. As a result, the estimates in the report attempt to measure the economic incidence of taxes, not the legal incidence.

Tax collections are useful for some purposes and cited frequently. However, dividing total taxes collected by governments in a state by the state’s total income is not an accurate measure of the tax burden on a state’s residents as a whole because it does not accurately reflect the taxes that are actually paid out of that state’s income.

The authoritative source for state and local tax collections data is the U.S. Census Bureau’s State and Local Government Finance division, which serves as the main input and starting point for our tax burdens model. Here are a few additional examples of the difference between tax collections (tallied by the Census Bureau) and our tax burdens estimates:

- When Connecticut residents work in New York City and pay income tax to both New York State and the city, the Census Bureau will count those amounts as New York tax collections, but we count them as part of the tax burden of Connecticut’s residents.

- When people all over the country vacation at Disney World or in Las Vegas, tax collectors will tally the receipts from lodging, rental car, restaurant, and general sales taxes in Florida and Nevada, but we allocate these taxes partly to labor and partially to holders of capital across the country.

- When a publicly traded company pays corporate income taxes in Minnesota, that tax burden is borne by shareholders across the country.

In addition to examples like these, our study allocates corporate taxes, individual income taxes, general sales taxes, tourism-related taxes, business property taxes, and severance taxes to out-of-state taxpayers.

Which Taxes Are Included in the Tax Burdens Estimates?

We include all taxes reported by the Census Bureau’s State and Local Government Finance division. These taxes are:

- Property taxes;

- General sales taxes;

- Excise taxes on alcoholic beverages, amusements, insurance premiums, motor fuels, pari-mutuels, public utilities, tobacco products, and other miscellaneous transactions;

- License taxes on alcoholic beverages, amusements, general corporations, hunting and fishing, motor vehicles, motor vehicle operators, public utilities, occupations and businesses not classified elsewhere, and other miscellaneous licenses;

- Individual income taxes;

- Corporate income taxes;

- Estate, inheritance, and gift taxes;

- Documentary and transfer taxes;

- Severance taxes;

- Special assessments for property improvements; and

- Miscellaneous taxes not classified in one of the above categories.

Our time unit of measure is the calendar year. Fiscal year data from states have been adjusted to match the calendar year. The state and local tax burden estimates for calendar year 2019 presented in this paper are based on the most recent data available from the Census Bureau, the Bureau of Economic Analysis, and all other data sources employed. Where data sources lag calendar year 2019, we adjust them based on the latest economic data.

Limitations

Tax burden measures are not measures of the size of government in a state, nor are they technically measures of the complete burden of taxation faced by a given state’s residents (this study excludes compliance costs and economic efficiency losses). Furthermore, the tax burden estimates presented here do not take into account the return to that taxation in the form of government spending. Such drawbacks, however, are not unique to our tax burden estimates.

It is also worth noting that our tax burden estimates are not at the individual taxpayer level. Our tax burden estimates look at the aggregate amount of state and local taxes paid, not the taxes paid by an individual. We collect data on the total income earned in a state (by all residents collectively) and estimate the share of that total that goes toward state and local taxes.

Calendar Year 2019 Results

State-local tax burdens of each of the states’ residents as a share of income are clustered quite close to one another. This is logical considering state and local governments fund similar activities such as public education, transportation, prison systems, and health programs, often under the same federal mandates. Furthermore, tax competition between states can often make dramatic differences in the level of taxation between similar nearby states unsustainable in the long run.

| State | State-Local Effective Tax Rate | Rank | State-Local Tax Burden per Capita | Taxes Paid to Own State per Capita | Taxes Paid to Other States Per Capita |

|---|---|---|---|---|---|

| Alabama | 9.0% | 38 | $3,893 | $3,025 | $867 |

| Alaska | 5.8% | 50 | $3,605 | $2,350 | $1,255 |

| Arizona | 8.7% | 45 | $3,926 | $2,974 | $951 |

| Arkansas | 10.4% | 17 | $4,581 | $3,437 | $1,143 |

| California | 11.5% | 8 | $7,529 | $6,171 | $1,359 |

| Colorado | 9.4% | 34 | $5,677 | $4,269 | $1,409 |

| Connecticut | 12.8% | 2 | $9,705 | $7,742 | $1,964 |

| Delaware | 10.3% | 18 | $5,550 | $4,210 | $1,340 |

| District of Columbia | 10.1% | (22) | $8,261 | $6,112 | $2,149 |

| Florida | 8.8% | 43 | $4,555 | $3,114 | $1,441 |

| Georgia | 8.9% | 41 | $4,221 | $3,292 | $929 |

| Hawaii | 12.7% | 3 | $7,144 | $5,873 | $1,271 |

| Idaho | 9.6% | 31 | $4,336 | $3,230 | $1,106 |

| Illinois | 11.1% | 10 | $6,450 | $5,210 | $1,240 |

| Indiana | 8.9% | 39 | $4,289 | $3,398 | $891 |

| Iowa | 10.8% | 13 | $5,499 | $4,397 | $1,102 |

| Kansas | 10.1% | 22 | $5,292 | $4,115 | $1,176 |

| Kentucky | 9.9% | 25 | $4,279 | $3,439 | $840 |

| Louisiana | 9.2% | 36 | $4,292 | $3,405 | $888 |

| Maine | 11.0% | 12 | $5,492 | $4,477 | $1,016 |

| Maryland | 11.8% | 6 | $7,539 | $5,973 | $1,566 |

| Massachusetts | 10.5% | 15 | $7,658 | $6,041 | $1,617 |

| Michigan | 10.0% | 23 | $4,841 | $3,913 | $928 |

| Minnesota | 12.1% | 5 | $7,001 | $5,782 | $1,219 |

| Mississippi | 9.5% | 33 | $3,654 | $2,975 | $680 |

| Missouri | 9.2% | 35 | $4,431 | $3,413 | $1,018 |

| Montana | 10.1% | 21 | $4,956 | $3,633 | $1,323 |

| Nebraska | 10.3% | 19 | $5,548 | $4,367 | $1,181 |

| Nevada | 9.7% | 29 | $4,895 | $3,561 | $1,334 |

| New Hampshire | 9.7% | 28 | $6,090 | $4,577 | $1,513 |

| New Jersey | 11.7% | 7 | $8,134 | $6,447 | $1,687 |

| New Mexico | 8.8% | 44 | $3,736 | $2,865 | $871 |

| New York | 14.1% | 1 | $9,987 | $8,467 | $1,520 |

| North Carolina | 9.5% | 32 | $4,490 | $3,547 | $943 |

| North Dakota | 8.9% | 42 | $4,996 | $3,634 | $1,362 |

| Ohio | 10.3% | 20 | $5,107 | $4,173 | $934 |

| Oklahoma | 8.2% | 46 | $3,841 | $2,903 | $938 |

| Oregon | 11.1% | 11 | $5,809 | $4,630 | $1,179 |

| Pennsylvania | 10.4% | 16 | $5,970 | $4,818 | $1,152 |

| Rhode Island | 11.4% | 9 | $6,334 | $4,893 | $1,441 |

| South Carolina | 8.9% | 40 | $4,000 | $3,039 | $961 |

| South Dakota | 9.1% | 37 | $4,855 | $3,464 | $1,391 |

| Tennessee | 7.0% | 48 | $3,368 | $2,578 | $790 |

| Texas | 8.0% | 47 | $4,143 | $3,259 | $884 |

| Utah | 9.6% | 30 | $4,636 | $3,491 | $1,145 |

| Vermont | 12.3% | 4 | $6,693 | $5,464 | $1,229 |

| Virginia | 10.0% | 24 | $5,854 | $4,412 | $1,442 |

| Washington | 9.8% | 27 | $6,245 | $4,687 | $1,558 |

| West Virginia | 9.9% | 26 | $4,114 | $3,242 | $873 |

| Wisconsin | 10.7% | 14 | $5,632 | $4,499 | $1,132 |

| Wyoming | 7.0% | 49 | $4,282 | $2,351 | $1,931 |

Since we present tax burdens as a share of income as a relative ranking of the 50 states, slight changes in taxes or income can translate into seemingly dramatic shifts in rank. For example, the 20 mid-ranked states, ranging from Delaware (16th) to Missouri (35th), differ in burden by just over one percentage point. However, while burdens are clustered in the center of the distribution, states at the top and bottom can have substantially different burden percentages: the state with the highest burden, New York, has a burden percentage of 14.1 percent, while the state with the lowest burden, Alaska, has a burden percentage of 5.8 percent.

Nationwide, 21 percent of all state and local taxes are collected from nonresidents. As a result, the residents of all states pay surprisingly high shares of their total tax burdens to out-of-state governments. Table 2 lists the per capita dollar amounts of total tax burden and income that are divided to compute each state’s burden, as well as the breakdown of in-state and out-of-state payments for calendar year 2019.

The residents of three states stand above the rest, experiencing the highest state-local tax burdens in the country: New York (14.1 percent of state income), Hawaii (12.8 percent), and Connecticut (12.6 percent). By contrast, the median state-local tax burden is 9.9 percent, and the national average is 10.3 percent. Four states are at or below 8 percent: Alaska (5.8 percent), Wyoming (7.0 percent), Tennessee (7.0 percent), and Texas (8.0 percent)

New York, Hawaii, and Connecticut have occupied the top three spots on the list since 2017, with Maryland, Minnesota, New Jersey, and Vermont vying for the next four spots—though not always in the same order. This may be partially attributed to high expenditure levels, which must be sustained by high levels of revenue. Furthermore, in the case of states like Connecticut and New Jersey, relatively high tax payments to out-of-state governments add to already high in-state payments, both due to direct interactions with neighboring states like New York and because these are high-income states whose residents experience high levels of capital income. High levels of capital income will result in residents paying an increased share of other states’ business taxes.[3] Finally, a substantial portion of Hawaii’s tax burden is generated by the tourism industry and substantially exported to the rest of the country.

The states with the highest state-local tax burdens in calendar year 2019 were:

1. New York (14.1 percent)

2. Connecticut (12.8 percent)

3. Hawaii (12.7 percent)

4. Vermont (12.3 percent)

5. Minnesota (12.1 percent)

6. Maryland (11.8 percent)

7. New Jersey (11.7 percent)

8. California (11.5 percent)

9. Rhode Island (11.4 percent)

10. Illinois (11.1 percent)

The states with the lowest state-local tax burdens in calendar year 2019 were:

50. Alaska (5.8 percent)

49. Wyoming (7.0 percent)

48. Tennessee (7.0 percent)

47. Texas (8.0 percent)

46. Oklahoma (8.2 percent)

45. Arizona (8.7 percent)

44. New Mexico (8.8 percent)

43. Florida (8.8 percent)

42. North Dakota (8.9 percent)

41. Georgia (8.9 percent)

Generally, a state’s ranking could change from year to year for three reasons. First, there could have been a change in total collections by the state, either due to policy changes or economic fluctuations. Second, there may have been a change in the level of income due to changing economic conditions. And third, other states to which residents pay state and local taxes could have seen changes in tax collections (again due to changing policy or economic conditions).

Our current data are for calendar year 2019. Although collections and net national product data are available for 2020, some data necessary for economic adjustments are not yet available and may have fluctuated substantially due to the COVID-19 pandemic. What we do know is that in 2020, net national product fell but tax collections remained steady, buoyed in part by federal programs and Federal Reserve actions which propped up employment, expanded unemployment compensation payments, and stabilized the stock market.

Net national product rose 4.0 percent in 2019. The average tax burden rose by 4.3 percent, slightly faster than the economy. This translated to higher tax burdens as a share of net national product compared to 2018, though only by 0.04 percentage points.

The most pronounced changes in burden as a share of income between 2018 and 2019 occurred in North Dakota (increase of 0.6 percentage points) and Alaska (increase of 0.2 percentage points), as largely exported severance tax revenues fell while in-state tax burdens remained roughly constant. Sixteen states and the District of Columbia saw a decrease in burden percentage, while 34 saw increases, all but five of which were less than 0.2 percentage points.

Table 3 lists each state’s burden as a share of income, including rankings, for the three most recent calendar years available.

| 2017 | 2018 | 2019 | ||||

|---|---|---|---|---|---|---|

| State | Burden | Rank | Burden | Rank | Burden | Rank |

| U.S. Average | 10.4% | 10.3% | 10.3% | |||

| Alabama | 8.9% | 44 | 8.9% | 39 | 9.0% | 38 |

| Alaska | 5.9% | 50 | 5.5% | 50 | 5.8% | 50 |

| Arizona | 8.9% | 45 | 8.7% | 43 | 8.7% | 45 |

| Arkansas | 10.3% | 19 | 10.3% | 18 | 10.4% | 17 |

| California | 11.6% | 8 | 11.5% | 8 | 11.5% | 8 |

| Colorado | 9.8% | 32 | 9.5% | 33 | 9.4% | 34 |

| Connecticut | 12.6% | 2 | 12.6% | 2 | 12.8% | 2 |

| Delaware | 10.5% | 17 | 10.1% | 20 | 10.3% | 18 |

| Florida | 8.9% | 43 | 8.8% | 42 | 8.8% | 43 |

| Georgia | 9.0% | 41 | 8.9% | 40 | 8.9% | 41 |

| Hawaii | 12.4% | 3 | 12.5% | 3 | 12.7% | 3 |

| Idaho | 9.9% | 27 | 9.7% | 30 | 9.6% | 31 |

| Illinois | 11.0% | 12 | 11.0% | 12 | 11.1% | 10 |

| Indiana | 8.9% | 42 | 8.9% | 41 | 8.9% | 39 |

| Iowa | 10.8% | 13 | 10.7% | 13 | 10.8% | 13 |

| Kansas | 10.0% | 25 | 10.0% | 22 | 10.1% | 22 |

| Kentucky | 9.8% | 31 | 9.9% | 26 | 9.9% | 25 |

| Louisiana | 9.2% | 38 | 9.0% | 37 | 9.2% | 36 |

| Maine | 11.1% | 11 | 11.0% | 11 | 11.0% | 12 |

| Maryland | 11.7% | 7 | 11.8% | 6 | 11.8% | 6 |

| Massachusetts | 10.6% | 15 | 10.5% | 15 | 10.5% | 15 |

| Michigan | 9.9% | 28 | 9.9% | 25 | 10.0% | 23 |

| Minnesota | 12.0% | 5 | 12.0% | 5 | 12.1% | 5 |

| Mississippi | 9.4% | 35 | 9.4% | 34 | 9.5% | 33 |

| Missouri | 9.2% | 37 | 9.2% | 35 | 9.2% | 35 |

| Montana | 10.1% | 22 | 10.1% | 21 | 10.1% | 21 |

| Nebraska | 10.4% | 18 | 10.3% | 17 | 10.3% | 19 |

| Nevada | 10.1% | 23 | 9.7% | 29 | 9.7% | 29 |

| New Hampshire | 9.8% | 30 | 9.7% | 27 | 9.7% | 28 |

| New Jersey | 11.8% | 6 | 11.7% | 7 | 11.7% | 7 |

| New Mexico | 9.1% | 39 | 8.6% | 44 | 8.8% | 44 |

| New York | 14.1% | 1 | 14.1% | 1 | 14.1% | 1 |

| North Carolina | 9.7% | 33 | 9.6% | 32 | 9.5% | 32 |

| North Dakota | 9.5% | 34 | 8.2% | 45 | 8.9% | 42 |

| Ohio | 10.2% | 21 | 10.2% | 19 | 10.3% | 20 |

| Oklahoma | 8.4% | 46 | 8.1% | 46 | 8.2% | 46 |

| Oregon | 11.3% | 10 | 11.1% | 10 | 11.1% | 11 |

| Pennsylvania | 10.5% | 16 | 10.4% | 16 | 10.4% | 16 |

| Rhode Island | 11.4% | 9 | 11.3% | 9 | 11.4% | 9 |

| South Carolina | 9.0% | 40 | 8.9% | 38 | 8.9% | 40 |

| South Dakota | 9.2% | 36 | 9.1% | 36 | 9.1% | 37 |

| Tennessee | 7.0% | 49 | 7.0% | 48 | 7.0% | 48 |

| Texas | 8.3% | 47 | 8.0% | 47 | 8.0% | 47 |

| Utah | 10.0% | 24 | 9.7% | 28 | 9.6% | 30 |

| Vermont | 12.0% | 4 | 12.1% | 4 | 12.3% | 4 |

| Virginia | 9.9% | 26 | 9.9% | 23 | 10.0% | 24 |

| Washington | 10.2% | 20 | 9.9% | 24 | 9.8% | 27 |

| West Virginia | 9.9% | 29 | 9.6% | 31 | 9.9% | 26 |

| Wisconsin | 10.6% | 14 | 10.6% | 14 | 10.7% | 14 |

| Wyoming | 7.2% | 48 | 6.8% | 49 | 7.0% | 49 |

| DC | 10.0% | (26) | 10.0% | (23) | 10.1% | (23) |

Many of the least-burdened states forgo a major tax. For example, Alaska (50th), Wyoming (49th), Tennessee (48th), Texas (47th), and Florida (43rd) all do without taxes on individual income. Similarly, Wyoming and South Dakota (37th) do without a major business tax, and Alaska has no state-level sales tax (though it does allow local governments to levy sales taxes). Notably, opting to not levy a personal income tax causes a state to rely more on other forms of taxation that might be more exportable.

Not every state with a significant amount of nonresident income uses it to lighten the tax load of its own residents. Maine and Vermont have the largest shares of vacation homes in the country,[4] and they collect a sizable fraction of their property tax revenue on those properties, mostly from residents of Connecticut, Massachusetts, and other New England states. Despite this, Maine and Vermont still rank 12th and 4th highest, respectively, in this study.

Despite the importance of nonresident collections and the increasing efforts to boost them, the driving force behind a state’s long-term rise or fall in the tax burden rankings is usually internal and most often a result of deliberate policy choices regarding tax and spending levels or changes in state income levels. This study is not an endorsement of policies that attempt to export tax burdens. From the perspectives of the economy and political efficiency, states can create myriad problems when they purposefully shift tax burdens to residents of other jurisdictions. This study only attempts to quantify the amount of shifting that occurs and understand how it affects the distribution of state and local tax burdens across states.

Historical Trends

Nationally, average state-local tax burdens as a share of income have fallen from 11.7 percent in 1977 (the first year for which comparable Census data are available) to 10.3 percent in 2019. Chart 2 shows the movement of U.S. average state-local tax burdens since 1977.

{kind=link}

Some states’ residents are paying the same share of their income to taxes now as they were three decades ago, but in other states, tax burdens have changed substantially over time. The tax burden in every state fluctuates as years pass for a variety of reasons, including changes in tax law, state economies, and population. Further, changes outside of a state can impact tax burdens as well. See Table 4 for historical trends in burdens by state (selected years).

States Where the Tax Burden Has Changed Dramatically Over Time

Among states with declining tax burdens, Alaska is the extreme example. Before the Trans-Alaska Pipeline system was finished in 1977, taxpayers in Alaska paid 11.7 percent of their share of net national product in state and local taxes. By 1980, with oil tax revenue pouring in, Alaska repealed its personal income tax and started sending out checks to residents instead. The tax burden plummeted, and now Alaskans are the least taxed with a burden of only 5.8 percent of income.

| Table 4. State-Local Tax Burdens as a Percentage of State Income by State, Selected Years | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| State | 1977 | 1980 | 1990 | 2000 | 2010 | 2015 | 2016 | 2017 | 2018 | 2019 |

| U.S. Average | 11.7% | 10.4% | 10.7% | 9.7% | 10.6% | 10.4% | 10.4% | 10.4% | 10.3% | 10.3% |

| Alabama | 10.1% | 9.3% | 9.5% | 8.8% | 9.2% | 8.7% | 8.8% | 8.9% | 8.9% | 9.0% |

| Alaska | 12.7% | 8.9% | 6.1% | 5.1% | 7.2% | 5.7% | 5.9% | 5.9% | 5.5% | 5.8% |

| Arizona | 11.7% | 10.2% | 10.7% | 8.9% | 9.2% | 8.9% | 8.9% | 8.9% | 8.7% | 8.7% |

| Arkansas | 9.4% | 9.2% | 9.3% | 9.4% | 10.8% | 10.4% | 10.4% | 10.3% | 10.3% | 10.4% |

| California | 13.3% | 11.4% | 11.3% | 10.7% | 12.0% | 11.5% | 11.4% | 11.6% | 11.5% | 11.5% |

| Colorado | 11.6% | 10.0% | 10.4% | 8.9% | 9.5% | 9.4% | 9.7% | 9.8% | 9.5% | 9.4% |

| Connecticut | 12.1% | 10.5% | 11.1% | 11.3% | 12.9% | 12.0% | 12.0% | 12.6% | 12.6% | 12.8% |

| Delaware | 10.9% | 10.3% | 9.2% | 8.6% | 9.7% | 10.1% | 10.0% | 10.5% | 10.1% | 10.3% |

| Florida | 10.2% | 8.7% | 9.2% | 8.6% | 10.0% | 8.8% | 8.8% | 8.9% | 8.8% | 8.8% |

| Georgia | 10.5% | 9.9% | 10.5% | 9.3% | 9.5% | 9.0% | 8.9% | 9.0% | 8.9% | 8.9% |

| Hawaii | 11.6% | 11.0% | 10.6% | 9.9% | 10.8% | 12.0% | 12.2% | 12.4% | 12.5% | 12.7% |

| Idaho | 11.7% | 10.5% | 11.0% | 10.2% | 10.0% | 9.6% | 9.8% | 9.9% | 9.7% | 9.6% |

| Illinois | 11.5% | 10.6% | 10.6% | 9.4% | 10.9% | 11.2% | 11.0% | 11.0% | 11.0% | 11.1% |

| Indiana | 9.4% | 8.3% | 9.5% | 8.4% | 9.9% | 9.1% | 8.9% | 8.9% | 8.9% | 8.9% |

| Iowa | 11.5% | 10.7% | 11.0% | 9.5% | 10.0% | 10.5% | 10.8% | 10.8% | 10.7% | 10.8% |

| Kansas | 10.6% | 9.6% | 10.3% | 9.6% | 10.1% | 9.2% | 9.4% | 10.0% | 10.0% | 10.1% |

| Kentucky | 10.7% | 9.8% | 10.3% | 10.0% | 9.7% | 9.8% | 9.8% | 9.8% | 9.9% | 9.9% |

| Louisiana | 8.6% | 8.0% | 8.5% | 8.4% | 8.2% | 8.7% | 9.0% | 9.2% | 9.0% | 9.2% |

| Maine | 11.4% | 10.9% | 11.5% | 10.9% | 10.9% | 11.4% | 11.2% | 11.1% | 11.0% | 11.0% |

| Maryland | 12.6% | 11.6% | 11.6% | 10.6% | 10.9% | 11.7% | 11.6% | 11.7% | 11.8% | 11.8% |

| Massachusetts | 13.4% | 12.1% | 11.4% | 10.0% | 10.9% | 10.7% | 10.5% | 10.6% | 10.5% | 10.5% |

| Michigan | 11.7% | 10.6% | 10.6% | 9.6% | 10.2% | 9.8% | 9.7% | 9.9% | 9.9% | 10.0% |

| Minnesota | 12.3% | 10.9% | 11.5% | 10.3% | 11.3% | 12.0% | 12.0% | 12.0% | 12.0% | 12.1% |

| Mississippi | 10.5% | 9.4% | 9.5% | 9.1% | 9.3% | 9.7% | 9.5% | 9.4% | 9.4% | 9.5% |

| Missouri | 10.3% | 9.4% | 9.9% | 9.3% | 9.5% | 9.1% | 9.1% | 9.2% | 9.2% | 9.2% |

| Montana | 10.8% | 9.6% | 10.0% | 8.9% | 9.5% | 10.1% | 9.9% | 10.1% | 10.1% | 10.1% |

| Nebraska | 12.1% | 10.8% | 10.3% | 9.6% | 10.2% | 10.2% | 10.3% | 10.4% | 10.3% | 10.3% |

| Nevada | 9.4% | 7.8% | 8.2% | 7.2% | 8.8% | 10.0% | 10.2% | 10.1% | 9.7% | 9.7% |

| New Hampshire | 9.9% | 8.5% | 8.6% | 7.7% | 8.8% | 9.8% | 9.7% | 9.8% | 9.7% | 9.7% |

| New Jersey | 13.9% | 12.1% | 11.9% | 11.0% | 13.0% | 11.6% | 11.6% | 11.8% | 11.7% | 11.7% |

| New Mexico | 10.1% | 9.3% | 10.8% | 9.9% | 9.1% | 9.4% | 9.3% | 9.1% | 8.6% | 8.8% |

| New York | 14.7% | 13.2% | 13.1% | 11.7% | 13.2% | 14.7% | 14.3% | 14.1% | 14.1% | 14.1% |

| North Carolina | 10.9% | 10.2% | 10.5% | 9.7% | 10.5% | 9.8% | 9.8% | 9.7% | 9.6% | 9.5% |

| North Dakota | 13.0% | 10.8% | 10.4% | 9.4% | 9.5% | 9.6% | 9.3% | 9.5% | 8.2% | 8.9% |

| Ohio | 9.9% | 9.2% | 10.5% | 10.2% | 10.2% | 10.3% | 10.3% | 10.2% | 10.2% | 10.3% |

| Oklahoma | 9.7% | 8.7% | 10.0% | 9.7% | 9.3% | 8.2% | 8.4% | 8.4% | 8.1% | 8.2% |

| Oregon | 12.4% | 11.2% | 11.8% | 10.1% | 10.9% | 11.2% | 11.2% | 11.3% | 11.1% | 11.1% |

| Pennsylvania | 11.5% | 10.7% | 10.6% | 9.9% | 10.6% | 10.4% | 10.4% | 10.5% | 10.4% | 10.4% |

| Rhode Island | 12.7% | 11.6% | 11.4% | 11.1% | 11.4% | 11.6% | 11.6% | 11.4% | 11.3% | 11.4% |

| South Carolina | 10.3% | 9.7% | 10.2% | 9.1% | 8.8% | 8.9% | 8.9% | 9.0% | 8.9% | 8.9% |

| South Dakota | 10.1% | 8.9% | 8.3% | 7.2% | 7.9% | 8.6% | 9.0% | 9.2% | 9.1% | 9.1% |

| Tennessee | 9.1% | 8.0% | 8.1% | 7.0% | 7.9% | 7.3% | 7.2% | 7.0% | 7.0% | 7.0% |

| Texas | 8.9% | 7.7% | 8.7% | 7.5% | 8.4% | 8.2% | 8.3% | 8.3% | 8.0% | 8.0% |

| Utah | 11.7% | 11.1% | 11.2% | 10.4% | 10.0% | 9.6% | 9.8% | 10.0% | 9.7% | 9.6% |

| Vermont | 13.0% | 10.8% | 11.1% | 10.1% | 10.8% | 11.7% | 11.8% | 12.0% | 12.1% | 12.3% |

| Virginia | 11.4% | 10.4% | 10.5% | 9.8% | 10.0% | 9.6% | 9.8% | 9.9% | 9.9% | 10.0% |

| Washington | 10.8% | 9.6% | 10.1% | 8.6% | 9.9% | 9.9% | 10.0% | 10.2% | 9.9% | 9.8% |

| West Virginia | 10.8% | 10.2% | 10.0% | 9.7% | 10.5% | 10.1% | 10.1% | 9.9% | 9.6% | 9.9% |

| Wisconsin | 14.1% | 12.2% | 12.3% | 11.5% | 11.7% | 10.6% | 10.6% | 10.6% | 10.6% | 10.7% |

| Wyoming | 9.0% | 7.9% | 6.9% | 6.7% | 8.3% | 8.5% | 8.2% | 7.2% | 6.8% | 7.0% |

| DC | 13.4% | 13.8% | 12.9% | 11.5% | 9.8% | 10.2% | 9.9% | 10.0% | 10.0% | 10.1% |

Similarly, North Dakota’s burden has fallen from 13.0 percent in 1977 to 8.9 percent of net state product in 2019. Its burden was even lower in 2018 at 8.2 percent, before a contraction in oil markets. Interestingly, the District of Columbia’s tax burden has also fallen dramatically, declining 3.4 percentage points since 1977, when it was 13.4 percent. In 2019 it stood at 10.1 percent.

Although most states have seen a decrease in tax burdens over time, six have experienced increases since 1977. Hawaii taxpayers have seen tax burdens increase by 1.2 percentage points, from 11.6 to 12.7 percent, between 1977 and 2019. And since 1977, Arkansas taxpayers have gone from some of the least taxed at 9.4 to an above-average tax burden at 10.4 percent. Connecticut, Louisiana, Ohio, and Nevada have also seen net increases as a percentage of net product since 1977.

Conclusion

When measuring the burden imposed on a given state’s residents by all state and local taxes, one cannot look exclusively to collections figures for the governments located within state borders. A significant amount of tax shifting takes place across state lines, and shifting is not uniform. Furthermore, shifting should not be ignored when attempting to understand the burden faced by taxpayers within a state.

[1] Net national product is a measure of the market value of the goods and services produced by U.S. residents less the value of the fixed capital used in production (or less depreciation).

[2] Charles E. McClure, “The Interstate Exporting of State and Local Taxes: Estimates for 1962,” National Tax Journal 20:1 (1967): 49–75.

[3] Business taxes collected by states are allocated nationwide based in part on each state’s share of capital income.

[4] U.S. Census Bureau, “Historical Census of Housing Tables: Vacation Homes,” Census of Housing.